1)chinwel 5007 Q1 之eps=6 sen ,rolling 4 quarters eps=24sen ,

pe=13 ,stock price=rm3.12 ,目前仍然物有所值!

chinwel 有强大净利做后盾,股价上升有理,又有红股计昼.

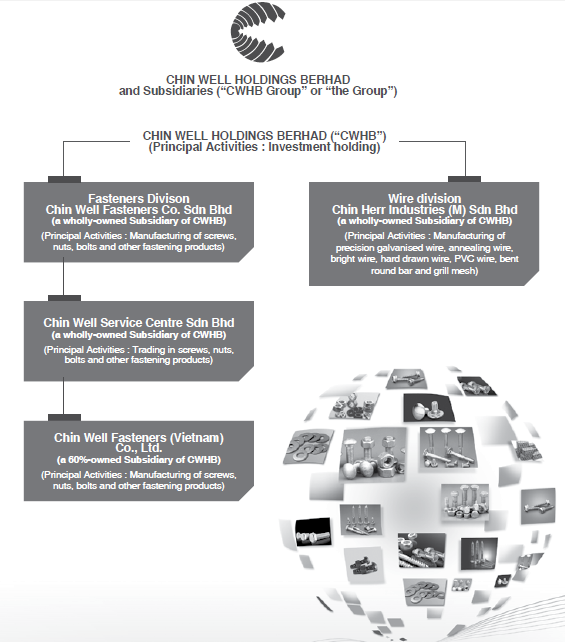

2)公司主要生產螺絲、螺母、螺帽、大頭釘及螺栓等產品,在大馬檳城及越南擁有生產線.

晋纬控股在大马拥有两座厂房和一家贸易公司,晋纬控股旗下3座厂房中,规模最大的是在越南,

该厂房是与一家投资公司合资,规模是大马厂房的3倍,仅仅包装部面积就有4个足球场大。

占有越南厂房股权100%的晋纬控股,当初决定在当地设立厂,除了因为槟城劳工短缺,

无法进一步扩展产能外,也是配合了进军DIY领域。

3)该集团的财务状况稳定以及在紧固件领域上的领导地位,从2014财年起,将派发至少40%的净利为股息。

4)全球商业市场调查公司Freedonia集团在《全球工业紧固件报告》中,

预计全球工业紧固件的销售额,在2016年可达829亿美元。晋纬控股将持续提高自助式螺丝

(DIY fastener)的业务,并认为将是下一个业务增长的催化剂。

5)晉緯控股(CHINWEL,5007,主板工業產品組)董事經理兼聯合創辦人蔡永泉,

增購該公司2千153萬股或佔7.9%的股權,使他在該公司的持股增加至58.12%,或是1億5千841萬股的股票。

明显对公司未来成长深具信心.

6)越南子公司2014財年的淨利達2140萬令吉,幾乎是晉緯控股淨利(4460萬令吉)的一半,

因此在今年底完成是項收購后,前者的淨利將完全貢獻晉緯控股,(估算可贡献净利达3000万).

7)转自--糊涂注:这是一篇10年前的台湾民营经济报报导,10年后的今天,晋亿、

晋纬与晋禾的货舱管理也正如3兄弟预测般的为公司带来丰厚的利润,

这也让我对晋纬(Chinwel)高库存或约RM100mil完成品感到安心。还没有研究这家公司之前,

我曾疑虑为何那么低调的公司竟然会有那么多基金买入它,尤其是国外的基金,

而这一些都在我看了晋禾、晋亿的网站的资料后才意识到原来在大马上市的Chinwel并不简单,

它竟然是全世界螺丝产量第一的一部分。当时我就想,那么多的利好,竟然只值PE 10?

这也未免太不可思议了,尤其是在中国上市的姐妹公司PE已来到300的天价水平,这也是我追高这家公司的理由之一。

8)官有缘前辈的加股后,投资者更有信心了,chinwel也是投行的投资对象.

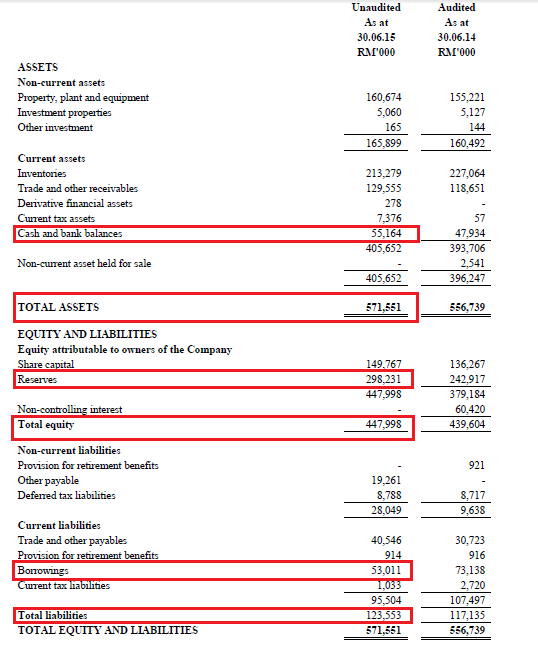

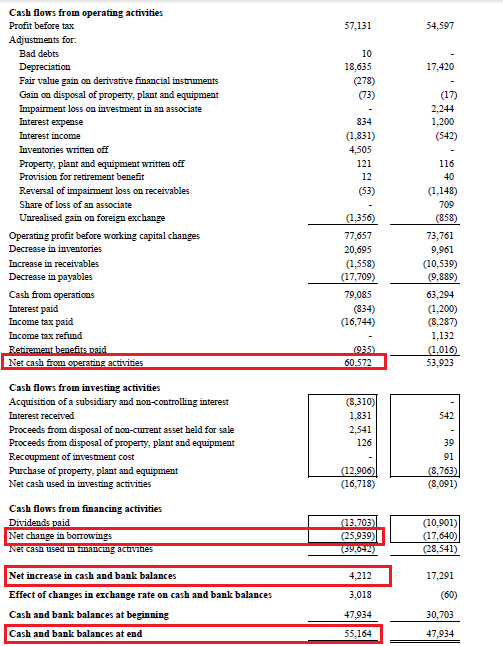

9)公司于30-09-2015 Chinwel 的债务6097万,公司有CASH 9134万,净现金达3037万.NTA=RM1.62

10)这些因素都是使Chinwel继续向北,引起人们的购兴,目前仍以单位数的本益比交易.

(估计2016 eps=24sen,pe=9.6 ,股价=rm2.31)

进与守为良策,rm3.12在等着上演.

供参考,进出自负.

--从早期的TNLOGIS,PRLEXUS,LATITUT,PWRROT,LILLHEN,INARI,VITRO,KESM,WELLCAL,

MAGNI,HOMERIZ,POHUAT,ksl,supermx,jaycorp,

teoseng,lcth,EVERGREEN,SUCCESS,RGB,GADANG,canone等,大致上只赚些绳头小利,

并没给净化奔跑,其实中長期投资者只要

进入价合理与低价,都可以收藏,公司基本面不变情况下,不必急于出售,这次chinwel rm2.24进入价,

因此安全线很好,打算收中長期求更好的回酬.

--chinwel提供的投资机会时,真的是越買越高,趁现在低,早点进货,等待丰衣足食.

正确机率多才能成功

所以,总括一句,我们只是平民散户,通过本身对投资的喜好和研究,希望(努力)在股市中挣到不错的回酬,

什么大师专家,受之有愧,不必对号入座。

不论我们做什么决定,都会诚实的面对结果。投资组合不是考试,不能每次要求一百分。

这三年多来,我们确然做了一些低级错误,不过也做了更多的正确决定,所以我们才能获得如此不差的成绩。

现实生活里,错和对总是交叉发生,每次都做对,不叫“成功”,那是“完美”,是每个人追求的境界(却不大可能达到)。

成功的投资者,只需要把正确的投资机率更多发生就是了。

取自于--http://klse.i3investor.com/blogs/golden_years/55570.jsp

1)网友糊涂兄之功课---

星期四, 十一月 26, 2015

ChinWell Q1'16 成绩单 + 年会简记

ChinWell Q1'16的业绩非常的标青,每股盈利高达6.07分VS去年同期3.28分,营业额也比去年增加了约10%左右,主要是因为马来西亚业务带动,我猜想这是GST带来的正面效应吧!还有就是防盗篱笆和石笼网的盈利也比去年同期进步了许多,马币走软也为它带来约287万的额外盈利。季报的重点如下:

- 标紧固件(Fasterners)业务增长了7.84%,盈利增长34%。

- 防盗篱笆和石笼网(Wire Products)业务也增长了15%,成功的转亏为盈,为公司带来2.09mil盈利。

- 马来西亚业务大幅度增长120%,GST除了让产品价格更具竞争力之外(6% GST VS 10% 销售税),同时也因客户减少购买走私入口的中国货而需求激增。我认为这是长期的利好,Chinwel有望逐渐提高本地市场的份额。

