--个人浅见,rm0. 685于上周五是低位了,除非油价大跌不然沒机会了,主力与基金将进入,因私募价为rm0.695 ,

一般上拉升几分属平常的。買进与守住待丰收。

--回调于低成交量,飞漲高成交量属正常,私募股rm0.695 ,rm0.70是关点支持,沒跌破且不易。

收住待收购成就过rm0.80了。

--简单想吧,私募价rm0.695,公开市场价如何都会高过rm0.75才会吸引買家购買公司股份,

長线会高过rm1。至今己有三家投行推介hibiscs 了,大众目標价为rm1.06 ,回银为rmo.85,

大马銀行为rm0.81,大莊与基金坐陣达標机率大。

--大众,回数,大马銀行 做莊有信心,大红花朵朵开油气來,

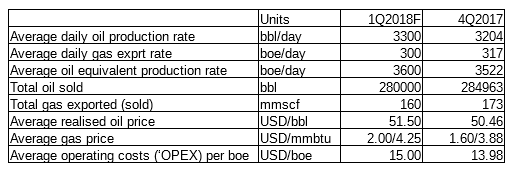

收购成北沙巴油田后,每日生产12500桶原油,这笔帳不少哦。

--忍不住就会被洗出去了,哈哈哈!此股莊家历害,但有三家投行推介作后盾,不怕,随时会射上然后公布收购成功,

公司市值达10亿马币,对一亿的北沙巴油田收购案不成问題。

--利好:

1)最大石油出口国沙地国王己开声,现石油生产无过剩问题,沙特阿美上市。

2)伊拉克,伊郎,利比亞,尼日利亞,委内瑞拉等存在地缘,内乱问题,使生产出现一些停顿。

3)全球第一,第三石油消费国(中国:每天用8百多万桶,印度:每日4百多万桶)的经济向好,须求上升。

4)Opec 的减产延長至2018年底机率大 。

--hibiscs 走势呈荣景至5 Dec 2018 的股东大会,到时想信会宣佈北沙巴油田收购与否,现股价73仙是未反应成功收购,成功的话股价过85仙,就算收购不成股价也近70仙,因布仑特油价己在60usd,大致上Am bank 推介价81仙我己看到,回教銀行推介的85仙紧跟着,大众的rm1.06 将隨公司净利与原油价上升做决定,非常乐观。

只是分享,投资请三思且自负。

http://www.bursamalaysia.com/market/listed-companies/company-announcements/5575073

--http://kongsenger.blogspot.my/2017/09/5199-hibiscus-rm-0615.html

--*STOCKS ON RADAR - 26 October 2017*

*AmBank Retail Research*

*Hibiscus Petroleum (5199)*

Buy uptrend continuation above RM0.70

Target: RM0.755, RM0.81 (time frame: 3-6 weeks)

Exit: RM0.605

*Hibiscus Petroleum (5199)*

Buy uptrend continuation above RM0.70

Target: RM0.755, RM0.81 (time frame: 3-6 weeks)

Exit: RM0.605

木槿花石油以2500万美元(约1亿零46万3000令吉)收购2011年沙巴北部油田产能复苏共享合约50%股权,已经获国油勘探(PCSB)及国家石油首肯。

(吉隆坡29日讯)木槿花石油(HIBISCS,5199,主板工业产品组)以2500万美元(约1亿零46万3000令吉)收购2011年沙巴北部油田产能复苏共享合约50%股权,已经获国油勘探(PCSB)及国家石油首肯.

该公司发文告通知,国油勘探免除联合营运合约的先购权。与此同时,国油也批准蚬壳石油转移国油勘探的营运权给买家Sea Hibiscus私人有限公司。

此批准是根据卖家及Sea Hibiscus检视后的一些状况后作出的决定,若国油还需进一步厘清这些状况,该公司将再作出宣布。

木槿花石油视此为正面进展,鉴于还需以厘清状况,管理层预计,此收购将2017年第二季完成。

文章来源:

星洲日报‧财经‧2017.05.29

a)--Oil rises on tighter fundamentals

Read more at http://www.thestar.com.my/business/business-news/2017/10/21/oil-rises-on-tighter-fundamentals/#MogpuozDMB4C9b2c.99

B)

