Prestariang’s share price has been in the limelight recently as it tumbled more than 51% over the last 1 month due to various uncertainties surrounding the companies amid heavy selling pressure from institutional investors, namely, Kumpulan Wang Persaraan (KWAP) and AIA. While having recovered admirably in recent days, we are nevertheless ceasing coverage on the stock given the poorer earnings outlook due to an anticipated ballooning in its finance costs, continuous bleed in its education segment and it bread-and butter income stream (software) under threat. Due to internal resource allocation, we are ceasing research coverage of Prestariang. Our last call on the stock is Neutral with a TP of RM1.19.

INVESTORS in e-government service provider Prestariang Bhd have been on tenterhooks since the change in government, largely due to uncertainty over the status of one of its key projects.

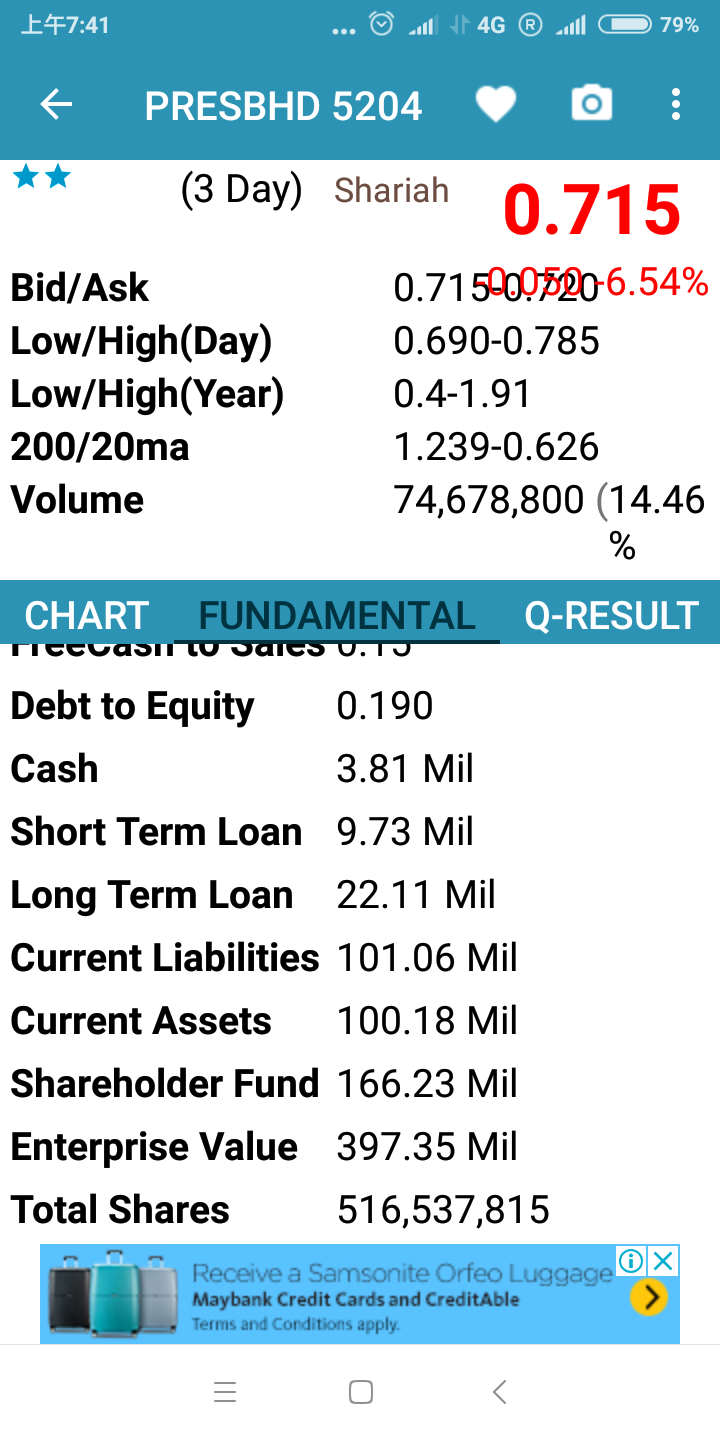

This was reflected in the stock crumbling to 44 sen last Monday, its lowest level so far this year and a 73% decline from its close of RM1.64 on the day before the 14th general election on May 9.