- 欧洲市场萎缩了,相信若不是DIY业务与汇率撑着,欧洲营业额的贡献将会更少。

- 每股净现金来到10分的高位了,资产表越来越漂亮,维持40%的派息率简直没难度。

数据:

年会简记

今天我也如约的出席了Chinwel的股东大会, 有幸与公司董事经理蔡永泉+太太, 公司执行董事蔡芑芸聊了约半个小时, 从公司业务开始聊, 也谈及国际经济局势与东南亚各国的竞争力。重点如下:

- 晋禾、晋亿与晋纬并不存在竞争关系,产品与针对的市场都各有不同。(一带一路火车轨道受惠的是晋亿)

- 公司的原料从中国采购,晋亿公司会帮忙圈定合格的商家,目前有3家公司以相当竞争的价格供应原料。(公司不考虑从晋亿购买原料)

- 马来西亚工厂的新员工(外劳)问题尚未解决,目前的员工只足够让公司以1班(shift)生产。

- 越南的员工冲劲十足,大部分员工都会做足12个小时(OT)。

- DIY包装需要靠人工,因此DIY包装阵营在越南,同时越南也是公司将来的成长的动力。

- 公司对DIY的前景表示乐观, 欧洲经济不景气会导致越来越多人亲自动手维修房子与家具, 这能够为公司的销售带来稳定的订单。

- 公司将会受惠于TPPA,目前从越南出口至美国需要8%的税务,若TPPA执行,公司将有能力与中国其它厂家竞争。值得一提的是,美国的市场比欧洲更大。

- 公司的生产成本无法追平中国的主要原因是中国对环境的管理较为松懈,举个例子:公司单单在water treatment方面每个月就至少要花上约400k的费用。无论如何,相信中国会逐步提升对环境保护的要求,因此5年后相信公司的竞争力就能跟上了。

- 中国目前正在处理僵尸企业的问题,因此中国国内的商家都是在打着割喉战,廉价销售亏损较少,不销售基本上就是等破产。预计最终能够存活下来的将会是行业的老大、老二,没有竞争力的商家会被慢慢淘汰。

- 目前集团(包括晋禾、晋亿)占了全世界约3%的销售,是当之无愧的老大!

- 来自印度的竞争并不强,定时交货是它们最大的弱点。同时,印度内需足以消化国内的产能,因此极少在国际竞争。

- 公司段其内并没有派发红股的打算,不过明年会考虑回购自家公司。

- 公司上市至今,蔡董与家族从未卖过公司的股票,曾经有基金找过他,希望能够买到一些股份,然而蔡董毫不考虑就拒绝了。蔡董还说,在大马上市的意义并不大,他也曾想过要把公司私有化,不过最终还是没有执行。

蔡董是个相当务实并低调的人,不会乱花不该花的金钱,对蔡董来说,能够设立一个理念并贯彻的执行与达到目标是最有满足感的事。老板娘更笑说蔡董以前是工作狂,年轻时每天都做足12个小时。我们虽然还谈及了许多信仰、人生观之类的,蔡董甚至开玩笑的说要请我们这些比较年轻的帮忙看管公司。呵呵,各位股东有兴趣吗?写了那么多废话不好,就此打住。。

总个来说,Chinwel是一家不可多得的好公司,业务会稳定的慢慢成长,不会有太多爆发的惊喜,不过也不会让他投资者晚上睡不着觉就是了。蔡董还说,无论经济或营运环境多么糟糕,公司还是能够获利,同时公司也准备好面对未来L型经济的种种挑战!基于我没有写笔记,公司业务方面的讨论就只记得那么多了,希望能够给大家一个参考。

2)

星期六, 十一月 21, 2015

交易记录之追高买入Chinwel

上个周末看了Chinwell的年报之后,我才察觉经过这几年的经营之后,它已经成为一家净现金公司,并开始制定了40%派息率的政策,同时也是马币走软与GST的受惠公司之一。

星期一短暂的观察它的交易情况之后,我就开始微量的慢慢买入它,我本来是打算买点票打底顺便出席它的AGM,可没想到它周四开盘就走高,下午4点半之后又爆涨20分让我措手不及,就没有追高买入它。

然而,周4晚上重新翻看公司过去3年的资料后,我就决定如果它的买盘依然强劲,我就追高买入它了。它周五的走势依旧强劲,半天的成较量就超越了2000张,我也就按照计划在1.68-1.72的价码加码了约50张的票。(投资组合买入的平均成本也从RM1.465增加得到RM1.57)

同时,刚好在闭市前Alaqar在1.33出现买盘,我就卖了约98张的货来补充子弹库,好让我下个星期在Chinwel的季报出炉前再加码一点点来当中期投资。这几天比较忙,也连续几晚看Chinwel的资料看到凌晨1.30am,因此我打算出席它的AGM之后,或等它的季报出炉之后再补上Chinwel的功课。今天只是记录一下我疯狂追高的交易,将来可以做个参考/学习,这样冲动的交易是对或错反而是次要了。

注:

上个星期我的交易比较多,为了筹积买Chinwel的资金,我在1块钱的价码把Hexza清了,只留1张免费票。同时也把手头上的CSCENIC与部分的Alaqar卖出换Chinwel,下星期若有好的价格,我还会继续套利Alaqar。另外一家我打算加码的Complet 这几天的交易量都不大,看来唯有季报出炉之后再决定是否追高加码了。

数据:

3)

星期二, 十一月 24, 2015

转贴:台湾“螺丝大王”—蔡氏三兄弟 (chinwel的创业史)

晋亿,这家一般人很陌生的公司,其实是全世界最大的螺丝企业。不起眼的小螺丝,被称为工业之米,最便宜的报价不过是新台币一分一颗,但是,光是生产螺丝,晋亿集团(泛指旗下三家公司)年销售收入就达150亿元,可生产两万种螺丝,占全世界4万种螺丝的一半。晋亿集团在马来西亚、越南、中国台湾和大陆共有4个工厂,拥有两家已上市和即将上市的公司。另外,晋亿集团的螺丝仓储与物流系统是全球最大的,总容重量达30万吨,所存钢材相当于41座巴黎铁塔的用量。分布在6个国家的7个仓库随时库存2万种螺丝,每种都有3个月到一年用量的库存,以供应全球所需。全美进口的螺丝中,每两颗就有一颗是晋亿的产品。这个庞大的螺丝王国,年产量55.80万吨。

把客厅当工厂成立晋禾公司

螺丝王国的主角是三个兄弟:大哥蔡永龙现任中国大陆晋亿实业董事长、老二蔡永泉负责马来西亚和越南厂,目前是晋纬总经理,老三蔡永裕则是中国台湾晋禾总经理。 1975年,还是20岁小伙子的蔡永龙,听说高雄冈山镇的螺丝产业正兴起,对那里的螺丝机像印钞机不断吐出钞票的传言充满憧憬。国小毕业后,蔡永龙就离开台湾彰化竹塘老家,到冈山的大顺螺帽厂,从工厂最低层的黑手开始做起。 1979年,蔡永龙自行创业,凑了10万元,带着弟弟蔡永泉、蔡永裕自己买机器设备、零组件,组了两台螺帽成型机,把客厅当工厂,成立晋禾公司开始生产螺帽。蔡永龙三兄弟出身比别人差、起步比别人晚,发展过程中,也遇到难以突破的瓶颈。当时,台湾中钢供应原料采取配额制,以上一年度的采购量,决定下年度原料提取的多寡。而且螺丝业者若想进口原料,还需要中钢出具证明许可,原料供应制度限制了螺丝厂的发展,出现了强者更强的局面

走向海外第一步买错设备买错地

当时蔡家三兄弟在台湾经营的晋禾企业,一个月获利已40万元,算是富足的中小企业。但是,蔡永龙不满足,赚钱之外,他要当螺丝业的老大!只是,在中钢的原料配额制下,他永远不可能在台湾当上第一。要摆脱这样的困境,只有到海外设厂! 1987年,兄弟抱着大破大立的决心,展开前进泰国的计划,学了一年泰文之后,1988年,三兄弟前往泰国签下购地合约。在朋友邀请下,顺便往马来西亚槟城考察,他们发现马来西亚槟城7成是华人,主要语言是闽南语,最重要的是当地有钢铁原料供应!当天,兄弟在旅途上召开紧急会议,转往槟城设厂,只在泰国设仓库。他们从一开始就要做南亚第一,决定陆续投入11亿元。为了当第一,蔡永龙亲自督军,他仅国小毕业,但马来西亚的晋纬公司,却用了包括马来西亚、印度、越南、中国、泰国、尼泊尔、孟加拉、缅甸、菲律宾、斯里兰卡等10国员工。为突破语言限制,蔡永龙发明图解螺丝生产的标准作业流程,包括螺丝线抽线机、螺丝成型机、磨牙设备到仓库管理,所有的螺丝生产机台,都画了详细的操作步骤,让所有员工可一目了然。这套图解流程,让训练生手员工的时间,从3个月缩短为1个月。 10国员工的文化背景和生活习惯南辕北辙。印度人喜欢在宿舍房间里养鸡生蛋当早餐,越南人则喜欢抓野狗煮火锅。蔡永龙只好把宿舍分成10处,分开管理。如今,晋亿集团在越南、中国大陆的工厂都有菲律宾、马来西亚干部进驻,人才已开始国际化。 1993年,蔡永龙有了更石破天惊的举动,他决定陆续投资1亿美元到大陆设厂。当时台湾晋禾销售收入不过6亿元,这笔庞大投资一旦成功,蔡家三兄弟就可以成为世界第一,但也有极大风险,万一失败,三兄弟可能没本钱再爬起来。

