--慕达由林氏家族所持有,年届82的主席丹斯里林源德,AS AT 21 MARCH 2017

直接及间接持有40.75%股权。亚洲文件夹有限公司 ASIAFLE 7129 则持有慕达控股17.97%的股权.

--慕达控股有限公司于1970年代开始作为私人有限公司的业务,并于1984年在马来西亚交易所上市。

公司于2005年改制为投资控股公司,目前子公司业务包括:

制造工业用纸,纸板和纸箱,纸基食品包装和文具,纸袋,贸易

纸张和学校书店的运作。

集团总资产达16亿令吉,在马来西亚,新加坡,中国和澳大利亚均有营运。 70%的

集团的产品在当地销售,其余出口到亚太地区,欧洲,中东和非洲。

制造设施

本集团经营两间造纸厂,七间瓦楞纸厂及另一间生产纸制食品包装及文具的工厂

产品。除中国广州的瓦楞厂外,其余工厂都位于西马。

集团在槟城的加影,雪兰莪和Tasek建立了两个主要生产基地。在Kajang,这个网站有一个

造纸厂和瓦楞纸厂,而在Tasek,该厂拥有造纸厂,瓦楞纸厂和生产纸张的工厂

基于食品的包装和文具产品。

除上述之外,集团在柔佛州新山和马六甲设有两个瓦楞厂

Muda owns one of the largest Paper Mills in Malaysia in terms of capacity and offers a wide range of products to our domestic and overseas customers. We are the leading producer of various industrial grade paper comprising Test Liner, Corrugated Medium, Laminated Chip Board, Core Board, Grey Chip Board, Yellow Wrapping Paper, Inserting paper, Manila paper, MF Kraft.

经济新闻

直接及间接持有40.75%股权。亚洲文件夹有限公司 ASIAFLE 7129 则持有慕达控股17.97%的股权.

--慕达控股有限公司于1970年代开始作为私人有限公司的业务,并于1984年在马来西亚交易所上市。

公司于2005年改制为投资控股公司,目前子公司业务包括:

制造工业用纸,纸板和纸箱,纸基食品包装和文具,纸袋,贸易

纸张和学校书店的运作。

集团总资产达16亿令吉,在马来西亚,新加坡,中国和澳大利亚均有营运。 70%的

集团的产品在当地销售,其余出口到亚太地区,欧洲,中东和非洲。

制造设施

本集团经营两间造纸厂,七间瓦楞纸厂及另一间生产纸制食品包装及文具的工厂

产品。除中国广州的瓦楞厂外,其余工厂都位于西马。

集团在槟城的加影,雪兰莪和Tasek建立了两个主要生产基地。在Kajang,这个网站有一个

造纸厂和瓦楞纸厂,而在Tasek,该厂拥有造纸厂,瓦楞纸厂和生产纸张的工厂

基于食品的包装和文具产品。

除上述之外,集团在柔佛州新山和马六甲设有两个瓦楞厂

集团目前共有员工超过2800人,业务仍在不断扩展之中。

--马来西亚大约拥有55条瓦楞纸板生产线,其瓦楞包装需求量将超过130万吨.马来西亚对瓦楞纸箱纸板消费保持着每年4-5%的增长,纸和纸板的人均消费超过60kg。大部分瓦楞纸箱生产企业位于马来西亚半岛,这里人口集中,是全国的经济命脉。现在马来西亚东部的六家瓦楞纸箱生产企业,主要为马来西亚东部的食品、饮料和其他当地行业提供纸箱产品。单面瓦楞纸板和三层瓦楞纸板大概占到了瓦楞纸板产品总量的70%左右,五层瓦楞纸板大概为30%。马来西亚市场拓展十分的迅速,但三级厂并不其中。Oji与Muda两大集团占据了马来西亚大约65-70%的市场份额。截止至2017年2月18日马来西亚已确定观展企业120家,其中就包含占据马来西亚包装市场大部分份额的Oji以及Muda。

Oji Paper Asia Sdn. Bhd:日本OJi(王子)集团,是马来西亚瓦楞包装市场领头企业之一在马来西亚拥有8家公司。

Muda paper millssdn.Bhd:1964年,Muda在马来西亚Tasek,Penang成立了第一家造纸厂。而如今,Muda是马来西亚最大的综合造纸厂之一,每年回收超过40万吨的废纸。并为当地和出口市场提供高档的纸板及相关产品。--公司于31-12-2017的库存有2.58亿,现金有9191万,借款为6.18亿,每股净资产为rm3.24