According to a filing with Bursa Malaysia on the same day, Prestariang founder and group CEO Dr Abu Hasan Ismail, who is also the company’s largest shareholder, saw forced selling of 15.1 million of his shares — representing a 3.13% stake held via his privately owned companies — to rectify a personal margin account position. Abu Hasan now holds a 24.3% stake in the company.

On Wednesday, however, Prestariang reversed its downward trend to hit an intraday high of 54.5 sen, gaining 24% in just two days.

So, what changed investor perception of the stock?

Although the company has yet to make any announcement on any of its projects, talk in the market has centred on the jewel in its crown — the RM3.5 billion Sistem Kawalan Imigresen Nasional (SKIN) project, which is understood to be one of the public-private partnership projects under review by the Ministry of Finance (MoF).

CIMB Research says in an Oct 23 report that based on its analysis of the company, there is a good chance the new government will soon approve the SKIN project.

“The Immigration Department’s MyIMMs IT infrastructure network, built in the 1990s, is outdated and there is an urgent need to replace it with a new IT infrastructure with the latest technology,” says the research house. “SKIN is a national security project.”

Assuming a weighted average cost of capital (WACC) of 6%, CIMB estimates SKIN’s value to be around RM750 million and since Prestariang owns 70% of it, the concession is worth RM525 million or RM1.08 per share to the company.

The remaining 30% of the SKIN project is reportedly owned by Muhammad Nagib Gopal Abdullah, Raja Azmi Adam Nadarajan and Faisalludin Mohamat Yusuff via their 30% stake in project owner Prestariang SKIN Sdn Bhd, whose CEO is Raja Azmi.

CIMB Research points out in its report that at 44 sen per share, the group’s business is being valued by investors at 13 times its FY2018 earnings, assuming zero value for the SKIN project.

PublicInvest Research has a similar valuation of the project. In a Sept 5 note, it says Prestariang’s stake in SKIN is worth RM521.3 million or RM1.08 per share, assuming a WACC of 7.48% and internal rate of return of 17%.

Given these assumptions, Prestariang’s closing price of 51 sen last Thursday implies a 53% discount to the value of the SKIN project.

“So far, there has been no confirmation of the status of SKIN from MoF. However, looking at the recent spike in its share price, it would seem that the market believes the project will go on but most likely at a lower price,” a market observer tells The Edge.

To recap briefly, SKIN is a new border control system that facilitates the movement of people in and out of Malaysia, and will replace the current system. On July 18 last year, Prestariang SKIN entered into a concession agreement with the Ministry of Home Affairs on the implementation of SKIN by way of a public-private partnership.

The project is a 15-year concession and will consist of three years of build and deployment phase and 12 years of maintenance and technical operation phase. Payment to Prestariang was to only commence upon the full commissioning of the system after three years with an average annual payment of RM294.7 million from year four to year 15 during the maintenance and technical operation phase.

Apart from SKIN, Prestariang’s other dealings with the government include its contract to supply Microsoft software licences, products and services. In January this year, its subsidiary, Prestariang Systems Sdn Bhd, received an extension of its contract to supply the licences to MoF under the Master Licensing Agreement 3.0.The extension is for three years, from Feb 1 this year to Jan 31, 2021, at an estimated value of RM222.6 million.

The group also received from the Ministry of Education an extension of its contract to supply Microsoft licences to public higher education institutions in the country for a year, from July 3 this year to July 2, 2019, at a total value of RM11.63 million.

In the first half of its financial year ended June 30 (1HFY2018), Prestariang reported a year-on-year decline of 22% in net profit to RM7.04 million due to higher tax expenses and provision for doubtful debts during the period. Revenue, however, rose almost 30% to RM128.68 million due to a higher contribution from the construction work for the SKIN project.

Besides Abu Hasan, Prestariang’s other substantial shareholders are Kumpulan Wang Persaraan (Diperbadankan) (KWAP) with an 8.6% stake, and Brahmal Vasudevan — who is the founder and CEO of private equity firm Creador — with a 6.2% stake.

Given the government’s announcement last Friday that it will accept MMC-Gamuda’s new, albeit lower, offer for the underground works of the MRT2 project, investors will be waiting to see whether the same fate befalls Prestariang.