逆势操作赚“库存”和“时间”的钱

一年一年搜集包括各国最大代理商当年度买卖状况,输入电脑建立资料与分析,如果搜集不到代理商资料,就直接花钱跟当地海关购买。在中国大陆,蔡永龙大胆尝试,他采购巴西、俄罗斯、南韩与当地的便宜钢材。这些钢材品质比较低劣,生产不出好的螺丝,因此一般同业不敢采购。但他不认输,为扭转颓势,他开始投资上游工厂设备,前前后后花了3年摸索与学习,直到1998年,最大、最完整的垂直整合厂──大陆晋亿厂终于完成投产,螺丝三兄弟完成全世界第一个螺丝一条龙生产线,也正式坐上全球产能第一宝座。整合了螺丝制造过程,三兄弟接着发展仓储物流和渠道。 1992年,台湾晋禾每年获利在5000万元左右,却决定花8000万元盖台湾第一个螺丝自动仓储,准备储存价值2亿元、总量8000千吨的螺丝。消息传出,同业抱着看笑话的心态来参观。自动仓储展现了三兄弟在螺丝产业的大格局。

晋亿的螺丝,从成品完成到仓库就位储存,全部自动化。蔡永裕说,没有自动仓库前,一条出货线三个工人,要从当时数千种螺丝中找出客户定单所要求的规格与数量,装满一个货柜要从早上八点做到半夜两、三点,现在靠自动仓储,一个工人装满一个货柜只要20分钟。他们的算盘是,当全球厂商都讲究“零库存”时,逆势操作赚“库存”和“时间”的钱。蔡永龙说,靠生产螺丝赚钱的时代已过去,螺丝业已经是服务业,大陆晋亿、马来西亚晋纬、台湾晋禾要赚的是物流跟管理的钱。台湾大学国际企业所教授赵义隆分析,所谓物流与生产两者零库存,并非是一味将库存放在生产端,或放在最末端零组件供货商上,而是两者之间有一套紧密的系统。蔡永泉说:“我们手上随时都有全球各大代理的所有买卖资料,清清楚楚掌握整个螺丝市场交易与库存状况!”三兄弟不是盲目地堆积库存,而是掌握市场最新动态。他们不仅精确掌握全美最大螺丝代理商Fastenal下给全球各大螺丝厂定单的数量,还可以替Fastenal分析整体美国市场的最新状况,教Fastenal怎么抓住螺丝市场的商机。

“从我们跨出台湾开始,我们就有计划地一步步搜集世界各国螺丝市场交易现况!”蔡永泉说,建立一个国家整体螺丝进出口与使用现况的资讯库,最少要三年。一年一年搜集包括各国最大代理商当年度买卖状况,输入电脑建立资料与分析,如果搜集不到代理商资料,就直接花钱跟当地海关购买,不计代价与成本,也要取得该国在该年度到底进出口多少种类与数量的螺丝。依据这套系统,螺丝三兄弟按照兄弟分工的方式,在大陆的蔡永龙主攻美国工业用螺丝与大陆市场、东南亚的老二蔡永泉主攻欧盟、东南亚与民生工业用螺丝、台湾的老三蔡永裕主攻高价合金钢螺丝市场。所有的库存按照市场实时状况做调整,缺什么螺丝就生产什么螺丝。 “所有库存务求三个月周转一次,随时检讨周转率低的库存!”蔡永泉、蔡永裕兄弟笑着说,应该怎么堆、该做什么库存才是关键。

不仅如此,三兄弟由台湾主导研发,不停地开发新螺丝,将产品线的种类不断推高。赵义隆分析,一次式服务时代,客户在乎的不仅是报价,而是整体性的服务,服务能力越高,掌握定单的机会越大。以螺丝产业为例,8成的定单可能都是标准型产品,其余两成则会有特殊要求,能替客户解决这两成的难题,就能通吃所有的定单,这就是胜出关键。 “我们不仅替Fastenal解决定单难题,还要替它节省成本!”蔡永泉说,过去螺丝交货是一个个货柜运往洛杉矶,Fastenal收货之后再自行依不同规格与数量分装送往各大据点,现在透过晋亿的自动仓储与两万种螺丝分类,Fastenal只要告知各据点需求与数量,螺丝三兄弟的工厂就按照这些需求,直接送往美国各地,省了Fastenal自行分装的人力与物流的费用。螺丝生产毛利仅10%,但三兄弟一次式服务却能加收5%的服务费,在螺丝三兄弟手里,螺丝产业不再是制造业,完全变成另一套管理与服务模式。 (吕国祯)

金羊网-民营经济报

把客厅当工厂成立晋禾公司

螺丝王国的主角是三个兄弟:大哥蔡永龙现任中国大陆晋亿实业董事长、老二蔡永泉负责马来西亚和越南厂,目前是晋纬总经理,老三蔡永裕则是中国台湾晋禾总经理。 1975年,还是20岁小伙子的蔡永龙,听说高雄冈山镇的螺丝产业正兴起,对那里的螺丝机像印钞机不断吐出钞票的传言充满憧憬。国小毕业后,蔡永龙就离开台湾彰化竹塘老家,到冈山的大顺螺帽厂,从工厂最低层的黑手开始做起。 1979年,蔡永龙自行创业,凑了10万元,带着弟弟蔡永泉、蔡永裕自己买机器设备、零组件,组了两台螺帽成型机,把客厅当工厂,成立晋禾公司开始生产螺帽。蔡永龙三兄弟出身比别人差、起步比别人晚,发展过程中,也遇到难以突破的瓶颈。当时,台湾中钢供应原料采取配额制,以上一年度的采购量,决定下年度原料提取的多寡。而且螺丝业者若想进口原料,还需要中钢出具证明许可,原料供应制度限制了螺丝厂的发展,出现了强者更强的局面

走向海外第一步买错设备买错地

当时蔡家三兄弟在台湾经营的晋禾企业,一个月获利已40万元,算是富足的中小企业。但是,蔡永龙不满足,赚钱之外,他要当螺丝业的老大!只是,在中钢的原料配额制下,他永远不可能在台湾当上第一。要摆脱这样的困境,只有到海外设厂! 1987年,兄弟抱着大破大立的决心,展开前进泰国的计划,学了一年泰文之后,1988年,三兄弟前往泰国签下购地合约。在朋友邀请下,顺便往马来西亚槟城考察,他们发现马来西亚槟城7成是华人,主要语言是闽南语,最重要的是当地有钢铁原料供应!当天,兄弟在旅途上召开紧急会议,转往槟城设厂,只在泰国设仓库。他们从一开始就要做南亚第一,决定陆续投入11亿元。为了当第一,蔡永龙亲自督军,他仅国小毕业,但马来西亚的晋纬公司,却用了包括马来西亚、印度、越南、中国、泰国、尼泊尔、孟加拉、缅甸、菲律宾、斯里兰卡等10国员工。为突破语言限制,蔡永龙发明图解螺丝生产的标准作业流程,包括螺丝线抽线机、螺丝成型机、磨牙设备到仓库管理,所有的螺丝生产机台,都画了详细的操作步骤,让所有员工可一目了然。这套图解流程,让训练生手员工的时间,从3个月缩短为1个月。 10国员工的文化背景和生活习惯南辕北辙。印度人喜欢在宿舍房间里养鸡生蛋当早餐,越南人则喜欢抓野狗煮火锅。蔡永龙只好把宿舍分成10处,分开管理。如今,晋亿集团在越南、中国大陆的工厂都有菲律宾、马来西亚干部进驻,人才已开始国际化。 1993年,蔡永龙有了更石破天惊的举动,他决定陆续投资1亿美元到大陆设厂。当时台湾晋禾销售收入不过6亿元,这笔庞大投资一旦成功,蔡家三兄弟就可以成为世界第一,但也有极大风险,万一失败,三兄弟可能没本钱再爬起来。

逆势操作赚“库存”和“时间”的钱

一年一年搜集包括各国最大代理商当年度买卖状况,输入电脑建立资料与分析,如果搜集不到代理商资料,就直接花钱跟当地海关购买。在中国大陆,蔡永龙大胆尝试,他采购巴西、俄罗斯、南韩与当地的便宜钢材。这些钢材品质比较低劣,生产不出好的螺丝,因此一般同业不敢采购。但他不认输,为扭转颓势,他开始投资上游工厂设备,前前后后花了3年摸索与学习,直到1998年,最大、最完整的垂直整合厂──大陆晋亿厂终于完成投产,螺丝三兄弟完成全世界第一个螺丝一条龙生产线,也正式坐上全球产能第一宝座。整合了螺丝制造过程,三兄弟接着发展仓储物流和渠道。 1992年,台湾晋禾每年获利在5000万元左右,却决定花8000万元盖台湾第一个螺丝自动仓储,准备储存价值2亿元、总量8000千吨的螺丝。消息传出,同业抱着看笑话的心态来参观。自动仓储展现了三兄弟在螺丝产业的大格局。