--马来西亚大约拥有55条瓦楞纸板生产线,其瓦楞包装需求量将超过130万吨.马来西亚对瓦楞纸箱纸板消费保持着每年4-5%的增长,纸和纸板的人均消费超过60kg。大部分瓦楞纸箱生产企业位于马来西亚半岛,这里人口集中,是全国的经济命脉。现在马来西亚东部的六家瓦楞纸箱生产企业,主要为马来西亚东部的食品、饮料和其他当地行业提供纸箱产品。单面瓦楞纸板和三层瓦楞纸板大概占到了瓦楞纸板产品总量的70%左右,五层瓦楞纸板大概为30%。马来西亚市场拓展十分的迅速,但三级厂并不其中。Oji与Muda两大集团占据了马来西亚大约65-70%的市场份额。截止至2017年2月18日马来西亚已确定观展企业120家,其中就包含占据马来西亚包装市场大部分份额的Oji以及Muda。

Oji Paper Asia Sdn. Bhd:日本OJi(王子)集团,是马来西亚瓦楞包装市场领头企业之一在马来西亚拥有8家公司。

Muda paper millssdn.Bhd:1964年,Muda在马来西亚Tasek,Penang成立了第一家造纸厂。而如今,Muda是马来西亚最大的综合造纸厂之一,每年回收超过40万吨的废纸。并为当地和出口市场提供高档的纸板及相关产品。--公司于31-12-2017的库存有2.58亿,现金有9191万,借款为6.18亿,每股净资产为rm3.24

--个人估计2018年Eps=28仙,pe=10,股价=Rm2.80

参考,进出自负。

--Muda 2018年第1,2,3季度业积很大机率超越去年的,趁回跌買入,中国禁止废纸进口,洛阳纸贵短期间会不变,作为大马唯一一家上游业务的慕达将受益,废紙便宜,成品銷售价好,从近期2017年第4季度业积取得8%多赚副,估计2018年的盈利爆升,取7%计,公司年营业额约15亿,盈利达1.05亿,1.05亿/305051,000=Eps 34 仙,取pe=10,股价可达Rm 3.40,现Rm1.90只是本益比5.5倍在交易,明显被低估了,加上公司多年沒回報股东,今年配合美丽业积,有望发放红股。

纸价上扬的赢家肯定是上游造纸业者(Muda Paper Mills, Oji Paper, Pascorp Paper),

因为他们拥有控制价钱的话语权.我的浅见,muda 30大股东己持近80%股份了,股价飞升速度之快于2月底业积出后己領敎过了,如这消息属实很快就漲停了,2018年在爆升净利下股价会是穩建挺进的。

只供参考,盈亏自负。

参考,进出自负。

--Muda 2018年第1,2,3季度业积很大机率超越去年的,趁回跌買入,中国禁止废纸进口,洛阳纸贵短期间会不变,作为大马唯一一家上游业务的慕达将受益,废紙便宜,成品銷售价好,从近期2017年第4季度业积取得8%多赚副,估计2018年的盈利爆升,取7%计,公司年营业额约15亿,盈利达1.05亿,1.05亿/305051,000=Eps 34 仙,取pe=10,股价可达Rm 3.40,现Rm1.90只是本益比5.5倍在交易,明显被低估了,加上公司多年沒回報股东,今年配合美丽业积,有望发放红股。

纸价上扬的赢家肯定是上游造纸业者(Muda Paper Mills, Oji Paper, Pascorp Paper),

因为他们拥有控制价钱的话语权.我的浅见,muda 30大股东己持近80%股份了,股价飞升速度之快于2月底业积出后己領敎过了,如这消息属实很快就漲停了,2018年在爆升净利下股价会是穩建挺进的。

只供参考,盈亏自负。

-- good future --

Looking forward, Muda said it expects positive domestic and global economies to drive the consumption of industrial paper and paper packaging products that would translate into higher demand for its products.

The planned capacity expansion in Melaka and Johor by the third quarter and fourth quarter of 2018 respectively, and completion of phase one of its paper machine expansion, is timely for the expected increase in demand for paper packaging products and industrial paper.

“Being mindful of the potential hike in energy cost, fluctuation in price of raw material, increase in interest rate and strengthening ringgit against US dollar, the board is confident of Muda’s profitability in FY18,” it said.