3)

获联昌国际唱好 刺激Prestariang价量齐升

/

October 24, 2018 10:16 am +08

(吉隆坡24日讯)联昌国际投资银行研究表示,新政府可能会批准国家移民监控系统(SKIN)项目,提振Prestariang Bhd今早交投活络,股价上升9.89%。

截至早上9点31分,该股涨4.5仙,至50仙,约3701万股成交。稍早前,该股一度上探至52仙高位。

联昌国际投资银行研究维持给予Prestariang的“增持”评级,但把目标价从2.05令吉,下修至1.89令吉,并指该股价今年低于大市,主要是担心新政府可能不批准SKIN项目所致。

“由于该股价比我们的综合估值法(SOP)折价高达76%,因此,可趁机累积股票。维持‘增持’评级。”

分析员表示,假设加权平均资本成本(WACC)为6%,估计SKIN价值约7亿5000万令吉,基于Prestariang持有SKIN项目的70%股权,这意味着其特许经营权总值5亿2500万令吉或每股1.08令吉。

4)

转贴:目标价:1.89令吉

最新进展:

因投资者担忧新政府或不批准国家移民控制系统(SKIN)工程,必达量(PRESBHD,5204 ,主板科技股)今年内股价大跌了71%,表现低于富时小型股指数21.8%的跌幅。

过去数月,政府全面检讨与私人企业合作(PPP)合约,且财政部长林冠英表示,不打算取消任何相关项目。

而前任政府已对SKIN计划进行紧密审核,必达量也耗时4年才获得该项目的批准。

行家建议:

我们相信,基于SKIN是国家安全相关项目,所以还是很大机会,政府会批准。

目前该公司的股价,等于目标价高达76%的折价,所以相信是累积股票的好时机,维持“增持”评级。

不过,调整了SKIN的估算后,目标价从2.05令吉下调至1.89令吉。

另外,该股评级上调的催化剂包括SKIN项目不展延,及软件销售提升。

5)

About Us

|

Prestariang is a Technology and Talent pioneer that has evolved from being Malaysia’s largest ICT software and training service provider to a leading Technology and Talent Platform innovator.

Through its Transformation Plan, Prestariang's Technology Platform has successfully taken off with the award of Sistem Kawalan Imigresen Nasional (SKIN) by the Malaysian Government. Whilst, EduCloud, its Talent Platform, supports Entrepreneurship, Education and e-Commerce in the education sector was launched in conjunction with JobMatching PTPTN at a ceremony to commemorate the 20th Anniversary of Perbadanan Tabung Pendidikan Tinggi Nasional (PTPTN).

Today, Prestariang in collaboration with global partners, which include Imprimerie Nationale, Microsoft, Autodesk, IBM, Oracle, KPMG, University of Melbourne and many others, drives innovation in the Digital Economy.

Prestariang is also the largest Microsoft Licensing Solutions Partner in Malaysia.

Through its Technology and Talent Platforms, Prestariang will deliver its innovation through six (6) core deliveries namely, Analytics and Business Intelligence, Cyber and Information Security, Cloud Services, Change Management, Digital Ecosystem and SKIN-in-a-Box.

Prestariang Group remains committed to drive the technology industry in Malaysia towards and beyond the new digital economy era.

Business Ecosystem

AT A GLANCE

- Founded in 2003

- Headquartered in Cyberjaya, Selangor, Malaysia

- Market capitalisation of over RM1.0 billion (~USD245 million)

- Listed on the Main Market of Bursa Malaysia on 27 July 2011

(Stock name: PRESBHD | Stock Code: 5204 | Bloomberg - PRES:MK)

- Minimum of 50% profit payout dividend policy (i.e. quarterly basis) and a syariah-compliant stock

Our SERVICES

- Largest ICT training and certifications provider in Malaysia

- The exclusive distributor for Microsoft (Government agencies) and Adobe & IBM SPSS (Education) license software in Malaysia

- 'Sistem Kawalan Imigresen Nasional' (SKIN) – A 15 years concession project to implement and manage the immigration and national border control transformation program for the government of Malaysia

- Owns and operates University of Computer Science & Engineering (UNIMY), the first ICT-focused digital technology university in Malaysia

- Accredited Prestariang Skill Training Institute (PSTI), the first in Pengerang, Johor for TVET Program

Our PARTNERS

- Key partner of international companies including Thales, Alibaba Cloud, Microsoft, Autodesk, IBM, Oracle, Salesforce, KPMG, University of Melbourne and many others.

|

|

https://www.prestariang.com.my/

https://klse.i3investor.com/servlets/ptg/5204.jsp

https://www.malaysiastock.biz/Corporate-Infomation.aspx?securityCode=5204

目标价:RM1.00

个人分享,股市变化莫测,投资自负。