| 集团公司董事长、总经理王有德同马来西亚内贸部部长Dato Seri Hamzah进行会谈 | |

2018年1月25日下午,集团公司董事长、总经理,HRC董事局主席王有德会同公司部分高管,与马来西亚内贸部部长Dato Seri Hamzah进行了亲切会谈。

Dato Seri Hamzah部长对HRC交割一年以来所取得的成绩表示了充分肯定,他对HRC在王总带领下将取得更大更好的发展抱有足够信心,同时,希望恒源石化作为“一带一路”战略下中国企业的成功典范,能够影响和引领更多的中国优秀企业到马来投资。

王总对Dato Seri Hamzah部长长期以来给予恒源的关注、关怀和支持表示感谢,并就公司交接一年多来的表现、欧四升级项目现状、资本管理策略、公司短期及长远规划目标同部长进行了汇报。

总经理办公室宣传部

2018年2月2日

| |

a)

Hengyuan Q1 2018 - Good Margins, Good Profit

Author: david_tan | Publish date:

2018 has been a turbulent year thus far for the share price of HRC. However, is the same turbulence seen in the operations of HRC? In this article, lets attempt to estimate the profitability of HRC in the 1st Quarter of 2018.

1. SALES

In estimating sales, cost of goods sold and gross profit of HRC for Q1 2018, the 3:2:1 Crack Spread approach is highly popular and favoured. This widely used crack spread ratio is based upon the premise that 3 barrels of crude oil produce 1 barrel of gasoil (diesel) and 2 barrels of gasoline (petrol).

a. Sales Price

The daily historical data of the followings were obtained from CME Group's website for the quarter from 1 January 2018 to 31 March 2018:

- Singapore Gasoil (Platts)

- Singapore Mogas 95 Unleaded (Platts)

b. Sales Quantity

Sales volume is determined as the average of the past 8 most recent quarters (1 January 2016 to 31 December 2017). In determining this average, quarters with the highest and lowest sales volume were disregarded to eliminate unusual fluctuations.

Using the 3:2:1 Crack Spread ratio, daily diesel sales is estimated at 36,790 barrels while daily petrol sales amounted to 73,580 barrels.

c. Sales In RM

Daily sales price extracted in US$ were converted to RM using daily foreign exchange rates extracted from Bank Negara's website. The daily sales price in RM is then multiplied with the sales quantity of diesel and petrol respectively on a daily basis, giving a sales revenue of RM3,058,775,000 for the quarter.

Note: Detailed daily sales calculation has not been included here as it is voluminous.

2. COST OF GOODS SOLD

Cost of goods sold is determined as Opening Inventories + Purchases - Closing Inventories.

a. Opening Inventories

Based on the latest breakdown of inventories available as at 31 December 2016, 56% of inventories was that of crude oil, 41% of refined products while the balance 3% was of other materials. Applying this ratio (but ignoring the insignificant 3% of other materials), the breakdown of inventories as at 31 December 2017 is estimated as below:

Cost of diesel and petrol is calculated based on Q4 2017 gross profit margin of 11.5%.

b. Puchases

For presentation purpose, it is assumed that daily crude oil used in production of 110,370 barrels is purchased and replenished on a daily basis.

As in the sales estimation above, daily prices of Brent Crude Oil were extracted in US$ and translated into RM using daily foreign exchange rates. This figure is then multiplied with daily sales of 110,370 barrels of crude oil, giving total purchases of RM2,624,104,000.

Note: Detailed daily purchases calculation has not been included here as it is voluminous.

c. Closing Inventories

For direct comparison, physical closing inventories is maintained per physical opening inventories.

The opening inventories of 2.6m barrels of crude oil is able to last daily production consumption of 110,370 barrels for 24 days. At daily crude oil purchases of 110,370 barrels per day, closing inventories of crude oil is calculated based on daily prices of Brent Crude Oil extracted (in US$ and translated into RM using daily foreign exchange rates) for the last 24 days of March 2018 giving a value of RM707,805,000.

For apple to apple comparison, gross profit margin of diesel and petrol are maintained at 11.5%.

Note: Detailed daily purchases calculation for the last 24 days of Q1 2018 has not been included here as it is voluminous.

