9334 Kesm 科技 rm3.54 进入的原因--

1)kesm 科技擁有強穩的資產負債表,截至2015年1月底公司现金有1.36亿,借款为8897万,淨現金達4700萬令吉,

每股净现金为rm1.09, nta=rm5.81 (现股价严重被低估了),roe=5.1

2)Kesm主攻个人电脑、平板电脑、智能手机和汽车这4大领域的晶片与测试业务。

在全球营收规模首十大半导体厂商当中,跟kesm有生意来往的,占了6个.(Intel, Samsung, Qualcomm, Micron,

Toshiba and Texas Instruments.)执行主席兼首席执行员林信赐表示,

该集团预料汽车晶片需求将加速。他说,自动驾驶汽车预料将在未来10年内冲击世界市场。

“因此,晶片需求预料将在未来数年大幅增长。

4)KESM科技的主要业务是电子零件生产,收购了KESM Test后,就可涉足汽车的电子零件业务。

随着汽车里的电子仪器越来越多,所需的电子零件也越来越多,且需要更高科技的测试设备。

其中一个就是司机驾驶辅助科技。目前这系统将被整合到一个晶片,所以,是半导体领域亮眼的增长前景,

而该公司已经有了相关的专业知识和领导地位。公司大部分净利来自kesm test,也难怪收购成功后,股价开始向上走势.

5)买股看公司的未来是否成长,净利多少等,当可见度变得清晰,投资风险相对变小,

股价也将呈现上升势头,kesm 会是不错的选择。

6)公司诚信度是很好的,因此数据造假应该不会发生在这公司上。

7)30大股东已持有78.68%(33845张),市场流通量只有9169张(21.32%),总股数为43014張.

大股东己持 53.49% .kesm现提供的投资机会,真的是越買越高,趁现在低,早点进货,等待丰衣足食.

8)kesm 绝对是投资者的首选股,公司的潜在价值好,成长佳,将会是一只黑马股。

9)估计2015全年eps=rm0.30 ,合理的pe=15 ,股价=rm4.50

10)kesm科技己完成收购kesm test股份,将增加40%的净利,相信2015年Q4,2016年可显现成長净利,因此现是进入良机.

目前rolling 4 quarters 的eps=rm0.29 ,如果2016年eps增加40%,到时eps为(rm0.29+rm0.11)

=rm0.40sen ,取pe=15倍,股价可达rm6.00

11)目前kesm的股价=rm3.53 ,用eps=rm0.30算,只是pe=11.7倍在交易,比较其他科技股后,明显被低估了.

12)有大股东sunright 作为强大的后盾,可保立足于市场且看好前景.(http://www.sunright.com/eng/index.htm)

只供参考,进出自负。

http://www.kesmi.com/

正确机率多才能成功

所以,总括一句,我们只是平民散户,通过本身对投资的喜好和研究,希望(努力)在股市中挣到不错的回酬,

什么大师专家,受之有愧,不必对号入座。

不论我们做什么决定,都会诚实的面对结果。投资组合不是考试,不能每次要求一百分。

这三年多来,我们确然做了一些低级错误,不过也做了更多的正确决定,所以我们才能获得如此不差的成绩。

现实生活里,错和对总是交叉发生,每次都做对,不叫“成功”,那是“完美”,是每个人追求的境界(却不大可能达到)。

成功的投资者,只需要把正确的投资机率更多发生就是了。

取自于--http://klse.i3investor.com/blogs/golden_years/55570.jsp

kesm 技术图美,无阻力,看到幸福的未来了.

a)KESM - TP may be revised upwards to RM4.55 post acquisition

[size=11.9999990463257px]

Background

KESM Industries Berhad is a semiconductor company primarily involved in the

provision of burn-in and test services. It is the largest independent burn-in

service company in Malaysia. The company serves as a sub-contractor to

electronic multi-national corporations. Operations are located across Malaysia

and China. As its largest shareholder, the group is an associate of the Sunright

group of companies.

Story So Far

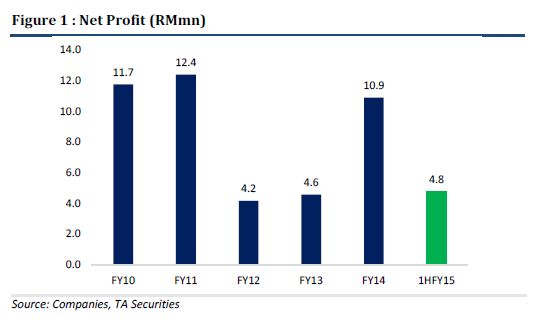

Enduring a tough spell, FY12 and FY13 were challenging years for the group. In

FY12, profit declined by 66.4% YoY to RM4.2mn. The reason for the slip was

attributed to a lower than anticipated production ramp up in China. This was

made worse by escalating labour costs in China. Also, an impairment of trade

receivables totalling RM7.0mn was recorded – as a customer in its electronic

manufacturing services (EMS) business ran into credit risk. Fortunes extended

into the following year amid weak industry demand and the implementation of

minimum wages locally.

Nevertheless, the weakness was short-lived as overall performance rebounded

in FY14. Mimicking the recovery of global semiconductor sales, the group

achieved internal records of over one billion semiconductor devices shipped.

Also, it enjoyed benefits from better productivity and positive cost control

measures. All in all, earnings recovered by 138.2% YoY to RM10.9mn. This was

in spite of higher electricity costs during the period.

Maintaining its momentum, the group recorded a net profit of RM4.8mn

(+70.5% YoY) in the 1HFY15.