Looking forward, Muda said it expects positive domestic and global economies to drive the consumption of industrial paper and paper packaging products that would translate into higher demand for its products.

The planned capacity expansion in Melaka and Johor by the third quarter and fourth quarter of 2018 respectively, and completion of phase one of its paper machine expansion, is timely for the expected increase in demand for paper packaging products and industrial paper.

“Being mindful of the potential hike in energy cost, fluctuation in price of raw material, increase in interest rate and strengthening ringgit against US dollar, the board is confident of Muda’s profitability in FY18,” it said.

--good comment from davidtslim:

Summary

1)Muda has the highest capacity of paper mill (upstream) in Malaysia. It benefited from China Blue Sky policy (ban of waste paper import) which the selling price of their products have increased consistently from Q4’17 to Q1’18 while the raw material (waste paper) price has dropped.

2)The timely expansion of Muda in 2017 and 2018 (to be completed in Q3 and Q4) for its paper mill and corrugated plants coincident with the price surge of its product. This will further drive its profit growth especially in Q4’18 due to peak season of online retail shopping in Nov and Dec.

3)Since 2nd half of 2017, paper price in China has been rising, and remain elevated until now. This was caused by shutting down of plants to improve environment. As China is a huge consumer of paper packaging products, the price increase spilled over to international market

4)The demands in Malaysia for corrugated products will continue to grow especially Malaysia now serve as Alibaba’s regional e-commerce and logistics hub in South East Asia.

5)Based on the higher demands and selling price of paper mill products, profit margin of Muda should be expanded in 2018 and it may has some export opportunity.

6)Based on estimated EPS of 38 sen, with forward 12-month PEx of 10x, the fair value of Muda is estimated to be around RM3.8.

7)Muda2018 = (Upstream+downstream+trading) X (Expansion+price hike) = High_Profit_Growth

--网友分享

http://oldfriendsinvesting.blogspot.my/2018/04/muda-7th-april-2018.html

http://oldfriendsinvesting.blogspot.my/2018/04/muda-7th-april-2018.html

公司业务:

a)Mills Division

Summary

1)Muda has the highest capacity of paper mill (upstream) in Malaysia. It benefited from China Blue Sky policy (ban of waste paper import) which the selling price of their products have increased consistently from Q4’17 to Q1’18 while the raw material (waste paper) price has dropped.

2)The timely expansion of Muda in 2017 and 2018 (to be completed in Q3 and Q4) for its paper mill and corrugated plants coincident with the price surge of its product. This will further drive its profit growth especially in Q4’18 due to peak season of online retail shopping in Nov and Dec.

3)Since 2nd half of 2017, paper price in China has been rising, and remain elevated until now. This was caused by shutting down of plants to improve environment. As China is a huge consumer of paper packaging products, the price increase spilled over to international market

4)The demands in Malaysia for corrugated products will continue to grow especially Malaysia now serve as Alibaba’s regional e-commerce and logistics hub in South East Asia.

5)Based on the higher demands and selling price of paper mill products, profit margin of Muda should be expanded in 2018 and it may has some export opportunity.

6)Based on estimated EPS of 38 sen, with forward 12-month PEx of 10x, the fair value of Muda is estimated to be around RM3.8.

7)Muda2018 = (Upstream+downstream+trading) X (Expansion+price hike) = High_Profit_Growth

--网友分享

solaris80 有个可能,老板用业绩来包装公司,来卖的中国或日本潜在买家。不久前就做了的资产从新估值NTA RM3.1,我看成是卖公司的前奏。Harta Pack在2010年,卖给王子纸业是是以2.8倍的Book Value来出售。Muda的值产有RM3.1,如果以当时Harta被收购的估值来评价的话,可以自己用计算机算看,Rm3.1x2.8=8.6。纯属推测。

03/03/2018 15:00

solaris80 Muda上游有500千吨加上下游现在有240千吨,过后接下来的几个月还有新的三架机器投产。单单Muda的下游240千顿,都已经值得两亿了,如果和Orna比较的话。Oji paper 才要刚建的上游新产能,450千吨的产能就要价12亿。现在Muda 500千上游吨产+240千吨下游产能才卖你6亿,价钱是否低估了?

MUDA @ 7th April 2018 - oldfriendsinvesting

Author: Tan KW | Publish date:

Friday, April 6, 2018

MUDA @ 7th April 2018

Disclaimers:

The raw data are extracted from internet without further validation. Readers are advised to refer to BURSA for the official financial figures of the mentioned listed company.