布伦特原油站上60美元关口 一个重要“玩家”回归

布伦特原油周五站上60美元关口,这是逾两年来首次。究其原因,除沙特力撑延长减产提供了支撑外,还可能是因为油市近日不太平。摩根士丹利指出,有一个“玩家”正在重新回归,油市前景由此将变得愈加复杂。

周六,布伦特原油不负众望在美市盘中站上60美元/桶关口,续刷2015年7月新高。

除了OPEC和沙特一如既往地表态支持延长减产协议外,油价上涨还可能是因为油市近日不太平:先是伊拉克与库尔德地区的争端一度发酵助推油价;而随着基尔库克一个油田恢复出口令该利好因素逐渐消失,又传出美国众议院通过对伊新制裁的消息。另一方面,委内瑞拉债务违约已经步入24小时倒计时……

再过不到24小时,委内瑞拉可能就要违约了

据彭博社周五(10月27日)报道,委内瑞拉石油公司(PDVSA)所欠的8.42亿美元债务将于27日到期。与正常的债务偿还不一样的是,PDVSA这笔债务并没有30日的宽限期。而在随后的11月2日,该公司还有11亿美元的债务到期,同样没有宽限期。

之前,在委国债务偿还临近截止期限时,媒体都会报道PDVSA将如期付款,该公司随后亦会发布新闻稿确认。但是目前为止PDVSA和委国政府仍然保持缄默,这令该国债市陷入恐慌。PDVSA于2020年到期的美元债券价格周四跌超4美分,收益率大涨逾2%至17.3%。

彭博预测,接下来最有可能出现的情形是,PDVSA或发表声明,称他们已经向债务持有人付款,但因为支付过程中出现问题导致无法准时到账,并将原因归咎于美国方面的制裁。特朗普曾于8月25日签署行政命令,禁止各方参与委国政府和PDVSA的新债券及证券发售交易。不过,如果债务持有人在三日内未收到还款,他们仍可以宣布委国违约。

美银美林主权债务分析师布劳尔(Jane Brauer)称,委内瑞拉短期内违约的可能性已经“大幅上升”。而Caracas Capital Markets执行董事达伦(Russ Dallen)表示,如果PDVSA周五违约,也许该国包括国债在内的所有债务都会跟着违约。信用违约互换数据显示,在未来的12个月内,PDVSA的违约概率为75%,未来5年违约率将达99%。

债务违约、国外制裁或令委内瑞拉原油生产状况雪上加霜。由于经济萎缩、国家石油公司投资不足和缺乏管理,委内瑞拉的原油产量已经降至近30年以来的最低水平。花旗银行周三在报告中指出,截至9月,委内瑞拉的石油产量仅为189万桶/日,远低于上世纪90年代末的320万桶/日,也低于2015年的近240万桶/日。如果没有资金,PDVSA就不能投资新产品,甚至不能维持设施的日常维护以防止现有产量下滑。有报道称,即使是生产出来的委内瑞拉石油也受到了质量下降的困扰,因为PDVSA无法妥善处理其重质原油。

地缘政治风险“重返赛场”

无论是此前的伊拉克,还是现在的伊朗、委内瑞拉,所有消息都在暗示着油市的一个新进展:地缘政治风险溢价重新回归。摩根士丹利本周就在报告中指出,近几年的持续供应过剩一度令市场对地缘政治风险的敏感度大大降低,但是从现在开始,油市的前景会因为这个因素变得更加复杂。

大摩的全球石油策略师拉茨(Martijn Rats)指出,年初以来,OPEC和非OPEC等主要产油国以前所未有的极高执行力度推行减产计划,对全球原油库存降至五年均值的目标起到了一定的作用,油市已经逐渐迈向再平衡。这就意味着原油市场中的“缓冲区间”变窄,油价在面对供应波动时会更加容易受到影响。

拉茨继续指出,地缘政治风险和供应波动的联系已变得紧密起来。他预计,目前布伦特原油价格计入了每桶1-2美元的地缘政治风险因素,即相当于计入了市场关于未来大约有4000万-6000万桶供应将因地缘政治事件而受到干扰的预期。换言之,油市投资者是时候需要更加密切地关注地缘政治风险方面的消息了。

C)

