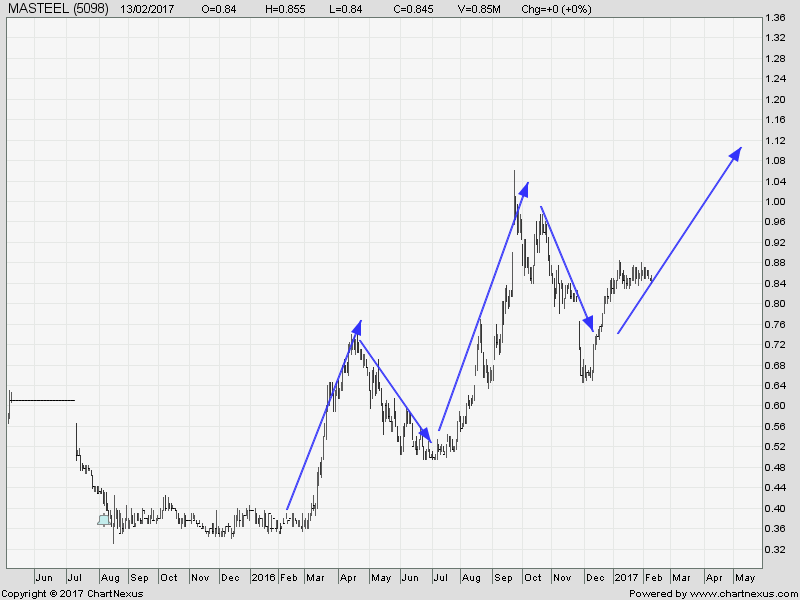

--估计2017 年6月财年的Eps =23-25 sen,pe=8,stock price=rm 1.84-2.00

--5665 这次100%可赚$,之前同行6556 annjoo(長钢),5094cscstel (扁钢)都大跑了.

随着南钢净利報捷,股价有望補上.

--公司于31-12-2016 的库存有5.33亿零吉,债务为9.45亿.

现金有5951万,累计净利有9576万.

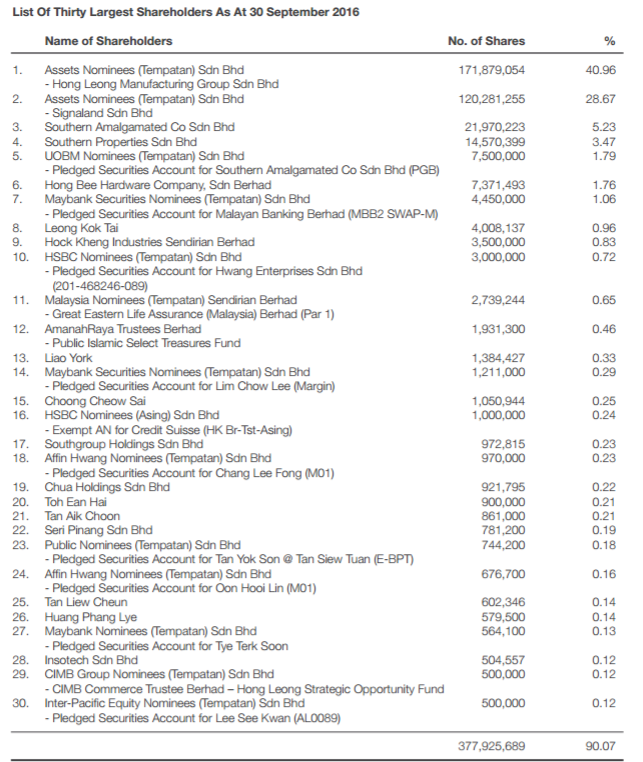

--公司于30-9-2016的30大股东共持有377925,600股份(90.07%),总股数为422,751m

股价一旦开跑是很快的. 丰隆集团牢控69.63%

--中国己对许多商品有绝对的定价权,螺蚊钢就是其中一项,一帶一路下,

产能减等是支持钢价利好。看來将有一些年的好景。

--现rolling 4 quarter 的Eps是亏損 15sen,当Q3,Q4 季报出后将呈現 EPs=23~25 sen ,

市場信心后股价就不是现在的rm1.43 了。

只供参考,投资自负.