3. OTHER INCOME

Other income is determined as the average of the past 8 most recent quarters (1 January 2016 to 31 December 2017). In determining this average, quarters with the highest and lowest other income were disregarded to eliminate unusual fluctuations.

4. MANUFACTURING EXPENSES

a. Manufacturing expenses is determined as the average of the past 8 most recent quarters (1 January 2016 to 31 December 2017). In determining this average, quarters with the highest and lowest manufacturing expenses were disregarded to eliminate unusual fluctuations.

b. Manufacturing expenses for Q2 2017 was normalised due to expenses incurred for an unplanned maintenance shutdown. Manufacturing expenses is adjusted accordingly based on number of production days.

5. ADMINISTRATIVE EXPENSES

Administrative expenses is determined as the average of the past 8 most recent quarters (1 January 2016 to 31 December 2017). In determining this average, quarters with the highest and lowest administrative expenses were disregarded to eliminate unusual fluctuations.

6. DEPRECIATION AND AMORTISATION

Depreciation and amortisation expenses are determined as the average of the past 8 most recent quarters (1 January 2016 to 31 December 2017). In determining this average, quarters with the highest and lowest depreciation and amortisation expenses were disregarded to eliminate unusual fluctuations.

7. OTHER OPERATING GAINS

On 23 January 2018, HRC took a new term loan amounting to US$430m (RM1.7b) to refinance existing term loans, to finance the planned 2018 capital expenditure and a revolving credit facility for working capital purposes.

As at 31 December 2017, the outstanding US$ denominated term loans amounted to RM1,205,008,000. The foreign exchange on that date was 4.0620. The exchange rate as at 23 January 2018 was 3.9270. Assuming the new term loan was drawndown for full repayment on the said date, the realised foreign exchange gain for HRC amount to RM40,048,000.

8. FINANCE COST

Finance cost is determined as the average of the past 8 most recent quarters (1 January 2016 to 31 December 2017).In determining this average, quarters with the highest and lowest finance cost were disregarded to eliminate unusual fluctuations.

9. PROFIT BEFORE TAXATION

10. TAXATION EXPENSE

Depreciation is assumed as capital allowance for taxation purpose.

11. PROFIT AFTER TAXATION FOR Q1 2018

b)

HENGYUAN (Not Rated)

1. SALES

In estimating sales, cost of goods sold and gross profit of HRC for Q1 2018, the 3:2:1 Crack Spread approach is highly popular and favoured. This widely used crack spread ratio is based upon the premise that 3 barrels of crude oil produce 1 barrel of gasoil (diesel) and 2 barrels of gasoline (petrol).

a. Sales Price

The daily historical data of the followings were obtained from CME Group's website for the quarter from 1 January 2018 to 31 March 2018:

- Singapore Gasoil (Platts)

- Singapore Mogas 95 Unleaded (Platts)

b. Sales Quantity

Sales volume is determined as the average of the past 8 most recent quarters (1 January 2016 to 31 December 2017). In determining this average, quarters with the highest and lowest sales volume were disregarded to eliminate unusual fluctuations.

Using the 3:2:1 Crack Spread ratio, daily diesel sales is estimated at 36,790 barrels while daily petrol sales amounted to 73,580 barrels.

c. Sales In RM

Daily sales price extracted in US$ were converted to RM using daily foreign exchange rates extracted from Bank Negara's website. The daily sales price in RM is then multiplied with the sales quantity of diesel and petrol respectively on a daily basis, giving a sales revenue of RM3,058,775,000 for the quarter.

Note: Detailed daily sales calculation has not been included here as it is voluminous.

2. COST OF GOODS SOLD

Cost of goods sold is determined as Opening Inventories + Purchases - Closing Inventories.

a. Opening Inventories

Based on the latest breakdown of inventories available as at 31 December 2016, 56% of inventories was that of crude oil, 41% of refined products while the balance 3% was of other materials. Applying this ratio (but ignoring the insignificant 3% of other materials), the breakdown of inventories as at 31 December 2017 is estimated as below:

Cost of diesel and petrol is calculated based on Q4 2017 gross profit margin of 11.5%.

b. Puchases

For presentation purpose, it is assumed that daily crude oil used in production of 110,370 barrels is purchased and replenished on a daily basis.