Driver SeatCurrent strategies are guided by two key initiatives. The first of which is to ‘build long term

Driver SeatCurrent strategies are guided by two key initiatives. The first of which is to ‘build long term

growth in the auto market segment’. At approximately 70% of total revenue, the automotive

segment is by far the group’s largest contributor by end market segment. As a sub-contractor

to various electronic multi-national corporations, its products are predominantly found in

upper-tier auto manufacturers.

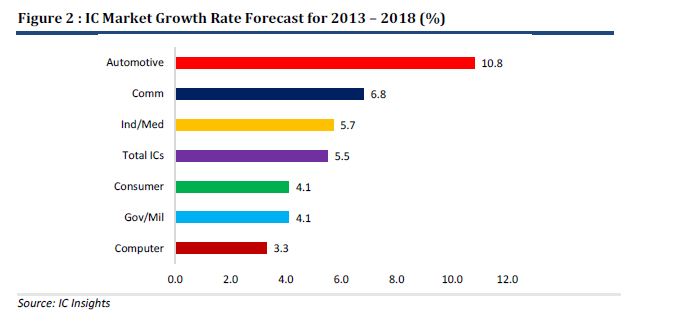

Analysing by end use applications, the automotive segment is forecasted to have the highest

future growth rate. IC Insights expects the segment to increase by a CAGR of 10.8% YoY

between 2013 and 2018. Partly attributed to its smaller base, this will be driven by an

increase in IC contents across new cars. Applications include vehicle-to-vehicle

communications, mandatory back up cameras and various driver assist systems. Certain

manufacturers have also exhibit prototypes of ‘driverless’ cars which provide a glimpse of

future capabilities.

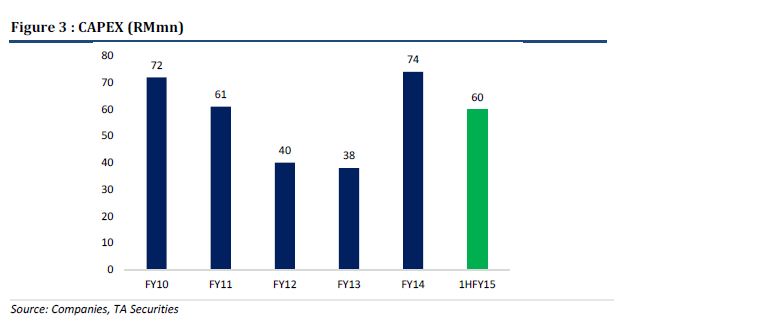

Test Growth EngineIts second initiative is to ‘strengthen its test growth engine’. Amid rapid technological

changes, testing services remain a fundamental part of the semiconductor manufacturing

process. Currently, the company has a capacity of 100 installed testers. Operating on a

controlled growth approach, plans are to add an additional 5 to 10 testers annually. On

average, test equipment cost between US$1.0-2.0mn each. In the 1HFY15, the group spent a

total of RM60mn on CAPEX – representing 81% of last financials year’s amount. We interpret

this as a positive signal of a brighter outlook ahead.

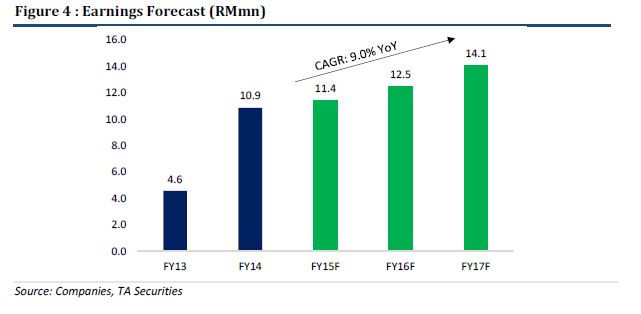

Resilient BusinessRelative to the industry’s cyclical nature, business operations have been stable and resilient.

Boasting a sturdy track record, all of its full year results have been profitable since listing in

1994. Moving forward, in line with plans to add an additional 5 to 10 testers annually, we

assume a capacity of 105/110/115 testers for FY15/FY16/FY17. This is accompanied by an

average utilisation rate of 80% (currently between 80-85%). Together, we estimate

FY15/FY16/FY17 earnings of RM11.4mn/RM12.5mn/RM14.1mn. This translates into a three

year CAGR of 9.0% between FY15 and FY17.

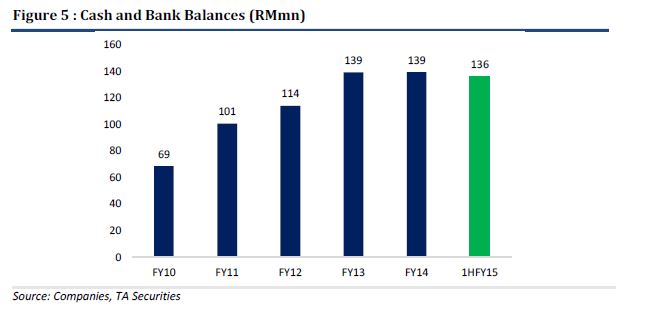

Cash RichFrom a balance sheet perspective, the company has a strong net cash position of RM47.4mn

or RM1.10/share (38.9% of share price). Given the capital intensive nature of the industry, it

maintains a high cash reserve to capture potential business. This ensures it is not beholden to

traditional sources of finance. Recently, it rewarded shareholders with a special dividend of

3.0sen/share. No dividend policy has been fixed.