http://southsteel.com/

http://www.100ppi.com/vane/detail-927.html

(2017财政年第2财报)

以下图表是之前4个季度的收支表。

2016第4季度的营业额上升,

当然和中盘商多买了一些货有关,

如果2016第4季度不买,

那2017年第一季度钢铁产品更贵了。

很多人说,长钢贵大不了不买。

那是外行人说的话。

在建筑工地,最贵的开销就是工人薪水。

还有各种租借的器材。

早一天完工,盈利就多。

为了钢筋起价,不买?

工钱不用给呐? 灌水泥也很花时间凝固。

Ssteel连续4个季度,Gross Profit 上升。

Operating Expenses 在最高营业额的第三季,

反而不是最高。

如果懂Fix Cost,Variable Cost, Output 之间的关系,

就动为什么了。这里不谈,因为不是上课。

2016第2季度的机械减记,

是因为引进错误和失败的机械。

大约1.34亿,而导致大亏损。

这个真的很好笑,

因为我在这个业界呆过,

这是乌龙事件。

如果没有减记,2016基本上第2季度也能赚个3千多万。

看得出,2016年最新出炉的第4季度报告,

比没有减记的2季度报告更好。

这很重要,为什么呢?

因为2016年4月-6月的时候,

钢铁因为缺货而价格狂飙。

7-9月时价格下跌。

而10-12月时,长钢价格又狂飙。

加上9月尾实施的长钢保护税,

所以2016年第4季度的成绩

比第2季度有过之而无不及。

从以上的BS, 可以看出第二季度PPE的减记。

也可以看出库存大约维持在5亿。

大月一个季度的库存。

应收款项没有增加,好事。

短期债务借贷减少一点,好事。

长期应付款项减少,但是长期借贷上升,

剩下10个交易日,以上的图表,

PBT/REVENUE 将被填满。

目前已经知道CSCSTEL和SSTEEL的了。

4)

--5665 这次100%可赚$,之前同行6556 annjoo(長钢),5094cscstel (扁钢)都大跑了.

随着南钢净利報捷,股价有望補上.

--公司于31-12-2016 的库存有5.33亿零吉,债务为9.45亿.

现金有5951万,累计净利有9576万.

--公司于30-9-2016的30大股东共持有377925,600股份(90.07%),总股数为422,751m

股价一旦开跑是很快的. 丰隆集团牢控69.63%

--中国己对许多商品有绝对的定价权,螺蚊钢就是其中一项,一帶一路下,

产能减等是支持钢价利好。看來将有一些年的好景。

--现rolling 4 quarter 的Eps是亏損 15sen,当Q3,Q4 季报出后将呈現 EPs=23~25 sen ,

市場信心后股价就不是现在的rm1.43 了。

只供参考,投资自负.

http://southsteel.com/

http://www.100ppi.com/vane/detail-927.html

多谢下列的分享人,感恩---

1)长钢四侠 之 长钢三叠浪 【ANNJOO SSTEEL MASTEEL LIONIND】

Author: zefftan | Publish date: Tue, 14 Feb 2017, 01:06 AM

灵感来源 【风景画 : 位于中国重庆的 长江三峡, 风景优美】

本文论及的股项 长钢四侠【ANNJOO SSTEEL MASTEEL LIONIND】

今天2月13日, CSCSTEL 中钢发布了业绩,结果是很多高位买入的朋友都失望了,很多人都在斟酌明天是否要抛售手上的股票。

值得安慰的是, 如预期一般宣布了超高诱人股息 14 cent , 对目前股价,周息率 6%++ ,还是起到了一定的防护作用。

(声明: 本人手上已无中钢股票)

这时很多人的心中都掀起了涟漪,钢潮是否已退? 钢铁股要 gap down 了 ?

