This post is a continuation of previous "Shell Trilogy: The Great Sale" article which is accessible from here.

3) North Sabah EOR (Announced Oct 2016, closed ??) Unlike Anasuria which is a concession, North Sabah EOR is under Production Sharing Scheme (PSC), details of which you can read more here. PSC is essentially a type of profit sharing arrangement where the profit is shared between the government and the operator after deducting out the cost. But the government will always has bills to pay even if the PSC is not making a profit. Hence, PSC is structured in such a way that caps the maximum cost that can be recouped in a reporting period (The technical term is Cost Recovery Ceiling, but there is no impact to accounting profit as any unrecoverd cost can be bought forward). The implication is the operator has to invest more of his own money to keep the operation ongoing especially during the low oil price period where costs have exceed the ceiling. Combined with Shell's reluctance to invest further on marginal assets, these provided the backdrop on the motivation for Shell to dispose its North Sabah assets.

At US$25m, is Hibiscus getting a good deal? Let's first compare the factsheets between North Sabah and Anasuria (a superb deal by all counts). Tabulation below shows key assets parameters of Anasuria and North Sabah:

Anasuria

North Sabah

Comment

Purchase Price (PP)

US$52.5m1

US$25.0m2

1) Economic interest since 1/1/2015 (~15 mths to close 10/3/2016) 2) Economic interest since 1/1/2017 (9 mths & counting to closing date)

2P Reserves (Acquisition Date)

20.2 MMbbl Oil 2.3 MMbbloe Gas

31.0 MMbbl Oil

Data is from Bursa Malaysia announcements

2C Reserves

5.6 MMbbl

39.5 MMbbl

Anasuria figure from FY16 AR

OPEX in bpd

US$29.873/15.11

US$13.924

3) Based on actual 2014 spending. Simple average 4 quarters OPEX has since dropped to US$15.11 4) Based on exchange rate USDMYR: 3.9592:1 @June 2016

Daily runrate in bpd

3.5k

9k

Purchase Price (PP) per 2P bbl

US$2.33

US$3.235

5) See below

PP per 2P+2C bbl

US$1.87

US$1.425

5) See below

Table below shows the differences between concession (Anasuria) and PSC (North Sabah).

Not all barrels are equal. To have an apple to apple comparison, we must first normalize a concession barrel with a PSC barrel. As can be seen in the first table, Anasuria Opex per barrel has nearly halved to US$15.11 since 2014. This is comparable with 2016 Opex of US$13.94 stated for North Sabah. We could therefore fairly deduced that the cost structure is quite similar for both the Anasuria & North Sabah. For modelling purpose, assuming oil price at US$55, Opex cost US$15 and a similar Capex cost US$15, total cost is US$30/US$55 or 45%

Anasuria(Concession)

Revenue (A)

US$55

Cost (B)

US$30

PBT

C=A-B

US$25

Tax (D)

40% Tax Rate

US$10

Net Profit

E=C-D

US$15

North Sabah (PSC)*

Revenue (A)

US$55

Cost (B)

US$30

Royalty (R)

US$5.50

PBT

C=A-B-R

US$19.50

His's Share of PBT

H=30% of C

US$5.85

Tax (D)

38% Tax Rate

US$2.22

Net Profit

E=H-D

US$3.63

Based on the model above, each barrel oil produced in Anasuria is US$15/US$3.6 = ~4x more profitable than a barrel produced in North Sabah. The other way of putting it is to say it takes 4 barrel oil oil produced in North Sabah to earn similar profit to a barrel of oil produced in Anasuria. So, using a normalizing factor N=4 to the Purchase Price per barrel oil in North Sabah,

North Sabah Purchase Price per 2P bbl= US$25m/31mbbls x 4= US$ 3.23

North Sabah Purchase Price per 2P+2C bbl=US$25m/70.5mbbls x 4= US$1.42

All in all for North Sabah, the Purchase Price per 2P bbl was at 40% premium compare with Anasuria. Inclusive of 2C resources, North Sabah's Purchase Price per 2P+2C barrel is at 25% discount. Overall, it can be reasonably concluded that the valuation for North Sabah is equally attractive compare with the Anasuria deal but at a smaller scale. And that is even without factoring that Anasuria's purchase price was based on Opex level of US$29.87 per bbl when the deal was struck.