晋亿的螺丝,从成品完成到仓库就位储存,全部自动化。蔡永裕说,没有自动仓库前,一条出货线三个工人,要从当时数千种螺丝中找出客户定单所要求的规格与数量,装满一个货柜要从早上八点做到半夜两、三点,现在靠自动仓储,一个工人装满一个货柜只要20分钟。他们的算盘是,当全球厂商都讲究“零库存”时,逆势操作赚“库存”和“时间”的钱。蔡永龙说,靠生产螺丝赚钱的时代已过去,螺丝业已经是服务业,大陆晋亿、马来西亚晋纬、台湾晋禾要赚的是物流跟管理的钱。台湾大学国际企业所教授赵义隆分析,所谓物流与生产两者零库存,并非是一味将库存放在生产端,或放在最末端零组件供货商上,而是两者之间有一套紧密的系统。蔡永泉说:“我们手上随时都有全球各大代理的所有买卖资料,清清楚楚掌握整个螺丝市场交易与库存状况!”三兄弟不是盲目地堆积库存,而是掌握市场最新动态。他们不仅精确掌握全美最大螺丝代理商Fastenal下给全球各大螺丝厂定单的数量,还可以替Fastenal分析整体美国市场的最新状况,教Fastenal怎么抓住螺丝市场的商机。

“从我们跨出台湾开始,我们就有计划地一步步搜集世界各国螺丝市场交易现况!”蔡永泉说,建立一个国家整体螺丝进出口与使用现况的资讯库,最少要三年。一年一年搜集包括各国最大代理商当年度买卖状况,输入电脑建立资料与分析,如果搜集不到代理商资料,就直接花钱跟当地海关购买,不计代价与成本,也要取得该国在该年度到底进出口多少种类与数量的螺丝。依据这套系统,螺丝三兄弟按照兄弟分工的方式,在大陆的蔡永龙主攻美国工业用螺丝与大陆市场、东南亚的老二蔡永泉主攻欧盟、东南亚与民生工业用螺丝、台湾的老三蔡永裕主攻高价合金钢螺丝市场。所有的库存按照市场实时状况做调整,缺什么螺丝就生产什么螺丝。 “所有库存务求三个月周转一次,随时检讨周转率低的库存!”蔡永泉、蔡永裕兄弟笑着说,应该怎么堆、该做什么库存才是关键。

不仅如此,三兄弟由台湾主导研发,不停地开发新螺丝,将产品线的种类不断推高。赵义隆分析,一次式服务时代,客户在乎的不仅是报价,而是整体性的服务,服务能力越高,掌握定单的机会越大。以螺丝产业为例,8成的定单可能都是标准型产品,其余两成则会有特殊要求,能替客户解决这两成的难题,就能通吃所有的定单,这就是胜出关键。 “我们不仅替Fastenal解决定单难题,还要替它节省成本!”蔡永泉说,过去螺丝交货是一个个货柜运往洛杉矶,Fastenal收货之后再自行依不同规格与数量分装送往各大据点,现在透过晋亿的自动仓储与两万种螺丝分类,Fastenal只要告知各据点需求与数量,螺丝三兄弟的工厂就按照这些需求,直接送往美国各地,省了Fastenal自行分装的人力与物流的费用。螺丝生产毛利仅10%,但三兄弟一次式服务却能加收5%的服务费,在螺丝三兄弟手里,螺丝产业不再是制造业,完全变成另一套管理与服务模式。 (吕国祯)

金羊网-民营经济报

糊涂注:这是一篇10年前的台湾民营经济报报导,10年后的今天,晋亿、晋纬与晋禾的货舱管理也正如3兄弟预测般的为公司带来丰厚的利润,这也让我对晋纬(Chinwel)高库存或约RM100mil完成品感到安心。还没有研究这家公司之前,我曾疑虑为何那么低调的公司竟然会有那么多基金买入它,尤其是国外的基金,而这一些都在我看了晋禾、晋亿的网站的资料后才意识到原来在大马上市的Chinwel并不简单,它竟然是全世界螺丝产量第一的一部分。当时我就想,那么多的利好,竟然只值PE 10?这也未免太不可思议了,尤其是在中国上市的姐妹公司PE已来到300的天价水平,这也是我追高这家公司的理由之一。

4)十面埋伏兄之功课--

5)资汇分析 5007 chinwel--

6)感谢官前辈的付出与回报社会。

a)My Critics and Doubting Thomas - Koon Yew Yin

Author: Koon Yew Yin | Publish date: Tue, 5 Jan 2016, 09:21 AM

In the stock market, with the exception of the original company founders who listed their shares, smart investors will make money and stupid ones will lose money. As money cannot come down from the sky, the smart investors’ profit must come from those losers.

As I said many a time, all investors must examine their track record to see how well they have performed. Those who have been losing money must really change their stock selection method and also their mindset.

All my critics and doubting Thomas must seriously examine their track record to see why they have not been making as much money as they would like people to think. They often criticize what I write to show that they are clever. But they must remember that there are many other smart investors who are laughing at their senseless comments. If they are so good, why don’t they write some articles with their share recommendations for readers to judge them?

As Christmas has just gone by, let me tell you the famous biblical story of Doubting Thomas. About 2015 years ago, according to the Christian Bible, Jesus had 12 apostles. Jesus was crucified on a cross, died and buried. After 3 days, he rose from the death and appeared before his 11 apostles. One of the apostles, called Thomas, who was not present, said that he would not believe unless he put his hand into the spear wound of Jesus. Subsequently Jesus appeared before Thomas and asked him to put his hand into his spear wound.

The point of this story is that after I have a proven track record of my success in share investment and my charity donations, unfortunately there are still a few doubting Thomases who continue to doubt. Can’t you see my sincerity in posting so many articles to help people to improve their investment skill?

In fact, my critics often say that when I recommend any share I want them to buy so that I can sell to make money out of them. Obviously that cannot be true because if I have sold how could their audited annual reports show that I am one of the top shareholders in companies such as VS, Latitude, Lii Hen, CanOne, Chin Well, Focus Lumber and T Guan.

If you look at their price charts, you can see that all of them have gone up a few hundred per cent within the last 2 years. I have been promoting VS for a long time and its 2015 audited annual report shows that I am among the top 5 shareholders, owning more than 100 million Vs shares. Why are my critics so stupid to sell good shares to make me so rich?

For a change, besides making money, my advice to all readers is to focus on gratitude and happiness. Gratitude is perhaps the most important key to finding success and happiness in the modern day. Knowing what we appreciate in life means knowing who we are, what matters to us and what makes each day worthwhile. Paying attention to what we feel grateful for puts us in a positive frame of mind. It connects us to the world around us and to ourselves. Research demonstrates that focusing on what we are grateful for is a universally rewarding way to feel happier and more fulfilled.

All readers must remember that our ultimate aim in life is happiness and we cannot take our money along when we die. I have written in my will that all my money and assets will be donated to charity when I die.

b)

As I said many a time, all investors must examine their track record to see how well they have performed. Those who have been losing money must really change their stock selection method and also their mindset.

All my critics and doubting Thomas must seriously examine their track record to see why they have not been making as much money as they would like people to think. They often criticize what I write to show that they are clever. But they must remember that there are many other smart investors who are laughing at their senseless comments. If they are so good, why don’t they write some articles with their share recommendations for readers to judge them?

As Christmas has just gone by, let me tell you the famous biblical story of Doubting Thomas. About 2015 years ago, according to the Christian Bible, Jesus had 12 apostles. Jesus was crucified on a cross, died and buried. After 3 days, he rose from the death and appeared before his 11 apostles. One of the apostles, called Thomas, who was not present, said that he would not believe unless he put his hand into the spear wound of Jesus. Subsequently Jesus appeared before Thomas and asked him to put his hand into his spear wound.

The point of this story is that after I have a proven track record of my success in share investment and my charity donations, unfortunately there are still a few doubting Thomases who continue to doubt. Can’t you see my sincerity in posting so many articles to help people to improve their investment skill?

In fact, my critics often say that when I recommend any share I want them to buy so that I can sell to make money out of them. Obviously that cannot be true because if I have sold how could their audited annual reports show that I am one of the top shareholders in companies such as VS, Latitude, Lii Hen, CanOne, Chin Well, Focus Lumber and T Guan.

If you look at their price charts, you can see that all of them have gone up a few hundred per cent within the last 2 years. I have been promoting VS for a long time and its 2015 audited annual report shows that I am among the top 5 shareholders, owning more than 100 million Vs shares. Why are my critics so stupid to sell good shares to make me so rich?