The raw data are extracted from internet without further validation. Readers are advised to refer to BURSA for the official financial figures of the mentioned listed company.

The raw data are extracted from internet without further validation. Readers are advised to refer to BURSA for the official financial figures of the mentioned listed company.

The raw data are extracted from internet without further validation. Readers are advised to refer to BURSA for the official financial figures of the mentioned listed company.

公司业务:

a)Mills Division

Muda owns one of the largest Paper Mills in Malaysia in terms of capacity and offers a wide range of products to our domestic and overseas customers. We are the leading producer of various industrial grade paper comprising Test Liner, Corrugated Medium, Laminated Chip Board, Core Board, Grey Chip Board, Yellow Wrapping Paper, Inserting paper, Manila paper, MF Kraft.

Ours mills have been accredited with ISO 9001 and OHSAS 18001 and our product qualities have gained industry-wide recognition and acceptance by our customers. Our branding of "Muda Board" has now won international recognition through our continuous presence in annual international trade fairs.

In line with our corporate mission, we continue to grow in tandem with the growth in market demand. We will be adding new machine capacities in 2010 to achieve a combined output of over 500,000 metric tons per annum.

Our mills are equipped with effluent treatment facilities to ensure that the mills effluent discharge will not cause harm to the environment. The mill is also equipped with a CHP plant to further save on energy consumption and to reduce carbon emission.

b)Packaging and Converting Division

Our corrugating and converting plants are strategically located throughout Peninsular Malaysia to provide packaging solutions to customers from various business sectors consisting of SMES to multinational companies. This geographical spread allows us to serve the customers better and faster.

With two paper mills in the Group, the Group's corrugated cartons plants are assured of uninterrupted supply of quality recycled industrial grade paper. With this Group synergy, the Group's cartons plants are able to provide quality value added products at competitive prices, reliable packaging solutions and on-time deliveries to its customers consistently.

We aim to be the preferred carton and packaging solution provider for all our customers and in line with the demand for more sophisticated packaging solutions, we are always on the lookout for innovative ways to meet customers' packaging requirement.

With two paper mills in the Group, the Group's corrugated cartons plants are assured of uninterrupted supply of quality recycled industrial grade paper. With this Group synergy, the Group's cartons plants are able to provide quality value added products at competitive prices, reliable packaging solutions and on-time deliveries to its customers consistently.

We aim to be the preferred carton and packaging solution provider for all our customers and in line with the demand for more sophisticated packaging solutions, we are always on the lookout for innovative ways to meet customers' packaging requirement.

c)Marketing and Trading Division

The future growth of the Group's main business divisions requires the continual support of its existing customers and expansion of customers' base.

To serve our domestic and overseas customers efficiently, the Group has extensive marketing and sales offices throughout Malaysia as well as in Hong Kong, Australia and Singapore.

Our team of experienced and well trained sales and marketing personnel will strive to provide customers with the best professional services and logistics support so that our quality products will arrive at customers' warehouses in the shortest possible time.

To serve our domestic and overseas customers efficiently, the Group has extensive marketing and sales offices throughout Malaysia as well as in Hong Kong, Australia and Singapore.

Our team of experienced and well trained sales and marketing personnel will strive to provide customers with the best professional services and logistics support so that our quality products will arrive at customers' warehouses in the shortest possible time.

Our Products

Our products depicted throughout this website are subject to stringent quality control. Our laboratories are equipped with the best equipment to carry out all necessary quality tests procedures to ensure total customer satisfaction.

R & D work on product innovations is also carried out by our companies in order to offer products with better value added and packaging solutions to our customers.

R & D work on product innovations is also carried out by our companies in order to offer products with better value added and packaging solutions to our customers.