Final Words The past few years were anything but an easy ride for Hibiscus. The management shift from exploration-oriented Jackpot to production-focused slow-but-steady growth has given much comfort. Those nightmares of flushing RM 100m+ down the exploration well only to encounter dry hole are truly over. If the Anasuria deal was the deal that save Hibiscus from bankruptcy, will the North Sabah deal propel Hibiscus to new height? The low asset entry price does not guarantee profitability but certainly provide much needed safety buffer against lower oil price. Today the focus shall be on the production costs, facilities uptime and maximizing reserve recovery, something certainly Hibiscus has better control with. As for the status of the deal, Hibiscus announced on 29/05/2017 that Petronas Carigali has waived its pre-emption rights under a joint operating agreement. Petronas has also conditionally approved the assignment of the Shell's interest to Hibiscus, which means the deal has not closed yet and can only be closed upon fulfilment of all conditions set by Petronas. Do take note that original closure date of the end of Q22017 was already due.

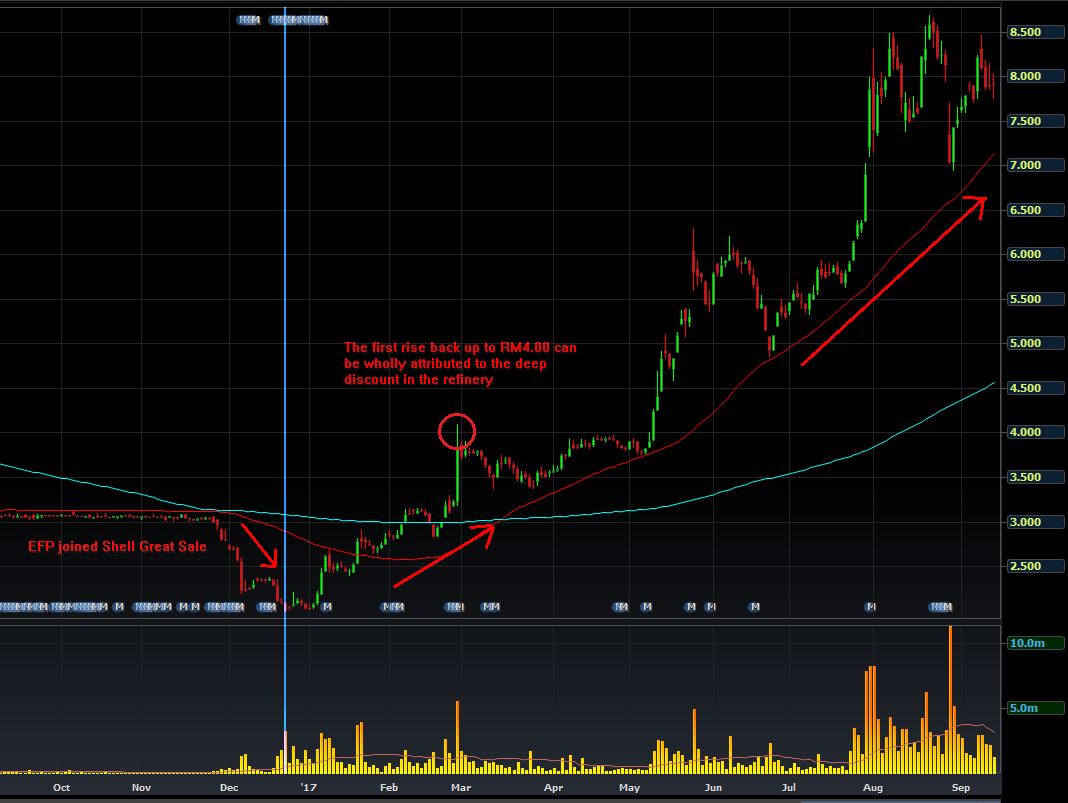

As for the share price, monster upward move of 39.7% on 20/09/2017 has exceeded the author's expectation by a wide margin. Without the benefit of hindsight, the author initially expects the RM0.56 level to be broken only upon the closure of the deal. The author believes that whatever windfall benefit from North Sabah deal should already be partially reflected in the price. With Brent oil price currently hovering at near the year high, caution is strongly advised. The author is humble and has been humbled by market numerous times to learn that investing is less about being correct than to simply make a profit out of our investment. The adage of "let the profit runs and cut the losses" can never be more apt here. Immediate support level is at RM0.61 and a much stronger level at RM0.56. Price dropping below RM0.56 flashes a big bearish signal.

Disclaimer:

1) The author has no access to management of Petronas, Shell or Hibiscus. The report was written purely based on the news reports, company statements and media releases together with industrial trade reports. Verificacy of the report is based on best efforts and was subject to the author's knowledge inadequacies, assumptions used and the probabilistic nature of the future events.