Corporate RestructuringRecently, it announced the proposed acquisition of remainder shares in KESM Test from

Sunright Limited. This will be priced at a cash consideration of RM35.0mn for the 34.6% stake

– translating into a FY14 PE of 6.4x. The disposal is part of a corporate restructuring exercise

that allows KESM to gain full control of the test business. Meanwhile, Sunright will then focus

on equipment development. Ultimately, as KESM is an associate of Sunright, it will still benefit

from growth in the test business. The exercise is expected to be completed by the first half of

2015. Assuming the deal goes through, we estimate EPS could potentially rise by ca. 41.9%.

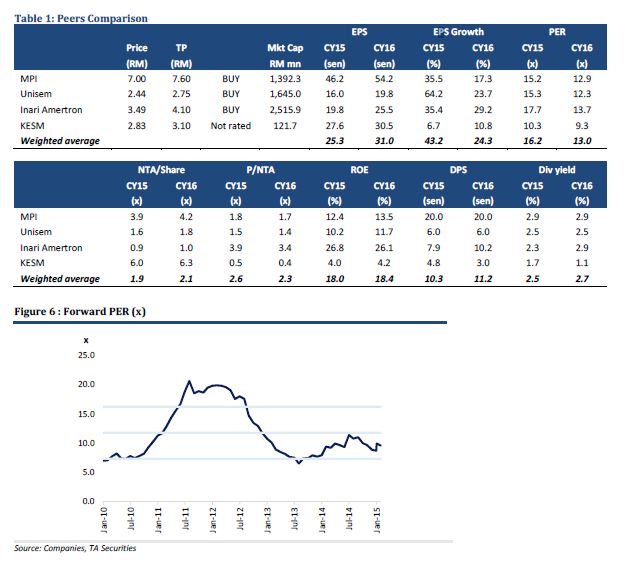

Attractive ValuationsWe value the company at a TP of RM3.05 – based on a PE of 10x and CY16 EPS of 30.5sen.

Although it can be argued that the company has a smaller market cap and lower earnings

growth, we opine that this is well accounted for by our discounted PE of 10x vs. our industry

target of 14x. Based on our estimates, the company is currently trading at a relatively

undemanding CY16 PE of 9.3x. Stripping out its net cash holdings, its effective CY16 PE

stands even lower at 5.7x. In the event the acquisition of KESM Test proceeds,

our TP may be revised upwards to RM4.55/share (potential upside of +60.8%). Not Rated.

Source: TA Securitiesb)KESM Industries – Cheap proxy to tech sector. Acquisition of minority interest to boost EPS by 50%

[size=11.9999990463257px]KESM Industries – Cheap proxy to the tech sector. Acquisition of minority interest to boost EPS by 50%

Disclaimer:- The purpose of this article is for sharing purpose only. It is neither a recommendation to buy or sell. Please do your own research before making any decision. At time of writing, I do own shares of this company.

Introduction

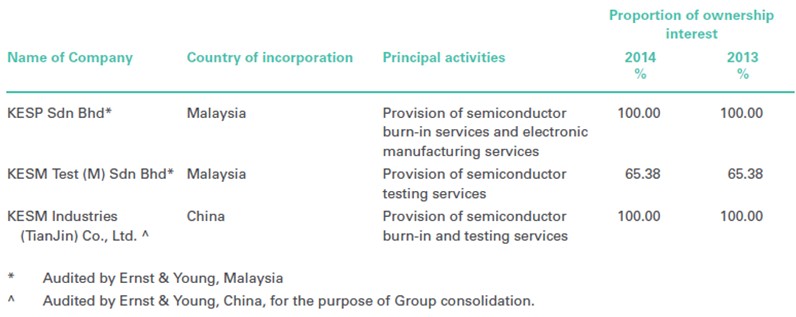

KESM has been engaged in specialized electronic manufacturing activities since 1978 is the largest independent burn-in service company in Malaysia. KESM's primary objective is in specialized electronic manufacturing activities and serves as sub-contractor to electronic multi-national corporations. In particular, it is in the business of providing burn-in services to the semiconductor industry. The company's customers are mainly from the global top ten semiconductor manufacturers in terms of market share including Intel, Samsung, Qualcomm, Micron, Toshiba and Texas Instruments. KESM has operations in Malaysia and China and a total of 3 subsidiaries as shown below:-

Historical earnings

I initially bought into KESM due to its strong balance sheet with huge cash hoard but am starting to see a growth story here. Let’s take a look at the historical figures for KESM

A quick look at KESM’s historical profitability underlines the cyclical nature of the business it is in. While revenue was growing steadily hitting at an all time high in 2014, operating and net profit margins are razor thin and the net profits gyrates wildly, falling from a high of RM 16.7mil in 2011 to only RM 7.3mil in 2012. Since then however, net profit has grown steadily and more than doubled to RM18.9 mil as of the latest trailing 12 months results. KESM’s free cashflow is rather lumpy with high capex requirements every now and then, but overall, they are still generate positive free cashflow. Their CFFO is rather high due to their high depreciation cost of almost RM 53 million in the last financial year. Its ROIC is also average, at only 7% and ROE is even lower at 4% due to its large cash hoard.

The operating margins although improving, are still low and suggest that KESM probably has no moat, but even a moat-less company can be a good investment if it is cheap enough. KESM’s balance sheet is strong. It has a net cash of RM1.25 per share (RM 54 mil) which makes up close to 44% of its market capitalization based on its last closing price of RM2.83. KESM’s enterprise valuation metrics suggest that it is not expensive

Net cash /share = RM 1.25

Excess cash/share = RM 3.27

EV/EBITDA = 1.4x

EV/EBIT = 6.1x

Despite its cheapness, market has probably not discovered KESM because from P/E standpoint, KESM appears more expensive at around 9.4x 2015ttm earnings. The divergence of the P/E and EV/EBIT is mainly caused by the high excess cash and minority interest carried in its balance sheet.