As in the sales estimation above, daily prices of Brent Crude Oil were extracted in US$ and translated into RM using daily foreign exchange rates. This figure is then multiplied with daily sales of 110,370 barrels of crude oil, giving total purchases of RM2,624,104,000.

Note: Detailed daily purchases calculation has not been included here as it is voluminous.

c. Closing Inventories

For direct comparison, physical closing inventories is maintained per physical opening inventories.

The opening inventories of 2.6m barrels of crude oil is able to last daily production consumption of 110,370 barrels for 24 days. At daily crude oil purchases of 110,370 barrels per day, closing inventories of crude oil is calculated based on daily prices of Brent Crude Oil extracted (in US$ and translated into RM using daily foreign exchange rates) for the last 24 days of March 2018 giving a value of RM707,805,000.

For apple to apple comparison, gross profit margin of diesel and petrol are maintained at 11.5%.

Note: Detailed daily purchases calculation for the last 24 days of Q1 2018 has not been included here as it is voluminous.

3. OTHER INCOME

Other income is determined as the average of the past 8 most recent quarters (1 January 2016 to 31 December 2017). In determining this average, quarters with the highest and lowest other income were disregarded to eliminate unusual fluctuations.

4. MANUFACTURING EXPENSES

a. Manufacturing expenses is determined as the average of the past 8 most recent quarters (1 January 2016 to 31 December 2017). In determining this average, quarters with the highest and lowest manufacturing expenses were disregarded to eliminate unusual fluctuations.

b. Manufacturing expenses for Q2 2017 was normalised due to expenses incurred for an unplanned maintenance shutdown. Manufacturing expenses is adjusted accordingly based on number of production days.

5. ADMINISTRATIVE EXPENSES

Administrative expenses is determined as the average of the past 8 most recent quarters (1 January 2016 to 31 December 2017). In determining this average, quarters with the highest and lowest administrative expenses were disregarded to eliminate unusual fluctuations.

6. DEPRECIATION AND AMORTISATION

Depreciation and amortisation expenses are determined as the average of the past 8 most recent quarters (1 January 2016 to 31 December 2017). In determining this average, quarters with the highest and lowest depreciation and amortisation expenses were disregarded to eliminate unusual fluctuations.

7. OTHER OPERATING GAINS

On 23 January 2018, HRC took a new term loan amounting to US$430m (RM1.7b) to refinance existing term loans, to finance the planned 2018 capital expenditure and a revolving credit facility for working capital purposes.

As at 31 December 2017, the outstanding US$ denominated term loans amounted to RM1,205,008,000. The foreign exchange on that date was 4.0620. The exchange rate as at 23 January 2018 was 3.9270. Assuming the new term loan was drawndown for full repayment on the said date, the realised foreign exchange gain for HRC amount to RM40,048,000.

8. FINANCE COST

Finance cost is determined as the average of the past 8 most recent quarters (1 January 2016 to 31 December 2017).In determining this average, quarters with the highest and lowest finance cost were disregarded to eliminate unusual fluctuations.

9. PROFIT BEFORE TAXATION

10. TAXATION EXPENSE

Depreciation is assumed as capital allowance for taxation purpose.

11. PROFIT AFTER TAXATION FOR Q1 2018

b)

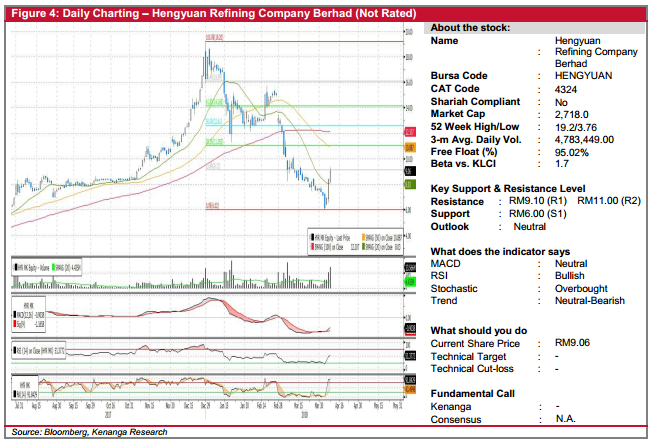

HENGYUAN (Not Rated)

- HENGYUAN surged 71.0 sen (8.5%) to end at RM9.06. This was accompanied by 13.6m shares being traded – above average volume of 4.4m shares.