For a change, besides making money, my advice to all readers is to focus on gratitude and happiness. Gratitude is perhaps the most important key to finding success and happiness in the modern day. Knowing what we appreciate in life means knowing who we are, what matters to us and what makes each day worthwhile. Paying attention to what we feel grateful for puts us in a positive frame of mind. It connects us to the world around us and to ourselves. Research demonstrates that focusing on what we are grateful for is a universally rewarding way to feel happier and more fulfilled.

All readers must remember that our ultimate aim in life is happiness and we cannot take our money along when we die. I have written in my will that all my money and assets will be donated to charity when I die.

b)

How can investors make money in 2016? Koon Yew Yin

Author: Koon Yew Yin | Publish date: Sat, 26 Dec 2015, 09:06 AM

Many people have asked me this question. In the last 2 festive days, many people told me how I have changed their lives through my charity work and my writing on Malaysian politics and share investment.

One commentator of my recent article said that 99% of the readers like my writing and only 1% do not like. As a writer, I expect some critics and I expect them to do it in a polite manner and not like illiterates or idiots.

Here are some of holdings which still comply with my share selection golden rule even after their prices have gone up quite rapidly. My golden rule is that I must be sure that the company can make more profit this year than last year and the projected P/E ratio is not more than 10.

I advise you to check all the shares you are holding to see that they can comply with my golden rule. Otherwise, you must cut loss and utilize the proceeds to buy better shares.

Can One: It is the largest tin cans and jerry cans manufacturer. It started more than 40 years ago and continues to improve its operation. It bought 146.1 million or 32.9% of Kian Joo shares at Rm 1.65 per share in 2012. The current price of Kian Joo is about Rm 3.30 per share. EPF is one of the 2 parties who have made an offer to buy up Kian Joo. Can One is waiting patiently.

Its 3 quarter EPS ending Sept 2015 was 39 sen and I can safely project its full year EPS to be about 55 because some of its products are sold in US$. Its last closing price was Rm 4.50. It will announce its full year result before end of February 2016.

Chin Well: It is among the largest manufacturers of screws, nuts and bolts in the world. 76% of its products are exported in foreign currencies. After it has acquired the 40% shares from its Vietnamese partners, its latest quarter EPS jumped to 6.07 sen from 4.41 sen. Its last closing price was Rm 1.92 per share.

Thong Guan: It is one of the largest plastic stretch film and bags, raffia stings, drinking straws and paper serviette manufacturers in the Asians region. It started business in 1942.

Its 1st, 2nd and 3rd quarter EPS are 4.4, 6.75 and 10.7 sen respectively. It about 2 months it will have to announce its 4th quarter result. In view of the depressed fossil fuel price, its raw plastic materiel is getting cheaper. What will be its share price when its annual result is announced before end of Feb 2016?

I am also holding VS, Latitude, Lii Hen, Focus Lumber and Ge Shen because they still comply with my golden rule although their share prices have gone up quite rapidly.

I am not asking you to buy any of the shares I mentioned above. But if you buy, you are doing it at your own risk.

7)2015-12-20 19:30

10)

One commentator of my recent article said that 99% of the readers like my writing and only 1% do not like. As a writer, I expect some critics and I expect them to do it in a polite manner and not like illiterates or idiots.

Here are some of holdings which still comply with my share selection golden rule even after their prices have gone up quite rapidly. My golden rule is that I must be sure that the company can make more profit this year than last year and the projected P/E ratio is not more than 10.

I advise you to check all the shares you are holding to see that they can comply with my golden rule. Otherwise, you must cut loss and utilize the proceeds to buy better shares.

Can One: It is the largest tin cans and jerry cans manufacturer. It started more than 40 years ago and continues to improve its operation. It bought 146.1 million or 32.9% of Kian Joo shares at Rm 1.65 per share in 2012. The current price of Kian Joo is about Rm 3.30 per share. EPF is one of the 2 parties who have made an offer to buy up Kian Joo. Can One is waiting patiently.

Its 3 quarter EPS ending Sept 2015 was 39 sen and I can safely project its full year EPS to be about 55 because some of its products are sold in US$. Its last closing price was Rm 4.50. It will announce its full year result before end of February 2016.

Chin Well: It is among the largest manufacturers of screws, nuts and bolts in the world. 76% of its products are exported in foreign currencies. After it has acquired the 40% shares from its Vietnamese partners, its latest quarter EPS jumped to 6.07 sen from 4.41 sen. Its last closing price was Rm 1.92 per share.

Thong Guan: It is one of the largest plastic stretch film and bags, raffia stings, drinking straws and paper serviette manufacturers in the Asians region. It started business in 1942.

Its 1st, 2nd and 3rd quarter EPS are 4.4, 6.75 and 10.7 sen respectively. It about 2 months it will have to announce its 4th quarter result. In view of the depressed fossil fuel price, its raw plastic materiel is getting cheaper. What will be its share price when its annual result is announced before end of Feb 2016?

I am also holding VS, Latitude, Lii Hen, Focus Lumber and Ge Shen because they still comply with my golden rule although their share prices have gone up quite rapidly.

I am not asking you to buy any of the shares I mentioned above. But if you buy, you are doing it at your own risk.

7)2015-12-20 19:30

假如飛機少了一個螺絲,那麼飛機就必須做檢查,以防發生事故。細小的扣件在日常生活中,似乎毫不起眼,但人們的生活卻無法離開它,因為它是結構工程重要的一部份,也因此品質高的螺絲成為了許多行業所重視的小零件。對此,東南亞最大的螺絲製造商又是如何看待這門行業呢?

晉緯控股(CHINWEL,5007,主板工業產品組)董事經理蔡芑雲接受《投資致富》專訪時表示,螺絲小至家具,大至重工業都必須使用它來銜接及穩定物件,因此公司所生產扣件(fastener,螺絲及螺帽一類的統稱)的品質,都可取得客戶的信任。

“公司部份的客戶合作時間甚至長達30年。”

她表示,公司可以和客戶維持那麼長久的關係,主要是公司的品質有保證,且準時交貨,客戶就不必擔心扣件無法如期到手,而展延自身的項目。

蔡芑雲認為,即使產品價格比別人貴,但服務可以比一般人來得好,而賺幅也不會太過份,那麼依然可以還是留得住客戶。

“公司也有一些客戶在更換採購員以後,採購其他公司的扣件,惟他們最終還是會選擇晉緯,因為我們可以提供比別人好的服務。”

經濟放緩

影響不大

影響不大

有關2016年的展望,她表示,公司在大馬的扣件市佔率高達80%至90%左右,因此即使全球經濟放緩,也不會對公司造成太大的影響。

她說,公司目前處於淨現金狀態,且所有的生產線都有盈利,因此未來的營運都暫時並不會面對問題。

她補充,公司未來的淨利多寡,公司40%的股息政策也不會改變。

自助業務料將受惠

“經濟繁榮對公司的營業額肯定可以提高,但經濟處於週期性,那麼公司多少會受到影響,惟賺幅並不會出現太大變化。因為沒有人願意做虧本的生意。”

“經濟放緩時,預期自助(DIY)業務可以取得成長。”

蔡芑雲解釋,歐洲一般喜歡自己動手維修物品,因此經濟不景氣,人們被迫休假時,就會趁機裝潢屋子,屆時扣件的需求將會走高,因此公司可從中受惠。

她表示,公司的客戶還包括了歐洲大型的自助商場。

她說,歐洲客戶對銷售自助產品的製造商有很嚴格的要求,例如製造商是否聘請童工、工作環境是否符合條件、員工待遇是否符合人道主義等等。

“只有符合上述的條件,才可在自助商場銷售。當然,如此嚴格的要求,公司也可以享有較好的賺幅。”

蔡芑雲透露,公司目前也正在和宜家洽談供應扣件的合作。

“若洽談成功,公司和宜家間接合作的關係將轉換成直接合作。”

她補充,公司一路以來和宜家的供應商都有合作的關係。

每月產能達6500噸

詢及產能方面,蔡芑雲表示,連越南的產能也算在內,公司每個月的扣件產能高達6千500噸左右。目前,大馬的工廠面對員工不足的問題,因此無法再提高產能。

“人力資源問題不能解決,公司有意增產也有心無力,希望有關單位可以正視相關問題並解決。”

看好籬笆網石籠網業務發展

蔡芑雲說,除了原有的扣件業務以外,公司也涉足籬笆網及石籠網(Gabion)。

她看好這兩項業務並表示,公司生產的籬笆,可用在火車軌道旁邊,防止人們攀爬。她說,對比同儕,公司生產的籬笆品質比較高,且不需要太多支柱。

“在特定的距離原本需要10根支柱,但公司生產的籬笆並不需10根支柱,也能支撐籬笆,那麼圍籬的成本就可降低許多了。”

她也表示,公司並沒有涉足生產火車的扣件,但預期印尼及馬新高鐵建造,其軌道需要籬笆圍籬,數以百計公里的火車軌道,公司應該可以受惠。

此外,蔡芑雲也表示,現代人重視居住環境的保安,公司的籬笆也適用於住宅社區。

至於石籠網業務,她表示,石籠網主要用於防止土壤侵蝕,主要用於公路兩側及河流,可防止土崩,該產品也適用於河流兩岸及礦業。

馬幣貶值

內外銷皆受惠

內外銷皆受惠

有關跨太平洋夥伴關係協議(TPPA),蔡芑雲表示,該協議理論上可讓公司受惠,但政府相關細則並沒有公佈,因此現在無法給予任何意見。

有關馬幣走弱方面,她表示,公司出口業務可受惠其中,內銷方面也相應提高了。

“部份商家從海外進口扣件,但目前匯率的波動,商家可能無法取得理想的利潤,因此商家紛紛轉向公司進貨。”

大宗商品價格目前處於疲弱的狀態,有助於晉緯控股的原料成本,蔡芑雲也表示,即使大宗商品價格回揚,也不會造成太大的影響,因為公司的原材料足以支撐未來3個月的營運。

(星洲日報/投資致富‧企業故事‧文:謝汪潮)

8)

Stock With Momentum: Chin WellThis article first appeared in The Edge Financial Daily, on December 22, 2015.