2) The author has position in Hibiscus and while trying to stay as objectively as possible but may still be influenced by subconscious confirmation and memory bias.

April 2015 marks a new chapter in the long, illustrious history of Shell when it announcedit was acquiring British Gas for £47bn. Simultaneously, Shell declared the combined business would sell off £17bn in assets, which would be returned to shareholder through share buyback. It certainly seemed a smart strategy considering oil price had plunged from $100+ per bbl to around $60 per bbl by the time the announcement was made. What could not be foreseen however was that oil price would further plunge to below $30 per bbl in Jan 2016, barely 8 months later. In response, Shell vowed to cut investment in order to protect its dividend.

All projects were scrutinized for their cash flow viabilities. Decisions were made where non-critical investments were postponed while those not able to self-sustained were earmarked to be disposed. Guided by the management decision, accelerated by the plunging oil price, the great sale especially those assets on the fringe (to Shell at least) began. When the big boys dine, we feed on their crumbs and frankly, the taste is not too bad!! And hence, the trilogy of deals relevant within the universe of Bursa Malaysia.

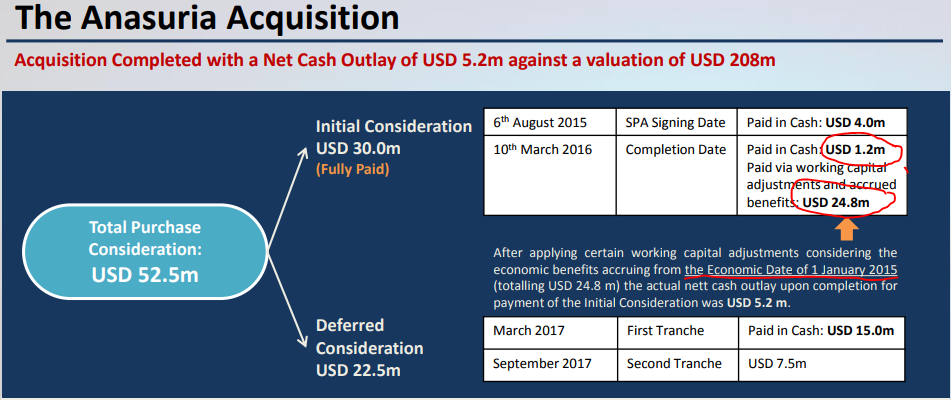

1) Anasuria Cluster (Deal announced Aug 2015, closed March 2016)

Hibiscus's quarterly reports revealed Opex cost around US$15 per barrels. But just two years earlier in 2014, the average cost per barrel in North Sea was around US$30. With oil price dropping to around US$30, this made Anasuria a no-brainer sale. How cheap then is the selling price? Hibiscus paid US$52.5 million for 50% stake in Anasuria. RCP Energy (a third party analyst) valued the asset (Hibiscus's portion) at US$113m in Sept 2015 report and US$208m in subsequent June 2016 report. Even then, the economic benefits were backdated to 1st Jan 2015. As shown below after adjusting for the "working capital adjustments and accrued benefits" of US$24.8m, the net purchase price was US$52m -US$24.8m = US$27.2m ONLY for an asset valued at US$208m!! Similarly, Hibiscus reported FY2016 negative goodwill gain on acquisition of RM364.1m.