- Positive movements in the past three days, backed by indicating strong volumes could indicate a potential bottoming-out.

- Likewise, momentum indicators also displayed signals of possible reversal, i.e. RSI rebounded strongly from oversold territory, with uptick seen in the MACD.

- The share is currently in the midst of testing its resistance at RM9.10 (R1). A break out from R1 could spark a further rally towards RM11.00 (R2) and RM12.60 (R3) further up.

- Conversely, RM6.00 (S1) represents a crucial support, in which a break below is highly negative and could possibly trigger another round of free fall.

Source: Kenanga Research - 10 Apr 2018

c)

Stallion - HengYuan Outlook 8 April 2018

Author: StallionInvestment | Publish date:

After my earlier posting on the drop of HengYuan, some followers were asking me how do I see in HengYuan. So, I am here to provide in depth analysis on this stock.

As I said earlier, I did warn that it is ridiculous when it was trading at the price near to 19. It justify my view by the drop from 19 to 6. So, now is the rebound phase and this has trigger the interest of the followers. Especially when Mr. Koon said he is coming back into HengYuan, this give the retail trader a confident booster.

I will see HengYuan from two different angles which I will elaborate at below.

Let see from Fundamental point of view :

Fourth Quarter result release showing that a small improvement of revenue but profit drop approximately 50% which you can see earlier quarter EPS was 120.59 compare to the most recent quarter which is only 61.18. So, from this we notice the business remain the same but what is curious is the drop of nearly 50% of the profit which require you dig out more info from the quarterly report. So, coming quarter most likely will be release on 24 May 2018 base on the historical release date. Unless you are pretty confident which HengYuan will resume the growth momentum for the revenue and profit, else it will be risky to hold on your position unless got more than 20% PROFIT as your buffer.

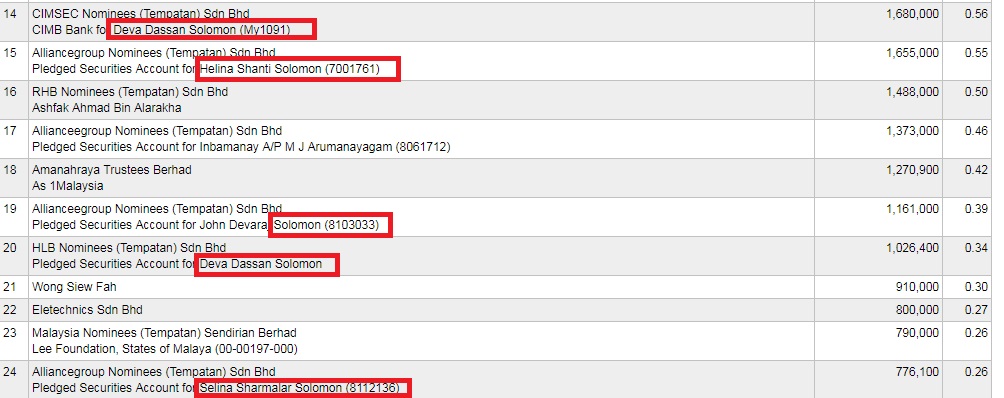

From the top 30 major shareholders which we notice Solomon holders name do appear very frequent as I printscreen attach as below. Name such as Deva Dassan Solomon, Helina Shanti Solomon, John Devaraj Solomon, Selina Sharmalar Solomon. Beside, Mr Koon Yew Yin, we should watch out closely Solomon family transaction.

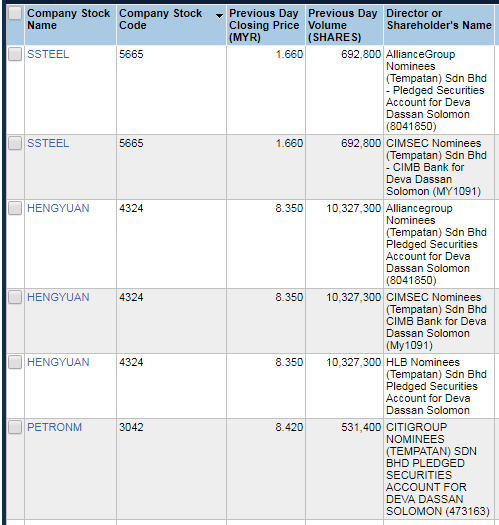

Below I provide the screen capture of using Insage Professional showing Deva Dassan Solomon shareholding we could find the stock he is holding is SSteel, HengYuan and Petronm.