我看未必,很多人都并不是很了解整个钢铁领域,很多人以为后面有个STEEL 或者 METAL的都从事同样的生意,其实不然。以下这个图表分析了市场上的一些钢铁股项。

(摘自网络)

一小部分的宏观大马钢铁领域

最基本的,我们应该知道,马来西亚钢铁领域普遍上则分为 长钢 (REBAR / WIRE ROD) , 扁钢 ( C.R COIL) ,成品钢

长钢 (REBAR / WIRE ROD) 公司 比如 :ANNJOO , SSTEEL, LIONIND , MASTEEL

扁钢 ( C.R COIL) 公司 比如 :CSCSTEL , MYCRON , YKGI ,EMETALL(少量)

这二者看似相同,实为不同.

我的看法,中钢margin的忽退无法与长钢公司的盈利挂上等号。

这是因为如果要制作 扁钢, 原料(热轧钢HRC) 必须尤外国进口,在去年Q4特朗普竞选期间马币兑美元狂泻 导致这些扁钢制造者必须承担一次性的外汇亏损,进而导致margin 被拉低,因为原料贵了。

据我的观察,本地扁钢制造者过去几年所面对的大问题是LIONCOR售卖的HRC价钱昂贵,所以导致扁钢业者没有margin,现在好不容易LIONCOR倒闭了,以为可以进口到便宜的HRC, 哪里知道外汇因素和HRC涨价因素,而造成进口的HRC无法像以往般便宜。

LIONCOR的倒闭事件导致有些公司原料短缺,(注明:LIONCOR是马来西亚唯一的HRC提供者,在9月-10月期间宣布打包),所以如果一些原料储备不够的公司在不得已的情况下必须利用高汇率来购买昂贵原料。

鉴于此,MYCRON YKGI 有可能会步CSCSTEL 后尘, 交出令人 O_O 的业绩.。

可是,长钢业者就不同了,长钢业者这几年面对的问题是来自于中国的廉价长钢。2016年9月尾,政府对进口长钢实施了进口税 (ANTI DUMPING POLICY),导致进口的长钢更贵了,无法媲美本地价钱,而很多长钢使用者比如建筑公司就迫不及待吨多一些货,这个举动助长了需求,而本地长钢业者也得到进一步调高产品的机会,单单是Q4,长钢价格就涨了大约20%左右。(传统上Q4需求比较少,所以钢铁价格都会回调)。 这意味着长钢业者必然得到很好的profit margin,所以即将来临的业绩报告都值得我们期待。

领域催化剂:各项大型基建工程, 比如捷运2线 (KVMRT2), 东海岸铁路(ECRW),西海岸高速公路(WCE)

来看个股 长钢四侠

ANNJOO 安裕 - 位于北马,拥有国内最先进领先的生产线,profit margin 最高 , 库存量最高 , 带头大哥

SSTEEL 南钢 - 位于北马,据说生产出来的产品素质堪称一绝,价格也比较贵,生意也做得比ANNJOO大

MASTEEL 马钢 - 位于中马,四个里面最小规模

LIONIND 金狮 - 位于中马,生意量最大,政治裙带强

无可否认,ANNJOO,SSTEEL, 和 MASTEEL 都是大可能性持续获利的公司,而且即将来临的业绩有机会是爆炸性的,毕竟Q4产品平均涨价了10-20% 不等。如果这三个股都持续获利,那么所谓的 re-rating 就有可能降临了。

至于LIONIND 我对它的业绩还比较保守因为它的库存量Q3的时候貌似不多,但是此股具备黑马本色,毕竟LIONCOR的苏州屎已经告一段落,该impair的loss也都已经报销了。相信FY2017 LIONIND 应该有机会背水一战,反败为胜,毕竟也是钟廷森爷子的最后堡垒。

值得关注的是,ECRW 是一项亟需耗铁的一项工程,工程大机会由强国公司包办了,但是原料方面应该不会千里迢迢运过来,所以本地钢厂应该有得分一杯。纵观东海岸钢铁厂,比如PERWAJA 和 KINSTEL 应该无法竞争,所以剩下的机会应该是中马那两间。

结论

综合以上观点,我觉得长钢个股不应该被扁钢个股行情所拖累,反之有机会坂下一城。

何谓长钢三叠浪 ?