Hibiscus's one year chart post completion told an interesting story of both a cautionary note and an opportunity. A cautionary note in the sense that a deal shall never be evaluated in isolation but must be within the context of operating environment. At the time of the deal completion, Hibiscus was trapped in a vicious vortex due to plunging oil prices, so vicious that eventually resulted in zeroing out all its investment in its 2 major operating subsidiaries Lime Plc and Hirex, a loss totaling some RM280.4m which would have outstripped its market capitalization at the time. The windfall of RM364.1m from Anasuria acquisition had more than cushioned all the impairment losses. More crucially, Anasuria gives Hibiscus a business unit that is generating positive cash flow quarter after quarter. Without a hint of exaggeration, Anasuria was the deal that saved Hibiscus from a near certain bankruptcy. The Aug 2016 announcement of 4QFY2016 results gave the clearest indication that the worst was over and hence lay the opportunity. Famed investor, Benjamin Graham once remarked that "In the short run, the market is a beauty contest but in the longer run is a weighing machine". The market will wake up, as it eventually did, to the potential of new Hibiscus, no doubt given the jolt by the announcement of the North Sabah deal.

2) Hengyuan (previously known as Shell Refinery Company (SRC)) (Deal announced Feb 2016, closed Dec 2016)

Not too dissimilar to Anasuria, the sale of 51% stake in SRC for a meagre sum of RM 1.80 per share (or US$66m) was driven by the desire to avoid capital investment more than anything else. So firm was its decision not to invest further in SRC than it chose to impair the refinery asset by RM461m in 4QFY2015, officially declaring to the world it would not upgrade the refinery. At worst, Shell was prepared to go as far as converting the refinery to an oil terminal, essentially writing off the whole asset. To Shell, US$66m sale is a welcome upside from a complete write off!! This is akin to your neighbor selling his house way below the market value because he is migrating oversea and not coming back. Would you similarly sell your house at that price? Well, unless one of your neighbor is a certain EPF…

A perfectly fine refinery with a name plate capacity of 156kbpd and is upgradable to meet Euro 4M and 5 standard at a relatively modest sum of US$160m which we found out later. How big is the discount then? A brand new 260kbpd, recently commissioned in Yunnan, China was built at the cost of US$4.4b, or roughly US$1.6b per 100kbpd capacity. At RM1.80 per share, total Enterprise Value (EV = Market cap + Debt - Cash) based on 4QFY2015 data was around RM1.85b or just US$282m per 100kbpd name plate capacity (USD:MYR 4.2:1), a mere 18% of the sticker price of a brand new refinery. Adding up 150% of the reported US$160m upgrade cost will increase EV per 100kbpd to US$436m, just some 27% of a brand new refinery. The math get more interesting if you consider than for every RM1 increment in Hengyuan's price is equal to 2.9% of a brand new refinery. What does that mean? Well, if you value the refinery at 33% of a brand new refinery that is more than 100% gain from Shell selling price of RM1.80. At 40%, that's more than triple the Shell selling price.

3) North Sabah EOR (Announced Oct 2016, closed ??)

To be continued...

Disclaimer:

1) The author has no access to management of Shell, Hengyuan and Hibiscus. The report was written purely based on the news reports, company statements and media releases together with industrial trade reports. Verificacy of the report is based on best efforts and was subject to the author's knowledge inadequacies, assumptions used and the probabilistic nature of the future events.