[url=]Chin Well Holdings Bhd[/url] ( Valuation: 2.00, Fundamental: 2.40) (-ve)

Valuation: 2.00, Fundamental: 2.40) (-ve)

SHARES of Chin Well (Fundamental: 2.4/3, Valuation: 2/3) have put on an impressive performance since announcing its quarterly earnings on November 26. The stock has gained 13.6% to close at RM1.92 on Monday, with 3.5 million shares changing hands.

Meanwhile, Tsai Yung Chuan (Chin Well’s largest shareholder and managing director) upped his stake in the company to 54.2% from 52.9% on November 27. This came after Mr. Tsai acquired a block of 3.9 million shares at RM1.54 per share in an off-market trade via a private vehicle, [url=]Benua Handal Sdn Bhd[/url].

Chin Well is one of the world’s largest manufacturers of carbon steel fasteners and wire products. Europe was the company’s largest market in FYJun2015, contributing 56% of sales. This was followed by Malaysia (22%), with the balance from Vietnam and other countries.

The stock currently trades at a trailing P/E ratio of 11.5 times and 1.2 times book.

[url=]Chin Well Holdings Bhd[/url] (

SHARES of Chin Well (Fundamental: 2.4/3, Valuation: 2/3) have put on an impressive performance since announcing its quarterly earnings on November 26. The stock has gained 13.6% to close at RM1.92 on Monday, with 3.5 million shares changing hands.

Meanwhile, Tsai Yung Chuan (Chin Well’s largest shareholder and managing director) upped his stake in the company to 54.2% from 52.9% on November 27. This came after Mr. Tsai acquired a block of 3.9 million shares at RM1.54 per share in an off-market trade via a private vehicle, [url=]Benua Handal Sdn Bhd[/url].

Chin Well is one of the world’s largest manufacturers of carbon steel fasteners and wire products. Europe was the company’s largest market in FYJun2015, contributing 56% of sales. This was followed by Malaysia (22%), with the balance from Vietnam and other countries.

The stock currently trades at a trailing P/E ratio of 11.5 times and 1.2 times book.

9)

Chin Well Holding Berhad (Recession Proof Exporter)

Chin Well Holdings Berhad (CWHB) is a Malaysia-based investment holding company. The Company, through its subsidiaries operates in three segments: fastening products, which include the manufacturing and trading of screws, nuts, bolts and other fastening products; wire products, which include the manufacturing of precision galvanized wire, annealing wire, hard drawn wire, polyvinyl chloride (PVC) wire, bent round bar and BRC wire mesh, and investment holding.

Excluding Malaysia & Vietnam (main factory) which business is dominated in local currency (MYR, VND), Chin Well remaining 74.8% business is export, which is mainly dominated in Euro & USD. A recent appreciation in EURO and USD contributes a positive impact on the company in term of profit margin. While on the other hand, most of their costs are source locally, which promises a better earning prospect for FY16.

Key Ratio and Statistics

· Total Asset RM571.5 million, Total Liabilities RM123.5 million, Total Equities RM448 million

· Cash Per-Share RM0.19

· Zero gearing/ Net cash, note that Chin Well finally turn into a net cash company in FY15 (note that, the company make an effort to reduce company gearing yearly)

· Book Value Per-share RM1.58, Price to book value 0.90 times, which is very low (based on current price 1.42)

· Reserves which is qualified for 1 for 1 bonus issue

· Price to earning 10.3 times (based on current price 1.42)

· Debt to Equity ratio 0.27x

· Return on Equity 9.3x

· Dividend Pay-out policy 40%

Chin Well (Completing they cycle of European recovery)

Chin Well business possesses its own defensive unique. In almost every major sector in the economy (automotive, construction, property development, furniture, oil & gas, technology) consumes Chin Well products. Based on the revenue breakdown above, we can see more than 56% of Chin Well products are exported to the European countries. While the extension of EU anti-dumping duty to the china fastener manufacturer for 5 years (March2015- March2020), grant Chin Well a big favor in term of business market share, as it is one of the eight companies in Malaysia that is exempted from this regulations.

The recent drop in the steel price furthermore boosts the company profit margin, as the raw material is accounted for 70% of its production cost. ECB Quantitative Easing, continues to spur European economic growth, and it is deems a great opportunity for the company to position itself for a greater and a better FY16 prospects.

As according to the Executive Director Tsai Chia Ling, GST effect does them a favor as they could save up 4% of the tax rate as their current sales tax is at 10%. Other than that, according to her, Chin Well Vietnam plant operates at 90% capacity while Malaysia plant 50% capacity, which literally gives them an opportunity to cater their customer upcoming demand.

Recap

Chinwel, is a lagging exporter company yet to be discovered, Net cash with good dividend yield and amazing future prospect.

Chin Well Holding Berhad (Recession Proof Exporter)

Author: Keithson Neoh | Publish date: Mon, 28 Sep 2015, 02:51 PM

Chin Well Holding Berhad (Recession Proof Exporter)

Chin Well Holdings Berhad (CWHB) is a Malaysia-based investment holding company. The Company, through its subsidiaries operates in three segments: fastening products, which include the manufacturing and trading of screws, nuts, bolts and other fastening products; wire products, which include the manufacturing of precision galvanized wire, annealing wire, hard drawn wire, polyvinyl chloride (PVC) wire, bent round bar and BRC wire mesh, and investment holding.

Excluding Malaysia & Vietnam (main factory) which business is dominated in local currency (MYR, VND), Chin Well remaining 74.8% business is export, which is mainly dominated in Euro & USD. A recent appreciation in EURO and USD contributes a positive impact on the company in term of profit margin. While on the other hand, most of their costs are source locally, which promises a better earning prospect for FY16.

| Key Statistic (Millions) |

2013

|

2014

|

2015

|

| Cash and Equivalent |

30.70

|

47.93

|

55.16

|

| Total Asset |

549.25

|

556.74

|

571.55

|

| Total Liabilities |

144.27

|

117.14

|

123.55

|

| Borrowings |

85.46

|

73.14

|

53.01

|

| Shareholders Fund |

404.98

|

439.60

|

448.00

|

| Book Value Per share |

1.30

|

1.39

|

1.58

|

| Net Cash |

(54.76)

|

(25.21)

|

2.15

|

| Cash Per share |

0.11

|

0.17

|

0.19

|

| NTAPS |

1.30

|

1.39

|

1.58

|

| Total share outstanding |

272.53

|

272.53

|

283.51

|

Key Ratio and Statistics

· Total Asset RM571.5 million, Total Liabilities RM123.5 million, Total Equities RM448 million

· Cash Per-Share RM0.19

· Zero gearing/ Net cash, note that Chin Well finally turn into a net cash company in FY15 (note that, the company make an effort to reduce company gearing yearly)

· Book Value Per-share RM1.58, Price to book value 0.90 times, which is very low (based on current price 1.42)

· Reserves which is qualified for 1 for 1 bonus issue

· Price to earning 10.3 times (based on current price 1.42)

· Debt to Equity ratio 0.27x

· Return on Equity 9.3x

· Dividend Pay-out policy 40%

Chin Well (Completing they cycle of European recovery)

Chin Well business possesses its own defensive unique. In almost every major sector in the economy (automotive, construction, property development, furniture, oil & gas, technology) consumes Chin Well products. Based on the revenue breakdown above, we can see more than 56% of Chin Well products are exported to the European countries. While the extension of EU anti-dumping duty to the china fastener manufacturer for 5 years (March2015- March2020), grant Chin Well a big favor in term of business market share, as it is one of the eight companies in Malaysia that is exempted from this regulations.

The recent drop in the steel price furthermore boosts the company profit margin, as the raw material is accounted for 70% of its production cost. ECB Quantitative Easing, continues to spur European economic growth, and it is deems a great opportunity for the company to position itself for a greater and a better FY16 prospects.

As according to the Executive Director Tsai Chia Ling, GST effect does them a favor as they could save up 4% of the tax rate as their current sales tax is at 10%. Other than that, according to her, Chin Well Vietnam plant operates at 90% capacity while Malaysia plant 50% capacity, which literally gives them an opportunity to cater their customer upcoming demand.