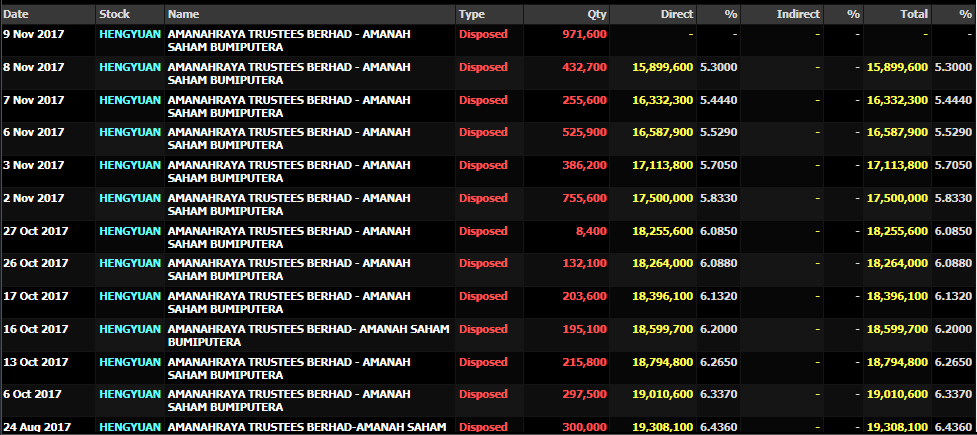

On top of that, we do notice actively disposal of HengYuan by Amanahraya Trustee Berhad – Amanah Saham Bumiputra. When the shareholding go below 5%, then it can move wild. Early alert for fellow HengYuan Trader. Technically speaking, the game is not over even with such huge drop from 19 to 6.

Technical Point of View :

It fulfill my 1 Cross 4 criteria ( Do attend M+Online Technical 101 course ) to capture the entry level detection.

Conclusion : if there is no external factor such as TRADE WAR getting serious, my personal view is HengYuan should ride on the uptrend then don’t hold when near to next quarter result date. That is my personal opinion.

d)

As I said earlier, I did warn that it is ridiculous when it was trading at the price near to 19. It justify my view by the drop from 19 to 6. So, now is the rebound phase and this has trigger the interest of the followers. Especially when Mr. Koon said he is coming back into HengYuan, this give the retail trader a confident booster.

I will see HengYuan from two different angles which I will elaborate at below.

Let see from Fundamental point of view :

Fourth Quarter result release showing that a small improvement of revenue but profit drop approximately 50% which you can see earlier quarter EPS was 120.59 compare to the most recent quarter which is only 61.18. So, from this we notice the business remain the same but what is curious is the drop of nearly 50% of the profit which require you dig out more info from the quarterly report. So, coming quarter most likely will be release on 24 May 2018 base on the historical release date. Unless you are pretty confident which HengYuan will resume the growth momentum for the revenue and profit, else it will be risky to hold on your position unless got more than 20% PROFIT as your buffer.

From the top 30 major shareholders which we notice Solomon holders name do appear very frequent as I printscreen attach as below. Name such as Deva Dassan Solomon, Helina Shanti Solomon, John Devaraj Solomon, Selina Sharmalar Solomon. Beside, Mr Koon Yew Yin, we should watch out closely Solomon family transaction.

Below I provide the screen capture of using Insage Professional showing Deva Dassan Solomon shareholding we could find the stock he is holding is SSteel, HengYuan and Petronm.

On top of that, we do notice actively disposal of HengYuan by Amanahraya Trustee Berhad – Amanah Saham Bumiputra. When the shareholding go below 5%, then it can move wild. Early alert for fellow HengYuan Trader. Technically speaking, the game is not over even with such huge drop from 19 to 6.