投资者认定支持减产国家越来越多 原油飙至8个月高点

摘要:美东时间周五,因沙特王储穆罕默德·本·萨尔曼表示,沙特将支持延长减产,而在几周前,俄罗斯总统普京也表示,他支持将减产协议延长至2018年的想法,缓解了此前市场投资者对由伊拉克政局可能引发的全球石油供应过剩局面的担忧,随后原油价格达到了今年3月以来的最高点,投资者获得了迄今最强烈的信号,即支持长期减产的OPEC成员国正在增加。

美东时间周五,因沙特王储穆罕默德·本·萨尔曼表示,沙特将支持延长减产,而在几周前,俄罗斯总统普京也表示,他支持将减产协议延长至2018年的想法,缓解了此前市场投资者对由伊拉克政局可能引发的全球石油供应过剩局面的担忧,随后原油价格达到了今年3月以来的最高点,投资者获得了迄今最强烈的信号,即支持长期减产的OPEC成员国正在增加。

周五(10月27日),在沙特阿拉伯王储穆罕默德·本·萨尔曼发表乐观评论后,原油价格走高,原因是预期OPEC将同意在2018年3月之前延长减产。

原油价格达到了今年3月以来的最高点,投资者获得了迄今最强烈的信号,即支持长期减产的OPEC成员国正在增加。目前美国WTI原油价格至53.90美元/桶,而ICE布伦特原油价格至60.40美元/桶。

此前,沙特王储穆罕默德·本·萨尔曼周四对路透社表示,沙特将支持延长减产,以消除市场上的供应过剩。

今年5月,OPEC同意将减产期延长9个月至3月,但仍坚持去年11月达成的减产120万桶。俄罗斯总统普京在几周前表示,他支持将减产协议延长至2018年的想法,缓解了外界对伊拉克和库尔德武装军队同意停火后全球减产的担忧,从而减少了供应中断的可能性。

与此同时,在美国,投资者们对显示石油钻井平台数量上升的数据进行了反复思考,并连续三周出现下跌。

油田服务公司贝克休斯周五表示,每周在美国运营的石油钻井平台数量增加了1个,达到737个。每周的钻机数量是钻井行业的一个重要晴雨表,它是石油生产和石油服务需求的代表。

D)

美油布油双双大涨 OPEC及俄罗斯均暗示延长减产协议

截止收盘,美国WTI 12月原油期货收涨1.26美元,涨幅2.39%,报53.90美元/桶,为3月初以来高位。

布伦特12月原油期货收涨1.14美元,涨幅1.92%,报60.44美元/桶,创2015年7月初以来收盘新高。

【相关阅读】

周四,沙特王储萨勒曼接受采访时表示,为了稳定市场,石油出口国需要延长减产,这意味着减产协议可能再次延长9个月。

在被问及沙特是否会支持将减产协议延长至2018年3月之后时,萨勒曼称,“我们致力于与所有产油国,不管是欧佩克还是非欧佩克产油国合作,我们已达成一项伟大而且是历史性的协议,我们将支持任何稳定油市供需的做法。”

几周之前,俄罗斯总统普京也表示,暂时支持延长减产,这表明沙特和俄罗斯都准备好继续合作,以减少原油供应并提高能源价格。

如果在OPEC下个月的会议上得到确认,减产协议延长可能会进一步提振油价。石油输出国组织(OPEC)及俄罗斯等其他10个产油国自今年1月起每日减产约180万桶,该协议明年3月到期,但他们正考虑延长协议。

OPEC下一次会议将在11月30日于维也纳举行。

“这似乎是我们看到的上涨势头的延续。市场对原油的整体看法略微更加积极,”Stratas Advisors驻纽约的石油分析师Ashley Petersen表示。其指出,看起来“原油在年底前将保持良好走势”。此外,美元指数周五盘中从三个月高位回落,此前据彭博援引三位知情人士报道称 ,美国总统特朗普倾向于任命美联储理事鲍威尔担任央行的下一任主席。

分析师认为,鲍威尔的立场被认为是更为鸽派的,所以这对美元不利。

另外,美国油服公司贝克休斯(Baker Hughes)公布数据显示,本周美国活跃钻机增加1座至737座,但本月减少13座,为2016年5月来最大降幅。

数据显示,美国10月27日当周石油钻井总数增加1座至737座,结束连降三周的周期,预期为736座,前值为736座,去年同期为441座。本月石油钻井平台数量下降13座,创2016年5月以来最大月度降幅。也是2016年5月以来首次出现连续下降三个月的情况。

Source:

Source:

米末

米末

梦婕

梦婕