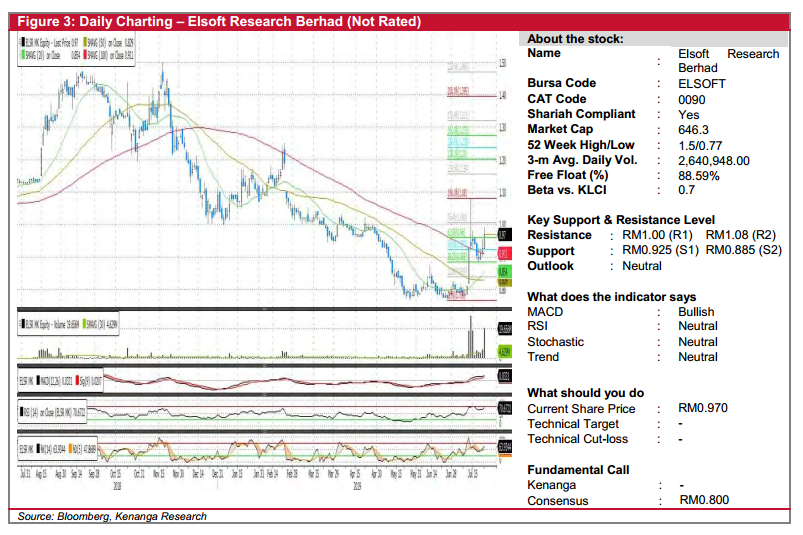

Elsoft 0090 艾尔软体简介:

公司于31/3/2019的现金为448万,无任何债务,现价(RM0.99)进其周息率为6.5%,ROE为31%,赚副为51%。

决定永远是你自己,買卖自负。

其他公司有赚钱可以考慮出货,買入0090收長期。RM2是目標且容易到达。

https://elsoftresearch.com/

https://elsoftresearch.com/product-category/industrial-io-board/

WHO ARE WE

Elsoft mainly provides cost effective ATE solutions to the semiconductor, optoelectronic and automation industries.

Elsoft is principally involved in research, design and development of test and burn-in systems and application specific embedded systems. Elsoft mainly provides cost effective ATE solutions to the semiconductor, optoelectronic and automation industries. The Group’s key product i.e. test and burn-in systems are used by its customers who manufacture optoelectronic devices such as LED, image sensors and automotive lightings to test their products before launching into the market. The name “Elsoft” consists of two elements i.e. Electronics and Software, symbolising the Group’s core competency in advanced electronics design and software technology innovation.

The company was founded by Mr. Tan Cheik Eaik, Mr. Koay Kim Chiew, Mdm. Tan Ai Jiew and Mr. Tan Ah Lek. With more than ten (10) years of experience in the ATE industry, the co-founders have been instrumental in the growth, success and development of the Elsoft Group. As a Chief Executive Officer, Tan Cheik Eaik has played an important role both in the business and product development.

The history of Elsoft Group can be traced back to 1996 with the incorporation of Siangtronics Technology Sdn Bhd (STSB), which was primarily involved in the manufacturing, retailing and designing of computer software, components and accessories. Since its inception, STSB has successfully developed various series of test and burn-in solutions for the semiconductor and optoelectronic industries and has grown considerably to become a key player in the ATE industry. Its customer base is made up of leading MNCs in the semiconductor and optoelectronic industries.

In 2003, pursuant to the restructuring exercise, STSB transferred its operations to Elsoft and concentrates on electronic devices/modules assembly, test and burn-in system integration and customised manufacturing solutions. The restructuring exercise enables the Group to accelerate prototype development and time to commercialisation and enhance the quality and performance of its solutions. In addition, the R&D resources of Elsoft extend the Group’s product to meet customers’ requirements, ensuring quality and cost competitiveness throughout every stage of design.

On 16 August 2018, Elsoft Systems is awarded the certification of standard ISO 9001:2015 Quality Management System. The certification is valid from 16 August 2018 until 15 August 2021.

Elsoft Systems is committed to achieve outstanding performance and deliver superior quality products that meet our customer’s expectation as well as the needs of all applicable interested parties. We believe employee’s commitment and teamwork is key towards achieving excellence in quality through continuous improvement.

达成的,大约有86%,之前提到的中国

达成的,大约有86%,之前提到的中国 则占13%,剩下的1% 公司没有说是哪里的。

则占13%,剩下的1% 公司没有说是哪里的。