Acquisition of minority interest to boost EPS by more than 50%

In February 2015, KESM proposed to acquire the entire remaining minority interest stake of KESM Test (M) Sdn Bhd from the major shareholder for RM 35 million. The rationale provided by the CEO for this exercise was to streamline the operations of the subsidiaries by allowing the major shareholder (Sunright Limited) to focus on test and burn in equipment innovations (RnD) while KESMI group focuses on providing burn in and test services. The table below summarizes the EPS contributions of the minority stake and what shareholders of KESM would stand to gain.

Based on the acquisition cost of RM35 million and using the average minority interest net profit contribution over past 3 years, the effective P/E of the acquisition works out to 6.4 x which is a good deal. If we inverse the P/E ratio of the acquisition, the earnings yield is about 15.6%, which implies that this is a good use of its excess cash to enhance returns to shareholders. The subsidiary KESM (M) Test Sdn Bhd also appears to be the major driver of earnings for the group judging from the high percentage of the minority interest contribution to total earnings. This acquisition which was recently approved in the AGM, will also boost its EPS by more than 50%,

Price = RM2.83

EPS pre-acquisition = RM 0.3

EPS post acquisition = RM 0.44

P/E pre-acquisition = 9.4x

P/E post acquisition = 6.4x

Although the acquisition cost was RM35 mil, net net, the acquisition is expected to reduce the net cash holdings of KESM group overall by only RM10 million after taking into account the cash holdings of the subsidiary, dividend payments from the subsidiary and the expenses related to the proposed acquisition. The earnings contribution from the acquisition of the minority stake is expected to be reflected in the group’s FYE 2015 results.

Barring any unforeseen negative earnings surprises, I believe that the exercise above will crystallize the valuations of KESM in the coming quarters and re-rate the stock price as what similar exercise has done for companies like Latitude Tree. If we assume that P/E ratio of 9x is fair for KESM, then after the exercise, KESM share price is looking at least a 40% upside from current levels.

Target price based on P/E of 9x post acquisition = RM 3.96

Growth to be underlined by its focus in the automotive semiconductor segment

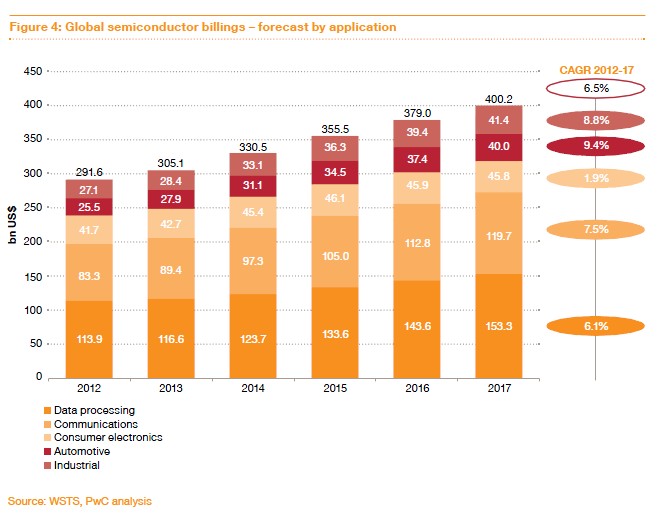

Aside from this exercise, it is also worth noting that KESM is expected to see better earnings growth moving forward with its focus in automotive semiconductor testing. Over the years, it has invested heavily in new equipment and machinery to support this direction. Automotive semiconductors are generally subjected to more stringent quality requirements due to safety reasons and potential costly product recalls. More cars are being equipped with increasingly more complex electronics and automotive semiconductor segment is expected to grow at a rate of 9.4% p.a based on a report by PWC semiconductor. Even the tech giant NXP semiconductors recently acquired Freescale Semiconductors for USD 11.8 billion with the objective of increasing its market share in automotive chips. KESM appears to be well positioned to take advantage of this new area of growth as its plants are currently at 70-80% utilization rate and space ready to take off any expansion in the future.

Valuation of KESM using DCF method (post acquisition of minority interest)

The 5 year average free cashflow was used as a starting point. As semiconductor up-cycles are short, I conservatively estimate a 5 year period of super-normal growth in FCF of 10% believing that its push towards automotive sector will start bearing fruits soon and conservatively a 3 % growth thereafter to adjust for inflation. As KESM has a healthy balance sheet and has generally been profitable over the years, I used a discount rate of 10%. I adjusted excess cash by RM10mil and zeroed out minority interest as the assumptions after the acquisition. Using these assumptions, I arrived at DCF derived intrinsic value of RM3.77 which presents a 25% margin of safety from current prices.

Summary

Strengths/Opportunities

- Strong balance sheet with net cash of RM1.25 / share limits downside

- Re-rating of stock price post acquisition of minority interest stake

- A cheap proxy to ride the automotive semiconductor boom due its large multi-national client base

Weakness/Threats

- Sharp increases in electricity and labour costs

- Capabilities limited to testing and burn in services only. May be less appealing to clients who prefer OEM able to provide an end to end solution (contract manufacturing + test services)

References

NOBY

17 APR 2015

2015-05-14 10:28

分析:达证券 http://www.nanyang.com/node/700520?tid=704

2201201421502890331757263402.jpg)

KESM Industries Bhd is riding high on the growth in demand for semiconductors from a global automobile industry which is becoming more technology-oriented.

For the first time in history, global automobile sales hit a record 82.84 million vehicles, according to a report from US-based consulting firm IHS Automotive. China alone is reported to have hit 17.9 million units for 2013, a 15.7% jump from 2012.

Carmakers have also benefited largely from an increase in demand for luxury cars in the US, one of the world’s biggest markets. The automobile industry has become more technology-oriented and reliant on semiconductors to carry out these technological advancements, which can mean only good news for companies like KESM, which specialises in testing integrated circuits (ICs) for semiconductor manufacturers.