请看下图

有没有看到共同点?

参考:

共勉之

ZEFF TAN

2)

Why rally in steel stocks is far from over

This article first appeared in The Edge Financial Daily, on February 13, 2017.

KUALA LUMPUR: Many metal stocks have risen sharply of late, mainly due to improving sentiment for commodities in general, supported by China’s commitment to tackle current excess capacity in its steel sector.

A check on 25 steel companies listed on Bursa Malaysia shows that more than half are trading at double-digit price-earnings ratios (PER), ranging from 10.33 times to as high as 74.32 times.

Among the big players, YKGI Holdings Bhd and FACB Industries Incorporated Bhd are trading at PERs of 74.32 times and 25.28 times, respectively.

In theory, the higher the PER ratio, the more expensive the stock. However, analysts see opportunity for investors to get into selective stocks for dividend play.

According to them, as steel prices continue to rally leading to some steel stocks’ prices to triple over the past year, a valuation gap is seen emerging that may open the door for an opportunistic dividend play.

“If things remain status quo, the mid-tier stocks are bound to catch up eventually [in terms of PER valuation],” a senior industry executive told The Edge Financial Daily.

“There could be opportunities for dividend play [as the steel companies’ earnings rebound following years of grappling with the surge of cheap Chinese imports into the local market], especially when a number of companies in the space are family controlled,” he added. Traditionally, family-controlled firms are seen paying some of the highest dividend payouts.

But that’s assuming these family-controlled steel companies whose valuation is lagging behind top-tier stocks, see a surge in profit and their share price continue to improve.

Taking away stocks with PERs at the extreme end such as YKGI and Tatt Giap Group Bhd’s 0.6 times, there are currently four steel stocks trading at single-digit PERs comprising Mycron Steel Bhd (8.87 times), CSC Steel Holdings Bhd (8.56 times), Leon Fuat Bhd (7.99 times) and Eonmetall Group Bhd (5.99 times).

According to the Malaysian Iron and Steel Industry Federation, imports of steel products from China surged 281% to 3.44 million tonnes in 2015 from 904,000 tonnes in 2010 after the Asean China Free Trade Agreement took effect in January 2010.

When contacted, several fund managers and analysts concurred that there is an opportunity for dividend play among the steel stocks, although some remained sceptical due to the cyclical nature of the steel sector which makes dividend payouts not sustainable in the long run.

In February this year, China announced that it will work to cut steel output by up to 150 million tonnes although it did not specify a time frame. The move will cut 500,000 jobs in the steel sector alone, Bloomberg quoted China’s human resources ministry as saying.

China has also committed 100 billion yuan over two years to aid retrenchment schemes, although this fund is also intended for job cuts in the coal sector.

These developments have helped steel prices in Malaysia to recover, alongside rising energy prices and local safeguard duties announced in September for rebar imports. The duties, which took effect for 200 days beginning Sept 26, 2016, are 13.9% for steel coils and 13.4% for reinforced bars respectively. The safeguard duties would be reviewed again in April, according to news reports.

“There were questions about whether China would really hurt its own steel production, but they have been cutting and seem to have the resolve to do this,” said a senior analyst with a local bank-backed research house.

“If the steel production capacity continues to fall, then yes, the worst is over [for Malaysian steel players],” he added.

According to a monthly survey by the Construction Industry Development Board, mild steel round bars in Selangor averaged just under RM2,500 a tonne last December, compared with RM1,800 a tonne a year ago.

“For cyclical sectors such as steel, dividends would be a bonus,” the senior analyst said.

However, two senior fund managers warned that this may not mean the sector is heading in the direction of recovery. They pointed to steel players’ tight cash flow and compressed margins in a high-capital business environment.

For one fund manager, that casts doubt on dividend hopes in general, as any dividend would “depend on [the company’s] cash flow. Their cash flow is very much affected by the commodity cycle and is very hard to predict.”