2) The author has positions in both Hibiscus and Hengyuan and while trying to stay as objectively as possible but may still be influenced by subconscious confirmation and memory bias.

D)

Public IB Research starts coverage on Hibiscus, target price RM1.06

KUALA LUMPUR (Sept 20): Public Investment Bank Bhd has initiated coverage on Hibiscus Petroleum Bhd with an “Outperform” rating at 47 sen and target price of RM1.06 and said Hibiscus continues to deliver production from its first producing field, the Anasuria Cluster in UK with average circa 3500bbls/day, anchoring its position more prominently amongst its oil peers.

In a note today, the research house said it remains positive on the Group’s performance, reaffirmed by its ability and perseverance to continue securing producing assets.

It said in October 2016, the Group announced another milestone, the conditional sale and purchase agreement (SPA) for the Group to acquire the 50% stake of the North Sabah Enhanced Oil Recovery (EOR) PSC.

“We are initiating coverage on Hibiscus with an Outperform call with a target price of RM1.06 premised on our sum-of-parts valuation.

“Our valuation is based on the relative undervaluation of Hibiscus’ Anasuria Cluster asset valued at RM0.58 based on our DCF valuation with an 11.0% WACC, and after close review of its upcoming North Sabah acquisition based on its 2P reserves only, we believe would add another 48 sen to the Group’s fair value,” it said.

How Iraq’s Kurdish Independence Referendum Could Impact Oil Markets

By

Angelina Rascouet

and

Khalid Al Ansary

Referendum on Kurdish independence planned for Sept. 25

Geopolitical risks abound as oil-rich region is set to vote

Does OPEC Have Any Fight Left in It?

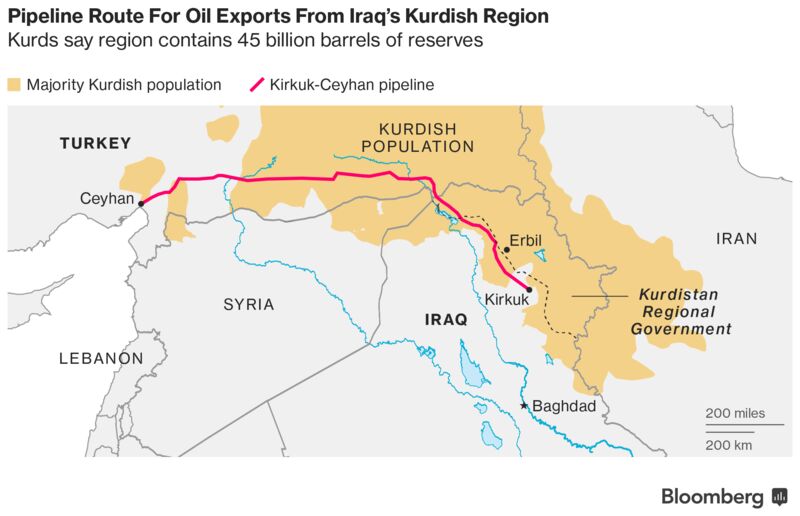

Iraq’s Kurdish provinces plan to vote in a referendum on independence on Sept. 25, a poll that regional and Western powers, not to mention the central government in Baghdad, have decried as a catalyst for greater instability in a region gutted by war. At stake are the petrodollars that have helped sustain the Kurdish Regional Government’s semi-autonomous rule after a budgetary deal with the federal government fell apart. Some of this oil wealth lies in disputed areas where the referendum will be held.

1. Why should the oil market care about this referendum?

The KRG says northern Iraq’s Kurdish enclave could hold 45 billion barrels of crude reserves, more than OPEC member Nigeria. The region pumped about 544,600 barrels of oil a day in 2016 and is expected to boost output to 602,000 barrels this year, consultant Rystad Energy said in April. Last year’s production represented about 12 percent of Iraq’s total supply, based on data compiled by Bloomberg News. These volumes alone would put the KRG on par with OPEC’s Ecuador and Qatar.