“New growth is no longer in the smartphone or tablet segment, but in automobiles. We have several new clients in the business of making semiconductors for the automobile industry. We will leverage their presence and this will drive growth,” says executive director Kenneth Tan.

The number of cars sold is expected to grow but, more importantly, the overall content of semiconductors used in each car will also rise, as more devices are required for safety systems, infotainment and GPS.

For the full story, please subscribe to Focus Malaysia.

- See more at: http://www.focusmalaysia.my/Main ... thash.Gv0O0gll.dpuf

Lim says the content of electronics in a car is expected to grow to RM1.2b in 2019 from RM1b in 2014. (Pic by:Ismail Che Rus/TMR)

Lim says the content of electronics in a car is expected to grow to RM1.2b in 2019 from RM1b in 2014. (Pic by:Ismail Che Rus/TMR)

1)kesm 科技擁有強穩的資產負債表,截至2015年1月底公司现金有1.36亿,借款为8897万,淨現金達4700萬令吉,

每股净现金为rm1.09, nta=rm5.81 (现股价严重被低估了),roe=5.1

2)Kesm主攻个人电脑、平板电脑、智能手机和汽车这4大领域的晶片与测试业务。

在全球营收规模首十大半导体厂商当中,跟kesm有生意来往的,占了6个.(Intel, Samsung, Qualcomm, Micron,

Toshiba and Texas Instruments.)执行主席兼首席执行员林信赐表示,

该集团预料汽车晶片需求将加速。他说,自动驾驶汽车预料将在未来10年内冲击世界市场。

“因此,晶片需求预料将在未来数年大幅增长。

4)KESM科技的主要业务是电子零件生产,收购了KESM Test后,就可涉足汽车的电子零件业务。

随着汽车里的电子仪器越来越多,所需的电子零件也越来越多,且需要更高科技的测试设备。

其中一个就是司机驾驶辅助科技。目前这系统将被整合到一个晶片,所以,是半导体领域亮眼的增长前景,

而该公司已经有了相关的专业知识和领导地位。公司大部分净利来自kesm test,也难怪收购成功后,股价开始向上走势.

5)买股看公司的未来是否成长,净利多少等,当可见度变得清晰,投资风险相对变小,

股价也将呈现上升势头,kesm 会是不错的选择。

6)公司诚信度是很好的,因此数据造假应该不会发生在这公司上。

7)30大股东已持有78.68%(33845张),市场流通量只有9169张(21.32%),总股数为43014張.

大股东己持 53.49% .kesm现提供的投资机会,真的是越買越高,趁现在低,早点进货,等待丰衣足食.

8)kesm 绝对是投资者的首选股,公司的潜在价值好,成长佳,将会是一只黑马股。

9)估计2015全年eps=rm0.30 ,合理的pe=15 ,股价=rm4.50

10)kesm科技己完成收购kesm test股份,将增加40%的净利,相信2015年Q4,2016年可显现成長净利,因此现是进入良机.

目前rolling 4 quarters 的eps=rm0.29 ,如果2016年eps增加40%,到时eps为(rm0.29+rm0.11)

=rm0.40sen ,取pe=15倍,股价可达rm6.00

11)目前kesm的股价=rm3.53 ,用eps=rm0.30算,只是pe=11.7倍在交易,比较其他科技股后,明显被低估了.

12)有大股东sunright 作为强大的后盾,可保立足于市场且看好前景.(http://www.sunright.com/eng/index.htm)

只供参考,进出自负。

http://www.kesmi.com/

正确机率多才能成功

所以,总括一句,我们只是平民散户,通过本身对投资的喜好和研究,希望(努力)在股市中挣到不错的回酬,

什么大师专家,受之有愧,不必对号入座。

不论我们做什么决定,都会诚实的面对结果。投资组合不是考试,不能每次要求一百分。

这三年多来,我们确然做了一些低级错误,不过也做了更多的正确决定,所以我们才能获得如此不差的成绩。

现实生活里,错和对总是交叉发生,每次都做对,不叫“成功”,那是“完美”,是每个人追求的境界(却不大可能达到)。

成功的投资者,只需要把正确的投资机率更多发生就是了。

取自于--http://klse.i3investor.com/blogs/golden_years/55570.jsp

kesm 技术图美,无阻力,看到幸福的未来了.

a)KESM - TP may be revised upwards to RM4.55 post acquisition

[size=11.9999990463257px]Author: tasecurities | Publish date: Wed, 22 Apr 2015, 04:24 PM

[size=11.9999990463257px]

Background

KESM Industries Berhad is a semiconductor company primarily involved in the

provision of burn-in and test services. It is the largest independent burn-in

service company in Malaysia. The company serves as a sub-contractor to

electronic multi-national corporations. Operations are located across Malaysia

and China. As its largest shareholder, the group is an associate of the Sunright

group of companies.

Story So Far

Enduring a tough spell, FY12 and FY13 were challenging years for the group. In

FY12, profit declined by 66.4% YoY to RM4.2mn. The reason for the slip was

attributed to a lower than anticipated production ramp up in China. This was

made worse by escalating labour costs in China. Also, an impairment of trade

receivables totalling RM7.0mn was recorded – as a customer in its electronic

manufacturing services (EMS) business ran into credit risk. Fortunes extended

into the following year amid weak industry demand and the implementation of

minimum wages locally.

Nevertheless, the weakness was short-lived as overall performance rebounded

in FY14. Mimicking the recovery of global semiconductor sales, the group

achieved internal records of over one billion semiconductor devices shipped.