Recap

Chinwel, is a lagging exporter company yet to be discovered, Net cash with good dividend yield and amazing future prospect.

10)

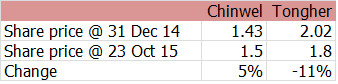

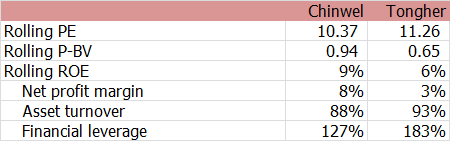

Deep value in fastener sector: Chinwel & Tongher

Author: angiegoh | Publish date: Sat, 24 Oct 2015, 12:00 AM

To me, personally, I acquire new knowledge through stock investment almost everyday.

It is fortunate to have helpful forum members like JTYeo, Noby and KcChong.

Now we are on the same page.

Fastener sector

Fasterners are a hardware device that mechanically joins objects together.

They are used in industry, commerce, and household. Therefore, there is sustainable demand for fasterners.

Raw materials for fasteners include stainless steel, aluminium, and copper. Prices of these raw materials have been declining, and touched a base of five-year low.

Most Malaysian made fasterners are exported to the West. Local fastener companies should benefit from RM depreciation.

There is a good chance that Chinwel and/or Tongher offer a deep value investing idea.

Stock performance of companies

It seems like investors have, so far, disagreed with the prospect of both fastener companies.

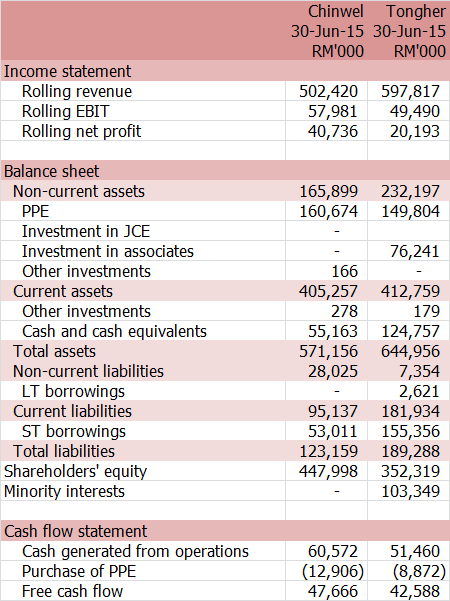

Financial statements and simple anlyses

It is noted that Tongher's net profit in the latest quarter was affected by the negative earnings of its associate.

Theoretically, companies should not consolidate the share of results (profit/loss) of associates (with only 30% shareholding) in their incme statement. However, many companies do so and 'wash' their net profit.

Consequently, the reported net profit does not reflect the operating profit of a particular company.

We, in deep value investing, focus on the cleanest operating profit (EBIT) that derived purely from the company's operating business.

Note: 6-month cash flow is used here.

Note: 6-month cash flow is used here.

Investors are concerned about their USD denominated borrowings. Their ability to meet the obligation is, of course, backed up by their healthy financial position and on-going free cash flow.

For Chinwel, its USD currency loans were reduced from USD73.138 mil (as at 30 June 14) to USD53.011 mil (as at 30 June 2015).

For Tongher, its USD currency loans were parred down from USD48.30 mil (as at 30 June 14) to USD40.98 mil (as at 30 June 2015).

In addtion, these two companies have used forward exhange contracts to protect them from fluctuations in currency pries. As stipulated in the contracts, Chinwel and Tongher agree to buy or sell a certain amount of foreign currency on a specific future date.

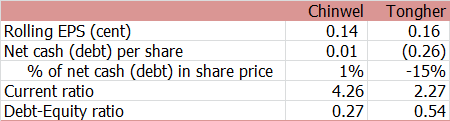

Simple valuation

At first, based on PE ratios, Tongher seems to be more expensive in transacton for lower ROE.

Nevertheless, Price-Book Value ratios suggest otherwise.

The contradiction prompts us to compare the two companies on a standard basis without being affected by their capital structures.

Deep valuation

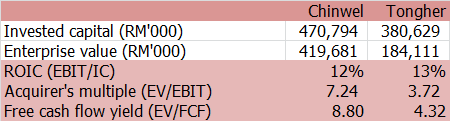

Now it is clearer.

Tongher's invested capital is smaller, and it is more efficient in employing its invested capital to generate ROIC 13%.

Most importantly, Tongher remains cheap. It is trading at Acquirer's Multiple 3.72 or Earnings Yield 27%.

Its 'cheapness' is reinforced by the inverse of free cash flow yield: Tongher is now selling, at a steep discount, of approximately 50% of Chinwel's valuation. The estimate (4.32) also suggests that Tongher can pay back our cost of acquisition or generate cash to reinvest in its business at a significant faster pace than Chinwel.

All these evidences perhaps explain why Tongher bought back 750,300 units of its stock in the open market from 1 Sept to 7 Oct 2015.

11)

12)darvinmk 网友的分享--(谢谢他的功课)

我也来推荐

跟北极一样冷的冷门股

全马最大的碳钢螺丝 (carbon steel fastener)生产商

5007

1. 开始计入越南厂房100%的贡献(原先为60%),视为长期利好。

2. 欧洲刚延长对中国反倾销制裁5年

3. 年初马来西亚产房因外劳申请成功有望提高产能,之前槟城产房使用率为大约46%-47%

4. 赚幅相对高的防剪篱笆年初开始贡献盈利

5. 管理层为台湾人,母公司晉億集团或晉禾http://www.jinnher.com.tw/about_29.html在台湾为数一数二的螺丝界龙头,是务实的商人

http://www.gvm.com.tw/Boardcontent_19701.html

6. div policy为40%,div yield换算到来未来将超过3.5%

7. GST实施以后没多久公司就已经表示订单提高六倍。

到今天7月头就不知道会到多少了。GST对公司的影响是视为长期的利好。

马来西亚目前占营业额24%。6倍是很可观的数字。

http://biz.sinchew.com.my/node/113471?tid=6

8. DIY市场赚幅较高,贡献在增长中,而且由刚全面收购的越南产房生产

9. 最新的财报出现了不少机构投资者大略计算从4家增加到8家,其中包括bank negara trust fund

credit suisse从1,125,000(0.41%)加码到4,027,600(1.48%),可谓基本面强稳

10. 目前PE 为大约11,似乎未反应未来的潜能

我用了蛋散叔推荐的fcfe formula来计算10年cash flow。

假设未来公司现金流的成长纯粹赶得上通膨。此股也值1.69,目前股价为1.55

基于尚未计入未来增长的潜力和目前净现金 RM 7,036,000 的健康水平

我认为此股的潜力尚未被发掘

It is fortunate to have helpful forum members like JTYeo, Noby and KcChong.

Now we are on the same page.

Fastener sector

Fasterners are a hardware device that mechanically joins objects together.

They are used in industry, commerce, and household. Therefore, there is sustainable demand for fasterners.

Raw materials for fasteners include stainless steel, aluminium, and copper. Prices of these raw materials have been declining, and touched a base of five-year low.

Most Malaysian made fasterners are exported to the West. Local fastener companies should benefit from RM depreciation.

There is a good chance that Chinwel and/or Tongher offer a deep value investing idea.

Stock performance of companies

It seems like investors have, so far, disagreed with the prospect of both fastener companies.

Financial statements and simple anlyses

It is noted that Tongher's net profit in the latest quarter was affected by the negative earnings of its associate.

Theoretically, companies should not consolidate the share of results (profit/loss) of associates (with only 30% shareholding) in their incme statement. However, many companies do so and 'wash' their net profit.

Consequently, the reported net profit does not reflect the operating profit of a particular company.

We, in deep value investing, focus on the cleanest operating profit (EBIT) that derived purely from the company's operating business.

Note: 6-month cash flow is used here.Investors are concerned about their USD denominated borrowings. Their ability to meet the obligation is, of course, backed up by their healthy financial position and on-going free cash flow.

For Chinwel, its USD currency loans were reduced from USD73.138 mil (as at 30 June 14) to USD53.011 mil (as at 30 June 2015).

For Tongher, its USD currency loans were parred down from USD48.30 mil (as at 30 June 14) to USD40.98 mil (as at 30 June 2015).

In addtion, these two companies have used forward exhange contracts to protect them from fluctuations in currency pries. As stipulated in the contracts, Chinwel and Tongher agree to buy or sell a certain amount of foreign currency on a specific future date.

Simple valuation

At first, based on PE ratios, Tongher seems to be more expensive in transacton for lower ROE.

Nevertheless, Price-Book Value ratios suggest otherwise.

The contradiction prompts us to compare the two companies on a standard basis without being affected by their capital structures.

Deep valuation

Now it is clearer.

Tongher's invested capital is smaller, and it is more efficient in employing its invested capital to generate ROIC 13%.

Most importantly, Tongher remains cheap. It is trading at Acquirer's Multiple 3.72 or Earnings Yield 27%.