Technical Point of View :

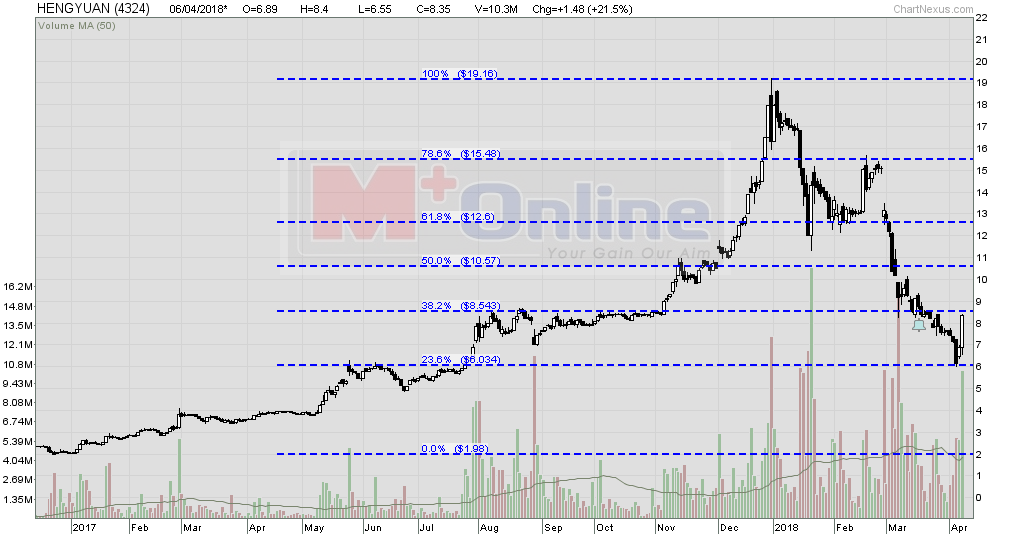

- HengYuan started the rally early year 2017 from the level 1.98 till 19.16. So, I am plotting the chart using Fibonacci Retracement which show you each support resistance if you have the basic knowledge how to read this. So, the first resistance level peg at 8.54. When it able to penetrate this level then we shall look at the psychological resistance at 10. If able to breakout with strong volume together with buying interest, then I am at 10.50 as the next resistance. From this level onward, I think anything go above will be extra for you. There is such thing in technical reading call cover gap. So, if would to cover previous gap down, then it is likely to rebound as high as 14. I would not expect it break above 15.48 level because if break this level. Then we can see bullish momentum and this definitely need to come together with a good revenue and profit. If this don’t happen, to me. 14 is more than enough. Nothing more than that. Anyone making more than 14 is crazy profit. You are rewarded for holding longer position than other.

It fulfill my 1 Cross 4 criteria ( Do attend M+Online Technical 101 course ) to capture the entry level detection.

Conclusion : if there is no external factor such as TRADE WAR getting serious, my personal view is HengYuan should ride on the uptrend then don’t hold when near to next quarter result date. That is my personal opinion.

d)

HENGYUAN: Can Hengyuan pay better dividend?

Author: Sslee | Publish date:

Dear all,

If your look into Hengyuan Q4 2017 financial report.

http://www.bursamalaysia.com/market/listed-companies/company-announcements/5705361

USD as at 31.12.2017 RM equivalent: RM 1,205,008,000.

USD exchange rate on 31/12/2017 1 USD = 4.0592

http://hrc.com.my/index.php/hengyuan-refining-company-berhad-secures-favourable-financing-of-rm1-7-billion-usd430-million/

This was announced on 23-1-2018. Highlight below.

“The facilities are segregated into a term loan and a revolving credit line. The term loan will be utilised towards refinancing HRC’s existing term loan and also to partially finance its planned capital expenditure. The revolving credit facility will support the company’s working capital needs. The term loan will be repaid in instalments throughout the tenure of the 5 year facility. Approval for the facilities was received from Bank Negara Malaysia on 22 January 2018.”

This mean from the date Hengyuan refinance the USD loans with RM loans Hengyuan will not have any mark to market gain/loss in the USD loan to equivalent RM anymore.

Assume actual refinancing loans and repayment on USD loans was done on 1st Feb 2018.

USD exchange rate at 1-2-2018 1 USD =3.9004.

If we base on exchange rate different at 31-12-2017 and 1-2-2018. This Q1 2018 will have USD loan realized gain of RM 1,205,008,000 X ((4.0592-3.9004)/4.0592))= RM47, 141,128.