Also, it enjoyed benefits from better productivity and positive cost control

measures. All in all, earnings recovered by 138.2% YoY to RM10.9mn. This was

in spite of higher electricity costs during the period.

Maintaining its momentum, the group recorded a net profit of RM4.8mn

(+70.5% YoY) in the 1HFY15.

growth in the auto market segment’. At approximately 70% of total revenue, the automotive

segment is by far the group’s largest contributor by end market segment. As a sub-contractor

to various electronic multi-national corporations, its products are predominantly found in

upper-tier auto manufacturers.

Analysing by end use applications, the automotive segment is forecasted to have the highest

future growth rate. IC Insights expects the segment to increase by a CAGR of 10.8% YoY

between 2013 and 2018. Partly attributed to its smaller base, this will be driven by an

increase in IC contents across new cars. Applications include vehicle-to-vehicle

communications, mandatory back up cameras and various driver assist systems. Certain

manufacturers have also exhibit prototypes of ‘driverless’ cars which provide a glimpse of

future capabilities.

Test Growth EngineIts second initiative is to ‘strengthen its test growth engine’. Amid rapid technological

changes, testing services remain a fundamental part of the semiconductor manufacturing

process. Currently, the company has a capacity of 100 installed testers. Operating on a

controlled growth approach, plans are to add an additional 5 to 10 testers annually. On

average, test equipment cost between US$1.0-2.0mn each. In the 1HFY15, the group spent a

total of RM60mn on CAPEX – representing 81% of last financials year’s amount. We interpret

this as a positive signal of a brighter outlook ahead.

Resilient BusinessRelative to the industry’s cyclical nature, business operations have been stable and resilient.

Boasting a sturdy track record, all of its full year results have been profitable since listing in

1994. Moving forward, in line with plans to add an additional 5 to 10 testers annually, we

assume a capacity of 105/110/115 testers for FY15/FY16/FY17. This is accompanied by an

average utilisation rate of 80% (currently between 80-85%). Together, we estimate

FY15/FY16/FY17 earnings of RM11.4mn/RM12.5mn/RM14.1mn. This translates into a three

year CAGR of 9.0% between FY15 and FY17.

Cash RichFrom a balance sheet perspective, the company has a strong net cash position of RM47.4mn

or RM1.10/share (38.9% of share price). Given the capital intensive nature of the industry, it

maintains a high cash reserve to capture potential business. This ensures it is not beholden to

traditional sources of finance. Recently, it rewarded shareholders with a special dividend of

3.0sen/share. No dividend policy has been fixed.

Corporate RestructuringRecently, it announced the proposed acquisition of remainder shares in KESM Test from

Sunright Limited. This will be priced at a cash consideration of RM35.0mn for the 34.6% stake

– translating into a FY14 PE of 6.4x. The disposal is part of a corporate restructuring exercise

that allows KESM to gain full control of the test business. Meanwhile, Sunright will then focus

on equipment development. Ultimately, as KESM is an associate of Sunright, it will still benefit

from growth in the test business. The exercise is expected to be completed by the first half of

2015. Assuming the deal goes through, we estimate EPS could potentially rise by ca. 41.9%.

Attractive ValuationsWe value the company at a TP of RM3.05 – based on a PE of 10x and CY16 EPS of 30.5sen.

Although it can be argued that the company has a smaller market cap and lower earnings

growth, we opine that this is well accounted for by our discounted PE of 10x vs. our industry

target of 14x. Based on our estimates, the company is currently trading at a relatively

undemanding CY16 PE of 9.3x. Stripping out its net cash holdings, its effective CY16 PE

stands even lower at 5.7x. In the event the acquisition of KESM Test proceeds,

our TP may be revised upwards to RM4.55/share (potential upside of +60.8%). Not Rated.

Source: TA Securitiesb)KESM Industries – Cheap proxy to tech sector. Acquisition of minority interest to boost EPS by 50%

[size=11.9999990463257px]Author: NOBY | Publish date: Mon, 20 Apr 2015, 11:44 PM

[size=11.9999990463257px]KESM Industries – Cheap proxy to the tech sector. Acquisition of minority interest to boost EPS by 50%

Disclaimer:- The purpose of this article is for sharing purpose only. It is neither a recommendation to buy or sell. Please do your own research before making any decision. At time of writing, I do own shares of this company.

Introduction

KESM has been engaged in specialized electronic manufacturing activities since 1978 is the largest independent burn-in service company in Malaysia. KESM's primary objective is in specialized electronic manufacturing activities and serves as sub-contractor to electronic multi-national corporations. In particular, it is in the business of providing burn-in services to the semiconductor industry. The company's customers are mainly from the global top ten semiconductor manufacturers in terms of market share including Intel, Samsung, Qualcomm, Micron, Toshiba and Texas Instruments. KESM has operations in Malaysia and China and a total of 3 subsidiaries as shown below:-

Historical earnings

I initially bought into KESM due to its strong balance sheet with huge cash hoard but am starting to see a growth story here. Let’s take a look at the historical figures for KESM

A quick look at KESM’s historical profitability underlines the cyclical nature of the business it is in. While revenue was growing steadily hitting at an all time high in 2014, operating and net profit margins are razor thin and the net profits gyrates wildly, falling from a high of RM 16.7mil in 2011 to only RM 7.3mil in 2012. Since then however, net profit has grown steadily and more than doubled to RM18.9 mil as of the latest trailing 12 months results. KESM’s free cashflow is rather lumpy with high capex requirements every now and then, but overall, they are still generate positive free cashflow. Their CFFO is rather high due to their high depreciation cost of almost RM 53 million in the last financial year. Its ROIC is also average, at only 7% and ROE is even lower at 4% due to its large cash hoard.