--末季业绩报捷 慕达控股涨停板

经济新闻

27/02/2018 18:57

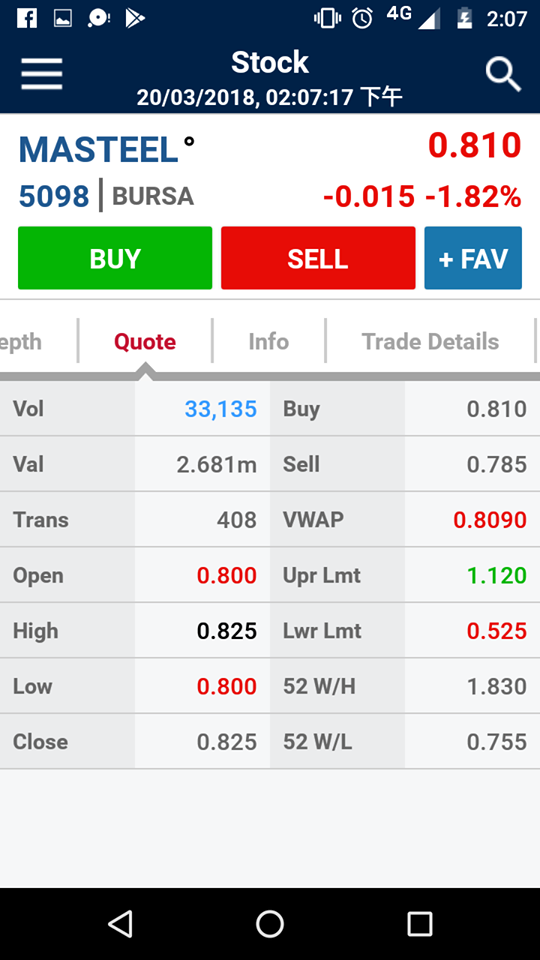

(吉隆坡27日讯)因纸品需求遽增和售价上扬,北马纸业先驱慕达控股有限公司(MUDA,3883,工业产品组)第四季净利增长一倍,激励公司股价今天涨停板,也是马股涨幅第七高的股只。’

闭市时,该股扬39仙或30%,报1.69令吉,成交量有119万9100股。

慕达控股于周一公布,截至去年12月杪末季净利达3597万令吉,或每股11.79仙,高于上财年同期的1791万令吉,或每股5.87仙,因售价以及造纸和纸包装产品的需求提高。末季营业额从3亿6089万令吉,扬25.23%至4亿5195万令吉,归功于制造业务的收入走高。2017财政年全年的净利为5877万令吉,或每股19.26仙,较2016财年的1881万令吉,或每股6.17仙,涨幅为212.47%,这是由于确认保险公司的赔偿。

纸包装产品需求和售价上涨,抵销较高的原料成本,促使全年营业额由12亿2000万令吉,增18.94%至14亿5000万令吉。展望未来,慕达控股预计国内和全球经济乐观,将推动工业纸和纸包装产品的消耗,这将使产品的需求增加。另一方面:根据《九点股票》网站早前分析,中港台纸品发力狂涨,大马纸业公司料将随着"洛阳纸贵"掀涨风。

纸品料掀涨风

“网购狂热,纸盒耗量惊人,造成国际纸品价格疯涨,中港台三地的纸品上市公司,股价都作三级跳,让眼光好的投资者从纸品业股赚了不少。”

“大马股票交易所里共有十七家上市公司涉及纸品生产,惟这些纸品公司的股价在纸价飞天之际,并没有闻风起舞,有些股价甚至倒跌。”

《九点股票》网站发现,大马股市里只有丹斯里林源德家族控制的慕达控股是唯一上游纸品公司,因此最有可能从中受惠。

该网站认为有可能搭上纸业热潮,基本面也不错的纸业公司是慕达控股,彦武纸业有限公司(ORNA ,5065,工业产品组)和合众机构有限公司(UPA ,7757,消费产品组)。 慕达控股的股价走势去年五月开始从1.79令吉呈下滑趋势,周一闭市价为1.30令吉。

http://klse.i3investor.com/servlets/stk/3883.jsp

http://www.muda.com.my/

1)http://m.jrj.com.cn/madapter/stock/2018/01/31042024034405.shtml

http://www.muda.com.my/

1)http://m.jrj.com.cn/madapter/stock/2018/01/31042024034405.shtml

造纸业7成公司净利倍增 纸价或再创新高

综合成本压力大 瓦楞原纸价格节节攀升

三大政策持续加码,2018年的纸价走势将深受影响

国际纸漿维持上行趋势

造紙產業鏈簡介

3点揭秘废纸价上涨内幕,或推动箱板瓦楞纸价维持高价位!

纸价即将脱缰,是顺应大势,还是跟风乱象?

8)http://www.chinapaper.net/news/show-26257.html

纸价大副上漲,后市继续看漲.

8)http://www.chinapaper.net/news/show-26257.html

再增涨价函,巨头带纸价直追历史高点!

9)http://www.chinapaper.net/news/show-26655.html纸价大副上漲,后市继续看漲.