Its 'cheapness' is reinforced by the inverse of free cash flow yield: Tongher is now selling, at a steep discount, of approximately 50% of Chinwel's valuation. The estimate (4.32) also suggests that Tongher can pay back our cost of acquisition or generate cash to reinvest in its business at a significant faster pace than Chinwel.

All these evidences perhaps explain why Tongher bought back 750,300 units of its stock in the open market from 1 Sept to 7 Oct 2015.

11)

PublicInvest Research Headlines - 28 Sep 2015

Chin Well: Sees rising domestic demand for its fasteners. Chin Well Holdings sees domestic demand for its construction grade fasteners growing as a result of the weakened ringgit. Group ED Tsai Chia-Ling said the hardware wholesalers in the country used to order from China. “But with the weakened ringgit, it has become more expensive for them to order from overseas. They have turned to us for their supplies.” (StarBiz)

12)darvinmk 网友的分享--(谢谢他的功课)

我也来推荐

跟北极一样冷的冷门股

全马最大的碳钢螺丝 (carbon steel fastener)生产商

5007

1. 开始计入越南厂房100%的贡献(原先为60%),视为长期利好。

2. 欧洲刚延长对中国反倾销制裁5年

3. 年初马来西亚产房因外劳申请成功有望提高产能,之前槟城产房使用率为大约46%-47%

4. 赚幅相对高的防剪篱笆年初开始贡献盈利

5. 管理层为台湾人,母公司晉億集团或晉禾http://www.jinnher.com.tw/about_29.html在台湾为数一数二的螺丝界龙头,是务实的商人

http://www.gvm.com.tw/Boardcontent_19701.html

6. div policy为40%,div yield换算到来未来将超过3.5%

7. GST实施以后没多久公司就已经表示订单提高六倍。

到今天7月头就不知道会到多少了。GST对公司的影响是视为长期的利好。

马来西亚目前占营业额24%。6倍是很可观的数字。

http://biz.sinchew.com.my/node/113471?tid=6

8. DIY市场赚幅较高,贡献在增长中,而且由刚全面收购的越南产房生产

9. 最新的财报出现了不少机构投资者大略计算从4家增加到8家,其中包括bank negara trust fund

credit suisse从1,125,000(0.41%)加码到4,027,600(1.48%),可谓基本面强稳

10. 目前PE 为大约11,似乎未反应未来的潜能

我用了蛋散叔推荐的fcfe formula来计算10年cash flow。

假设未来公司现金流的成长纯粹赶得上通膨。此股也值1.69,目前股价为1.55

基于尚未计入未来增长的潜力和目前净现金 RM 7,036,000 的健康水平

我认为此股的潜力尚未被发掘

13)

(Icon8888) Chin Well (Part 2) - Other People's Indifference Could Be Our Opportunity

http://klse.i3investor.com/blogs/icon8888/68308.jsp

Executive Summary

On 5 November 2014, the company announced the acquisition of the remaining 40% of its Vietnam subsidiary through issuance of 27 mil new shares (at RM1.45) and RM8 mil cash. The acquisition was completed on 31 December 2014.

The acquisition will enhance Chin Well's EPS immediately. This is because Chin Well issued new shares at PER of 11.5 times to acquire the remaining 40% at PER of 5.5 times. The Vietnam subsidiary reported net profit of RM21 mil in latest financial year.

On top of that, Chin Well exports the bulk of its products. As such, it should benefit from the strong US Dollars.

(Chin Well share price)

1. Background Information

Chin Well is principally involved in the manufacturing and trading of the following :-

(a) fasterners (essentially screws, bolts and nuts); and

(b) security fence & gabions

(Security fence)

(Gabions)

The company has market cap of RM450 mil (based on 300 mil shares and RM1.50 share price).

Based on past 12 months adjusted net profit of RM44 mil (after factoring in effect of acquisition, being RM35.6 mil + RM21 mil x 0.4 = RM35.6 mil + RM8.4 mil), historical PER is approximately 10 times.

The group has strong balance sheets. With net assets of RM383 mil, loans of RM80 mil and cash of RM65 mil, net gearing is 4% only.

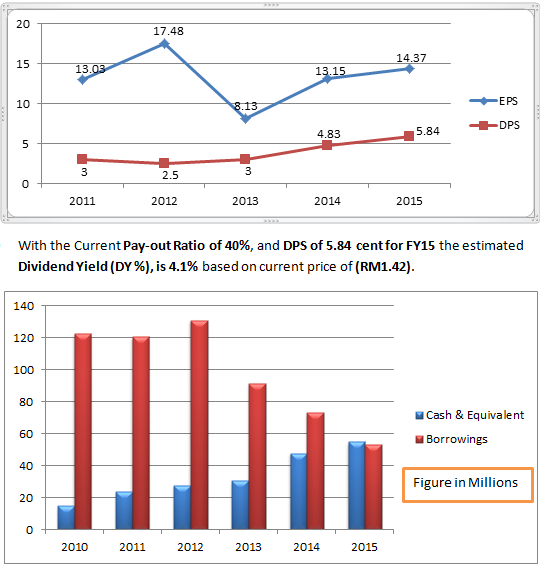

The company paid out dividend of 4.83 sen per share over past twelve months. Dividend yield works out to be approximately 3.2%.

2. Export Oriented

FY2014 revenue based on geographical location of customers is as follows :-

As can be seen from table above, approximately 24% of products are sold domestically while the remaining 76% are exported.

3. Major Shareholder Increased Shareholdings Recently

On 19 September 2014, the Tsai family acquired additional 22 mil shares via an off market transaction, thereby increased its shareholding from 51% to 58%.

4. Concluding Remarks

I first wrote about Chin Well in July 2014. Kindly refer to that article to better understand the group's operation and the various factors that affect its profitability.

The purpose of me writing Part 2 is to provide an update of the Group in view of its recent acquisition. In my opinion, it was a transaction that should have material positive impact on the group's earnings.

One thing that also attracted me to take a re-look is because the group exports the bulk of its products. The recent weakening of Ringgit should benefit the group either through margin expansion or increase in volume (due to pricing competitiveness).

A word of caution though - there is no information in quarterly / annual reports regarding what currency the group's sale is denominated in. The US Dollar has strengthened against the Ringgit recently, but Euro is in quite a mess. So please do your own homework before jumping in (of course, if you bump into any relevant information, please feel free to share it with all of us. Thanks in advance).

Have a nice day.

Author: Icon8888 | Publish date: Tue, 13 Jan 13:09

http://klse.i3investor.com/blogs/icon8888/68308.jsp

Executive Summary

On 5 November 2014, the company announced the acquisition of the remaining 40% of its Vietnam subsidiary through issuance of 27 mil new shares (at RM1.45) and RM8 mil cash. The acquisition was completed on 31 December 2014.

The acquisition will enhance Chin Well's EPS immediately. This is because Chin Well issued new shares at PER of 11.5 times to acquire the remaining 40% at PER of 5.5 times. The Vietnam subsidiary reported net profit of RM21 mil in latest financial year.

On top of that, Chin Well exports the bulk of its products. As such, it should benefit from the strong US Dollars.

(Chin Well share price)

1. Background Information

Chin Well is principally involved in the manufacturing and trading of the following :-

(a) fasterners (essentially screws, bolts and nuts); and

(b) security fence & gabions

(Security fence)

(Gabions)

The company has market cap of RM450 mil (based on 300 mil shares and RM1.50 share price).

Based on past 12 months adjusted net profit of RM44 mil (after factoring in effect of acquisition, being RM35.6 mil + RM21 mil x 0.4 = RM35.6 mil + RM8.4 mil), historical PER is approximately 10 times.

The group has strong balance sheets. With net assets of RM383 mil, loans of RM80 mil and cash of RM65 mil, net gearing is 4% only.

The company paid out dividend of 4.83 sen per share over past twelve months. Dividend yield works out to be approximately 3.2%.

2. Export Oriented

FY2014 revenue based on geographical location of customers is as follows :-

As can be seen from table above, approximately 24% of products are sold domestically while the remaining 76% are exported.

3. Major Shareholder Increased Shareholdings Recently

On 19 September 2014, the Tsai family acquired additional 22 mil shares via an off market transaction, thereby increased its shareholding from 51% to 58%.

4. Concluding Remarks

I first wrote about Chin Well in July 2014. Kindly refer to that article to better understand the group's operation and the various factors that affect its profitability.

The purpose of me writing Part 2 is to provide an update of the Group in view of its recent acquisition. In my opinion, it was a transaction that should have material positive impact on the group's earnings.

One thing that also attracted me to take a re-look is because the group exports the bulk of its products. The recent weakening of Ringgit should benefit the group either through margin expansion or increase in volume (due to pricing competitiveness).

A word of caution though - there is no information in quarterly / annual reports regarding what currency the group's sale is denominated in. The US Dollar has strengthened against the Ringgit recently, but Euro is in quite a mess. So please do your own homework before jumping in (of course, if you bump into any relevant information, please feel free to share it with all of us. Thanks in advance).

Have a nice day.

14)

没有评论:

发表评论