To get its oil to market, the landlocked Kurdish area relies on a pipeline to the Mediterranean port of Ceyhan, Turkey. Kurdish exports averaged 515,000 barrels a day last year, according to cargo tracking compiled by Bloomberg News. Shipments averaged 583,600 barrels a day year to date, the data show.

2. Does the referendum pose a threat to oil production?

The referendum will be held not only in the three governorates, or provinces, of the Kurdish region but also in the disputed region of Kirkuk and its oil fields, where Iraq first discovered crude in 1927. The federal government deems it illegal for the KRG to include Kirkuk in its referendum and has threatened to retaliate.

“The reactions to the referendum were childish,” Ahmed Al-Askari, head of the energy committee at the Kirkuk provincial council, said in a phone interview. “We are peaceful people and ready to negotiate for our rights.”

Kurdish forces took control of territory around the city of Kirkuk in June 2014 after the Iraqi Army fled from Islamic State militants, but Baghdad refuses to recognize Kurdish control of the area.

“We have some differences with the minister of natural resources of the KRG over the Kirkuk field,” Iraqi Oil Minister Jabbar Al-Luaibi said on Sept. 19. The KRG’s ministry of natural resources declined to respond to a Bloomberg request for comment.

Because the poll is non-binding, the International Energy Agency doesn’t “anticipate any immediate change in the status quo at this time” and will monitor developments as they unfold, it said in an emailed statement. The IEA tracks supply from the Organization of Petroleum Exporting Countries, including Iraq, OPEC’s second-biggest producer.

3. Are oil exports at risk?

The biggest risk to exports would be for neighboring Turkey -- which opposes the referendum, given it has its own restive Kurdish minority -- to shut down the pipeline that can transport as much as 700,000 barrels from Kurdish fields to Ceyhan, according to regional specialists Michael Knights of the Washington Institute and Michael Rubin of the American Enterprise Institute.

A Turkish closure of the link would wipe out recent gains in the KRG’s energy industry, Knights said, citing the Kurds’ regular payments to international oil companies in the past two years, a resolution of overdue receivables owed to some of these businesses and a proposal by Russia’s Rosneft Oil PJSC to build a natural gas pipeline in the region. The fact that the oil pipeline has operated without interruption since the Kurds announced the referendum in June should reassure energy companies, Knights said.

4. Are there risks for oil companies?

Publicly listed international oil companies operating in the Kurdish territory include Gulf Keystone Petroleum Ltd., Genel Energy Plc and DNO ASA. Gulf Keystone operates the 36,700 barrel-a-day Shaikan field, while DNO produces at the Tawke field. Around Kirkuk, a local oil company, KAR Group, operates the Khurmala, Avanna and Bai Hassan fields.

Risks to operating in the region have eased amid the progress cited by Knights of the Washington Institute and recent military advances against Islamic State in northern Iraq.

“Our industry is the most important industry in the region, and it’s in everyone’s interest to protect” it, Jon Ferrier, Gulf Keystone chief executive officer, said in an interview on Sept. 19. Officials at Genel declined to comment. DNO couldn’t immediately be reached for comment.

5. Why does Kirkuk matter?

Kurds, Arabs and Turkmens are all competing to control Kirkuk, making the city and its oil-rich area a potential flashpoint for conflict. Tensions are threatening to escalate after clashes this week between Kurds and Turkmen during an event to promote the referendum. Iraq’s parliament voted to dismiss the province’s Kurdish governor, a move KRG President Massoud Barzani said would end the partnership with Baghdad. Kirkuk fields under Kurdish control are pumping 350,000 to 400,000 barrels a day, according to Iraqi Deputy Oil Minister Fayyad Al-Nima.

“If the Kurds include Kirkuk by force in the referendum process, it will be considered then an occupied province by non-Iraqi forces, and then the prime minister will be obliged to take measures to take back these lands,” Khalid Al-Miferji, who represents Kirkuk in Iraq’s federal parliament, said in a phone interview.

塔伦

塔伦

没有评论:

发表评论