The operating margins although improving, are still low and suggest that KESM probably has no moat, but even a moat-less company can be a good investment if it is cheap enough. KESM’s balance sheet is strong. It has a net cash of RM1.25 per share (RM 54 mil) which makes up close to 44% of its market capitalization based on its last closing price of RM2.83. KESM’s enterprise valuation metrics suggest that it is not expensive

Net cash /share = RM 1.25

Excess cash/share = RM 3.27

EV/EBITDA = 1.4x

EV/EBIT = 6.1x

Despite its cheapness, market has probably not discovered KESM because from P/E standpoint, KESM appears more expensive at around 9.4x 2015ttm earnings. The divergence of the P/E and EV/EBIT is mainly caused by the high excess cash and minority interest carried in its balance sheet.

Acquisition of minority interest to boost EPS by more than 50%

In February 2015, KESM proposed to acquire the entire remaining minority interest stake of KESM Test (M) Sdn Bhd from the major shareholder for RM 35 million. The rationale provided by the CEO for this exercise was to streamline the operations of the subsidiaries by allowing the major shareholder (Sunright Limited) to focus on test and burn in equipment innovations (RnD) while KESMI group focuses on providing burn in and test services. The table below summarizes the EPS contributions of the minority stake and what shareholders of KESM would stand to gain.

Based on the acquisition cost of RM35 million and using the average minority interest net profit contribution over past 3 years, the effective P/E of the acquisition works out to 6.4 x which is a good deal. If we inverse the P/E ratio of the acquisition, the earnings yield is about 15.6%, which implies that this is a good use of its excess cash to enhance returns to shareholders. The subsidiary KESM (M) Test Sdn Bhd also appears to be the major driver of earnings for the group judging from the high percentage of the minority interest contribution to total earnings. This acquisition which was recently approved in the AGM, will also boost its EPS by more than 50%,

Price = RM2.83

EPS pre-acquisition = RM 0.3

EPS post acquisition = RM 0.44

P/E pre-acquisition = 9.4x

P/E post acquisition = 6.4x

Although the acquisition cost was RM35 mil, net net, the acquisition is expected to reduce the net cash holdings of KESM group overall by only RM10 million after taking into account the cash holdings of the subsidiary, dividend payments from the subsidiary and the expenses related to the proposed acquisition. The earnings contribution from the acquisition of the minority stake is expected to be reflected in the group’s FYE 2015 results.

Barring any unforeseen negative earnings surprises, I believe that the exercise above will crystallize the valuations of KESM in the coming quarters and re-rate the stock price as what similar exercise has done for companies like Latitude Tree. If we assume that P/E ratio of 9x is fair for KESM, then after the exercise, KESM share price is looking at least a 40% upside from current levels.

Target price based on P/E of 9x post acquisition = RM 3.96

Growth to be underlined by its focus in the automotive semiconductor segment

Aside from this exercise, it is also worth noting that KESM is expected to see better earnings growth moving forward with its focus in automotive semiconductor testing. Over the years, it has invested heavily in new equipment and machinery to support this direction. Automotive semiconductors are generally subjected to more stringent quality requirements due to safety reasons and potential costly product recalls. More cars are being equipped with increasingly more complex electronics and automotive semiconductor segment is expected to grow at a rate of 9.4% p.a based on a report by PWC semiconductor. Even the tech giant NXP semiconductors recently acquired Freescale Semiconductors for USD 11.8 billion with the objective of increasing its market share in automotive chips. KESM appears to be well positioned to take advantage of this new area of growth as its plants are currently at 70-80% utilization rate and space ready to take off any expansion in the future.

Valuation of KESM using DCF method (post acquisition of minority interest)

The 5 year average free cashflow was used as a starting point. As semiconductor up-cycles are short, I conservatively estimate a 5 year period of super-normal growth in FCF of 10% believing that its push towards automotive sector will start bearing fruits soon and conservatively a 3 % growth thereafter to adjust for inflation. As KESM has a healthy balance sheet and has generally been profitable over the years, I used a discount rate of 10%. I adjusted excess cash by RM10mil and zeroed out minority interest as the assumptions after the acquisition. Using these assumptions, I arrived at DCF derived intrinsic value of RM3.77 which presents a 25% margin of safety from current prices.

Summary

Strengths/Opportunities

- Strong balance sheet with net cash of RM1.25 / share limits downside

- Re-rating of stock price post acquisition of minority interest stake

- A cheap proxy to ride the automotive semiconductor boom due its large multi-national client base

Weakness/Threats

- Sharp increases in electricity and labour costs

- Capabilities limited to testing and burn in services only. May be less appealing to clients who prefer OEM able to provide an end to end solution (contract manufacturing + test services)

References

NOBY

17 APR 2015

c)KESM加大投資汽車領域2015-05-02 15:42

(吉隆坡2日訊)軟體和電子方案供應股近期引領大盤走揚,同時也重燃投資者對半導體領域的興趣。

分析員認為,半導體晶片市場正迎來週期性上升趨勢,主要從事半導體測試和預燒服務的KESM科技(KESM,9334,主板科技組)前景也顯著改善。

特大通過全購KESM Test34.62%

值得一提的是,KESM科技股東在4月16日召開的股東特大批准以3千500萬令吉,收購其餘未持有的KESM Test股權34.62%股權,後者現為其最重要的盈利來源,幾乎佔集團過去3個財政年的全部淨利。