Do steel stocks still have legs?

While a couple of market observers opined that the steel recovery prospects in general have not been fully priced in, they are of the view that the cheaper buys in the sector have all been taken.

“The lowest phase has clearly passed and every day the rally continues, the more uncertain it becomes on where we are at the current upcycle,” noted one market observer. “Everyone is assuming things will recover and that things in the steel sector will remain the status quo. But the market is ignoring [possible risks] ahead.”

They include uncertainty over what US President Donald Trump might do amid signals of increasing protectionism from the world’s largest economy.

“The very obvious risk is what would Trump do? If he puts a border tax across the board on imports, a lot of our steel exports can’t get into the US. Our steel exports are not big, but it would impact global steel prices and that would spill over into our steel sector,” said one analyst.

In addition, while steel product prices have recovered, demand outlook is mixed.

A fund manager opined that while major infrastructure projects announced by the government may support demand, that boost is offset by a slowdown in the housing sector, another primary driver.

Such infrastructure works include the Mass Rapid Transit project and the upcoming RM55 billion new East Coast Rail Line that will connect the Klang Valley to the East Coast via 600km of rail tracks.

The Malaysian Steel Institute (MSI), an agency under the ministry of international trade and industry (Miti), estimates a full-year steel products consumption of at least 10.4 million tonnes in 2017, slightly higher than the expected figure for 2016 which will only be confirmed after December’s data is released in early March.

It is understood that MSI and Miti have been pushing to promote the use of local steel products in construction works to boost consumption of the local steel sector’s output.

For investors looking at value buys amid the ongoing rally in the steel sector, a key factor to watch out for is the cost structure, said several fund managers.

This means examining the sub-niches of each player, their type of facilities and comparing them against direct peers. In addition, a look at major shareholdings may add another dimension of interest for those looking to bet on dividends from a potential year of earnings recovery.

“The more efficient players would have a higher net profit margin,” said another analyst. “Also look at how good the management are and how new is their steel milling facilities — newer usually means more efficient.”

3)

Tuesday, 14 February 2017

分析南钢2016第4季度财报!

(2017财政年第2财报)

以下图表是之前4个季度的收支表。

2016第4季度的营业额上升,

当然和中盘商多买了一些货有关,

如果2016第4季度不买,

那2017年第一季度钢铁产品更贵了。

很多人说,长钢贵大不了不买。

那是外行人说的话。

在建筑工地,最贵的开销就是工人薪水。

还有各种租借的器材。

早一天完工,盈利就多。

为了钢筋起价,不买?

工钱不用给呐? 灌水泥也很花时间凝固。

Ssteel连续4个季度,Gross Profit 上升。

Operating Expenses 在最高营业额的第三季,

反而不是最高。

如果懂Fix Cost,Variable Cost, Output 之间的关系,

就动为什么了。这里不谈,因为不是上课。

2016第2季度的机械减记,

是因为引进错误和失败的机械。

大约1.34亿,而导致大亏损。

这个真的很好笑,

因为我在这个业界呆过,

这是乌龙事件。

如果没有减记,2016基本上第2季度也能赚个3千多万。

看得出,2016年最新出炉的第4季度报告,

比没有减记的2季度报告更好。

这很重要,为什么呢?

因为2016年4月-6月的时候,

钢铁因为缺货而价格狂飙。

7-9月时价格下跌。

而10-12月时,长钢价格又狂飙。

加上9月尾实施的长钢保护税,

所以2016年第4季度的成绩

比第2季度有过之而无不及。

从以上的BS, 可以看出第二季度PPE的减记。

也可以看出库存大约维持在5亿。

大月一个季度的库存。

应收款项没有增加,好事。

短期债务借贷减少一点,好事。

长期应付款项减少,但是长期借贷上升,

剩下10个交易日,以上的图表,

PBT/REVENUE 将被填满。

目前已经知道CSCSTEL和SSTEEL的了。

4)

没有评论:

发表评论