I believe the S&P long term contract signed with Shell is base of Petrol/Diesel pricing = Crude oil Price + Crack Spread. Crude oil price and Crack Spread will be base on mutually agreed publication available to public and settlement on monthly basis with weightage average of daily price and spread. Will seek board confirmation on the actual formula and which mutual agreed publication in reference to crude oil price and Crack spread? What is the breakeven crack spread?

This S&P contract was agree upon when the petrol and diesel retail price was fixed by Government on monthly basis since then it had been changed to weekly basis hence perhaps Hengyuan have the right to renegotiate to weekly settlement with credit term of 10 days instead of 1 month. If this is done then the trade receivable will reduce from RM 1.08 billion to 370 million an addition cash in bank of 710 million.

With the support of own jetty and pipeline and 78 refined product storage tanks and ability to import the refined products from China to fulfill contract with Shell. (As what they already plan to do with booked refine products at preferred rate during the major turnaround shutdown in Aug 2018 from 45 to 90 days max) Perhaps Hengyuan can reduce their inventory from 16 days cycle to 11 days cycle. Hence inventory can be reduced from RM 1.11 billion to 763 million an addition cash in bank of RM 347 million.

Hope this will answer everyone question whether Hengyuan have the ability to pay better dividend or Not?

Thank you. Have a nice week end.

If your look into Hengyuan Q4 2017 financial report.

http://www.bursamalaysia.com/market/listed-companies/company-announcements/5705361

- Inventories RM 1,110,315,000

- Trade Receivable RM 1,080,401,000

- Other receivable and prepayments RM 166,296,000

- Deposits with licensed banks RM 210,000,000

- Bank Balance RM 302,907,000

- Trade and other payable RM 601,497,000

- Borrowing: Non Current RM 1,125,905,000 Current RM 79,103,000

USD as at 31.12.2017 RM equivalent: RM 1,205,008,000.

http://hrc.com.my/index.php/hengyuan-refining-company-berhad-secures-favourable-financing-of-rm1-7-billion-usd430-million/

This was announced on 23-1-2018. Highlight below.

“The facilities are segregated into a term loan and a revolving credit line. The term loan will be utilised towards refinancing HRC’s existing term loan and also to partially finance its planned capital expenditure. The revolving credit facility will support the company’s working capital needs. The term loan will be repaid in instalments throughout the tenure of the 5 year facility. Approval for the facilities was received from Bank Negara Malaysia on 22 January 2018.”

This mean from the date Hengyuan refinance the USD loans with RM loans Hengyuan will not have any mark to market gain/loss in the USD loan to equivalent RM anymore.

Assume actual refinancing loans and repayment on USD loans was done on 1st Feb 2018.

USD exchange rate at 1-2-2018 1 USD =3.9004.

If we base on exchange rate different at 31-12-2017 and 1-2-2018. This Q1 2018 will have USD loan realized gain of RM 1,205,008,000 X ((4.0592-3.9004)/4.0592))= RM47, 141,128.

I believe the S&P long term contract signed with Shell is base of Petrol/Diesel pricing = Crude oil Price + Crack Spread. Crude oil price and Crack Spread will be base on mutually agreed publication available to public and settlement on monthly basis with weightage average of daily price and spread. Will seek board confirmation on the actual formula and which mutual agreed publication in reference to crude oil price and Crack spread? What is the breakeven crack spread?

This S&P contract was agree upon when the petrol and diesel retail price was fixed by Government on monthly basis since then it had been changed to weekly basis hence perhaps Hengyuan have the right to renegotiate to weekly settlement with credit term of 10 days instead of 1 month. If this is done then the trade receivable will reduce from RM 1.08 billion to 370 million an addition cash in bank of 710 million.

With the support of own jetty and pipeline and 78 refined product storage tanks and ability to import the refined products from China to fulfill contract with Shell. (As what they already plan to do with booked refine products at preferred rate during the major turnaround shutdown in Aug 2018 from 45 to 90 days max) Perhaps Hengyuan can reduce their inventory from 16 days cycle to 11 days cycle. Hence inventory can be reduced from RM 1.11 billion to 763 million an addition cash in bank of RM 347 million.

Hope this will answer everyone question whether Hengyuan have the ability to pay better dividend or Not?

Thank you. Have a nice week end.

没有评论:

发表评论