該公司首席執行員林信賜在股東特大後表示,隨著半導體在汽車應用的使用率增加,現是收購KESM Test股權的最佳時機。

他說,汽車電子組件科技日趨新穎,需要新的測試設備,而KESM Test在汽車領域測試經驗豐富,更是領域領頭羊。

歸功於測試能力不斷提昇,以及製造循環時間也有所下降,KESM Test的2013和2014財政年營業額走揚至5千800萬令吉和6千850萬令吉,相等於年均17%增幅。

分析員認為,基於KESM Test專注汽車產品,因此並沒有直接對等連接(DirectPeer)問題,可善用業務規模龐大,以及先行者優勢來攫取攀升的需求。

達證券報告早前指出,若相關交易案過關,可能提昇KESM科技每股盈利年增41.9%。

隨著收購案闖關成功,KESM科技股價也水漲船高。在4月16日至24日期間,該股股價從2令吉70仙飆升13%至3令吉零5仙,但後因套利回吐,收在2令吉82仙。(星洲日報/財經‧The Edge專

版)

KESM科技 收购后估值仍低2015-05-14 10:28

目标价:4.55令吉

最新进展:

上周五,KESM科技(KESM,9334,主板科技股)宣布,股东批准收购KESM测试公司(KESM Test)剩余股权,因而成为无条件股权买卖协议。

买卖双方已同意,把交易完成日期定在今日。

行家建议:

在考量到该项收购计划带来的效益,我们把KESM科技的2015、2016、2017财年净利预测,分别上调12.1%、49.6%和50%,达1280万、1860万和2110万令吉。

KESM科技以3500万令吉,向Sunright有限公司收购KESM测试公司剩余股权,是集团其中一项重组活动,符合推动测试业务成长的策略。

由于Sunright是集团大股东,所以将从未来成长中受惠。

同时,也让Sunright持续关注在设备发展的资源上。

除了上调净利预测外,我们也把KESM科技的目标价格,从3.05令吉,调高至4.55令吉。

此外,该股估值仍具吸引力。

在加入收购计划带来的影响后,该股目前以6.7倍的2016年本益比交易,属于偏低水平。

分析:达证券 http://www.nanyang.com/node/700520?tid=704

d)Automotive sector to drive KESM’s sales

KESM Industries Bhd is riding high on the growth in demand for semiconductors from a global automobile industry which is becoming more technology-oriented.

For the first time in history, global automobile sales hit a record 82.84 million vehicles, according to a report from US-based consulting firm IHS Automotive. China alone is reported to have hit 17.9 million units for 2013, a 15.7% jump from 2012.

Carmakers have also benefited largely from an increase in demand for luxury cars in the US, one of the world’s biggest markets. The automobile industry has become more technology-oriented and reliant on semiconductors to carry out these technological advancements, which can mean only good news for companies like KESM, which specialises in testing integrated circuits (ICs) for semiconductor manufacturers.

“New growth is no longer in the smartphone or tablet segment, but in automobiles. We have several new clients in the business of making semiconductors for the automobile industry. We will leverage their presence and this will drive growth,” says executive director Kenneth Tan.

The number of cars sold is expected to grow but, more importantly, the overall content of semiconductors used in each car will also rise, as more devices are required for safety systems, infotainment and GPS.

For the full story, please subscribe to Focus Malaysia.

- See more at: http://www.focusmalaysia.my/Main ... thash.Gv0O0gll.dpuf

e)KESM Sets Sight On Car Electronic In The Future

[size=1.5em]Farah AdillaFriday, January 16, 2015[size=0.85em]Lim says the content of electronics in a car is expected to grow to RM1.2b in 2019 from RM1b in 2014. (Pic by:Ismail Che Rus/TMR)

KESM Industries Bhd plans to accelerate its business focus in the automotive segment as its see tremendous growth potential in this segment.

Its executive chairman and CEO Samuel Lim Syn Soo said as the automotive industry is producing more self driven cars in the future, more electronics are being used as part of the component of a car and this augurs well with KESM business.

“With this growth, microprocessors and sensors manufacturers will increase its volume expense. The products will become cheaper but as features increase, the electronics become more complex and it must work reliably. That is where we come in.

“We are confident that this market will continue to grow. It will not be less, for sure. And KESM will have to be ready to make more investment in the burn-in and test market,” he told reporters after KESM's AGM and EGM in Kuala Lumpur yesterday.

KESM has been engaged in specialised electronic manufacturing activities since 1978. KESM's primary objective is in specialized electronic manufacturing activities and serves as sub-contractor to electronic multi-national corporations. In particular, it is in the business of providing burn-in services to the semiconductor industry.

Besides automotive industry, KESM also conduct burn-in and testing of semiconductors for industrial, medical, PC, information and communication industries.

He said the content of electronics in a car is expected to grow to US$330 in 2019 from US$284 in 2014.

The company's customers are mainly from the global top ten semiconductor manufacturers in terms of market share including Intel, Samsung, Qualcomm, Micron, Toshiba and Texas Instruments.

Lim said the company's test and burn-in lines in Kuala Lumpur, Penang and Tianjin, China are currently running at 70% to 80% capacity. Last year, the company delivered a record shipment of over a billion semiconductor devices generating record revenue of RM254.37 million.

Asked if the company has plans to expand its burn-in and testing lines, Lim said the company's existing plants each are space ready to take off any expansion in the future.

Last year, the company experienced a sharp rise in costs for labour and electricity, in both China and Malaysia.

“At the same time, we make good improvements in manufacturing cycle time and improved equipment utilisation. These efforts have enabled us to mitigate the cost increases,” Lim said.

For the financial year ended July 31, 2014 (FY14) jumped to RM10.88 million from the RM4.57 million recorded in FY13. Its revenue during the same period increased 2.7% to RM254.37 million from RM247.61 million.

f) | 只看该作者| kesm 会受惠吗? |

| |

没有评论:

发表评论